AI stocks have continued to climb so far into 2025, though big-cap stocks in AI have started to slow down considerably over the past few months. Names like Palantir (NASDAQ:PLTR) are still delivering explosive growth, but there are AI stocks that currently have better long-term value worth looking into.

Regardless, the broader AI industry looks quite solid as companies have doubled down on data centers and AI investments after the DeepSeek spook. If the AI rally continues, it will likely lift most if not all boats in the sector this year, but I believe certain stocks are worth looking deeper into as they don’t trade at nosebleed valuations yet and offer high upside potential with limited downside risk. Here are the three AI stocks:

ACM Research (ACMR)

ACM Research (NASDAQ:ACMR) makes advanced wafer processing equipment. The company’s products are a key part of the semiconductor supply chain and it has grown significantly as chip demand increases.

It has very solid financials and raised its 2024 guidance to $755-770 million, which is up about 4% from its prior guidance. It also projects 2025 revenue at $850-950 million. Q3 2024 revenue grew 21% year-over-year to $203.98 million, with net income growing 20.4% to $30.9 million.

Yet, the stock trades at just 11 times forward earnings and 1.6 times 2025 sales estimates. ACMR is also down 49% from its 2021 high. This isn’t what makes me optimistic though.

A short-seller named Kerrisdale Capital pointed out that its Shanghai subsidiary has a much higher valuation compared to ACMR. ACM Research (Shanghai) trades with a valuation of $6.2 billion, whereas the stock we are talking about has a valuation of just $1.43 billion. ACM Research owns 82% of ACM Research (Shanghai) Inc. When you combine that with the growth, I think there’s solid upside potential here.

Snowflake (SNOW)

Snowflake (SNOW)

Snowflake (NYSE:SNOW) is up 52.6% in just the past six months but is still down by over 51% from its 2021 highs. It doesn’t trade as cheap but it still has lots of upside potential when you compare it to some of its peers.

The company’s data center business is well-integrated into some of the biggest AI models. For example, Cortex AI is a fully managed service for LLMs, and it integrates with Anthropic’s Claude 3.5 models and Meta’s (NASDAQ:META) Llama 3.2. It also adopted Nvidia’s (NASDAQ:NVDA) AI Enterprise software and acquired Datavolo to streamline data processing for generative AI.

Over 2,500 customers now use Snowflake’s AI tools weekly, and product revenue grew 29% year-over-year to $900 million in Q3 FY2025. Analysts project AI-driven workloads will fuel 21%+ product revenue growth in FY2026. On top of that, Q3 FY2025 total revenue hit $942 million and grew 28% year-over-year, and profitability is expected for all of FY2025.

The stock doesn’t trade cheaply by any means, but considering how high the market has taken other software stocks like Palantir for similar growth, SNOW could play out very well.

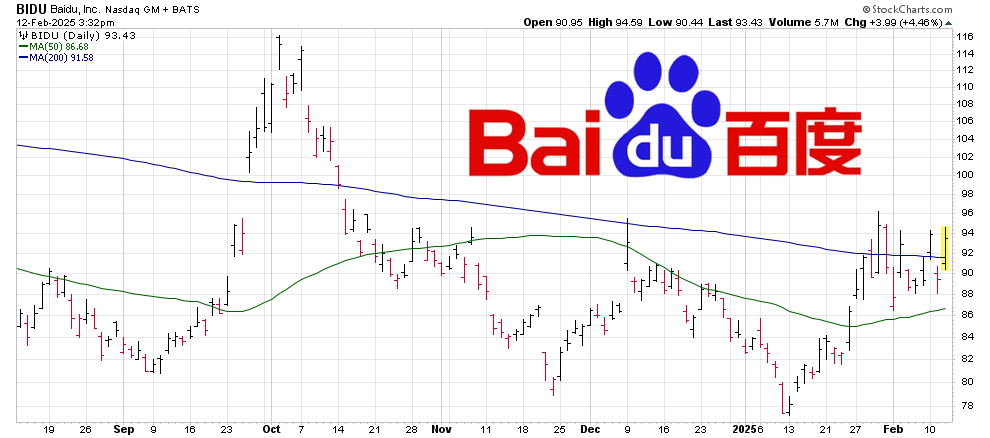

Baidu (BIDU)

Baidu (BIDU)

Baidu (NASDAQ:BIDU) is probably one of the cheapest AI stocks you can buy right now, and the stock’s downside risk is very low compared to the possible upside potential here. It is basically China’s Google (NASDAQ:GOOG, NASDAQ:GOOGL) and has been transitioning into one of its biggest AI and data center companies.

Chinese companies are unlikely to use Western data centers for their AI models, so it makes sense why analysts are starting to turn bullish on Chinese data center companies as China makes solid AI models. Baidu itself is expected to come out with its own next-gen AI model this year. Alibaba (NYSE:BABA) did something similar right after DeepSeek and analysts have rewarded the stock handily, so I see no reason to not be bullish on BIDU stock. Baidu’s AI Cloud revenue is already driving its core growth.

It is also a very profitable company and has a multi-billion buyback program in play. As such, paying just 9 times forward earnings for the long-term potential here seems quite cheap. The stock is up 13% year-to-date.

— Omor Ibne Ehsan

— Omor Ibne Ehsan

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning