The artificial intelligence boom has inflated valuations across the tech sector, turning market leaders and peripheral players into overpriced darlings. Companies like Nvidia (NVDA) and Advanced Micro Devices (AMD) command premiums for their pivotal roles in AI hardware, while peripheral players such as Palantir Technologies (PLTR) boast tremendous growth potential but stretch credulity with metrics like 213x trailing earnings, 73x forward estimates, and a whopping 72x sales.

Investors rationalize these multiples by pointing to PLTR’s data analytics prowess in AI applications, yet the hype often outpaces fundamentals.

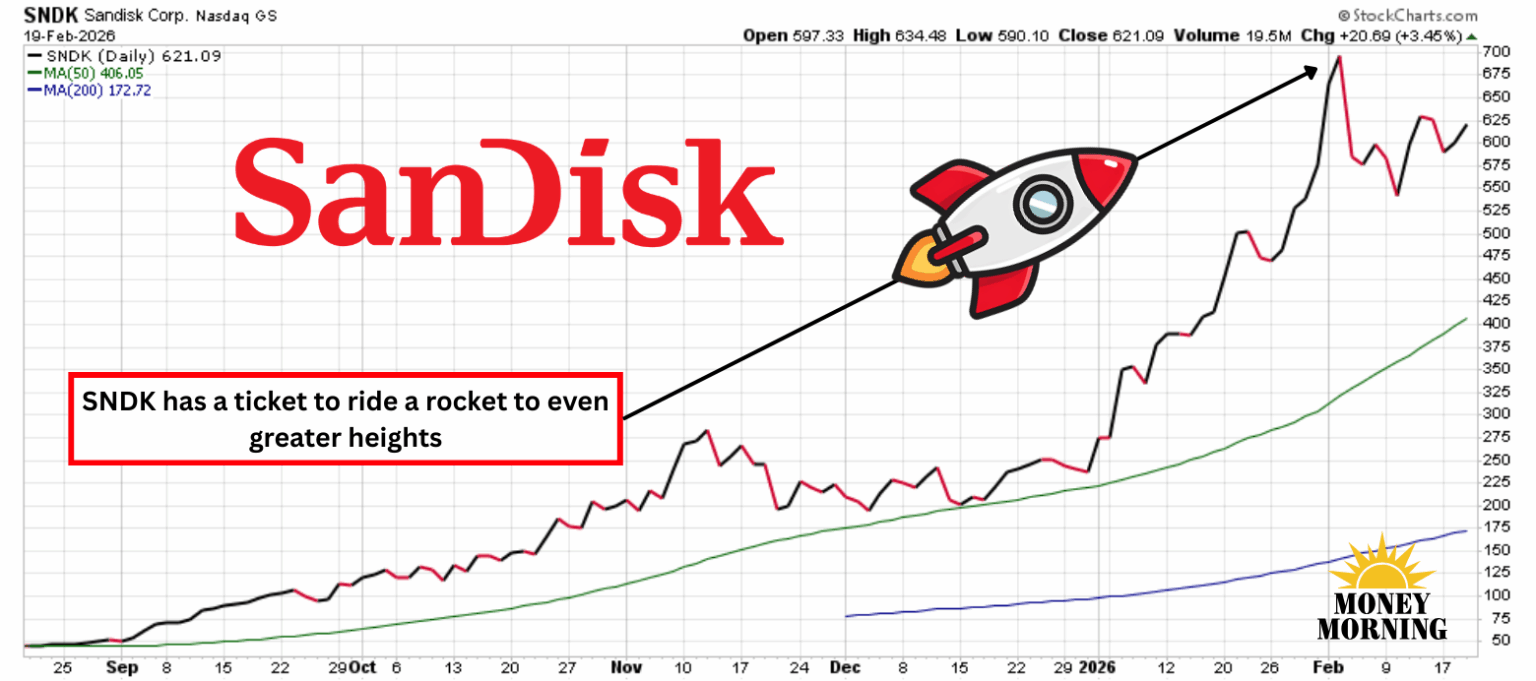

What if you could buy a stock that was both a high-octane growth engine and a genuine bargain? You can. SanDisk (SNDK) – the memory specialist that’s quietly powering the AI data explosion – is the full package.

The Spinoff That Sparked a Surge

SanDisk’s journey as an independent entity began with its spinoff from Western Digital (WDC) last year, separating the flash memory business to focus on NAND and solid-state drives. Initially, the market took time to warm up, with shares languishing as investors digested the restructuring. But traction built rapidly as AI-driven demand for high-capacity storage exploded.

Over the last six months, SNDK has surged 1,300%, fueled by an insatiable appetite for memory in data centers. Tech giants like Amazon (AMZN), Google, and Microsoft (MSFT) are in a frenzy to build out AI infrastructure, where vast datasets require robust, fast storage solutions. This buildout shows no signs of abating, with analysts projecting continued double-digit growth in global data center spending.

SNDK’s products – high-performance NAND flash – are at the heart of this, enabling efficient data handling for machine learning models and generative AI.

Unpacking the Bargain Valuation

Unpacking the Bargain Valuation

What truly sets SNDK apart is its dirt-cheap valuation despite blistering growth. Trading at just 7x forward estimates, it’s a steal compared to peers. Even more striking is its PEG ratio of a minuscule 0.04x, as it factors in Wall Street’s projected earnings growth rate of an eye-bleeding 185% annually over the next five years, driven by AI’s memory-intensive needs.

Sure, it commands 10x sales, but in the tech universe where multiples often hit 20x or more, this is bargain-basement territory. SNDK is already profitable, though it lacks a traditional P/E ratio since it hasn’t yet reported four full quarters of earnings post-spinoff. That said, its latest quarter showed earnings skyrocketing 408% year-over-year, underscoring operational strength and market dominance in memory tech.

Bottom Line

SNDK has it all: a highly in-demand product lineup essential for AI’s data-hungry ecosystem, surging sales from the ongoing data center boom, skyrocketing earnings that validate its growth narrative, and a valuation that’s remarkably cheap even after recent stock gains.

In an AI landscape riddled with overvaluation, SNDK offers investors a rare combination of upside potential and downside protection – making it a compelling pick for those seeking value in the hype.

— Rich Duprey

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning