Intuit (INTU) just delivered a standout performance in its fiscal Q1 2026 earnings, crushing Wall Street expectations on both the top and bottom lines. Revenue soared 18% year-over-year to $3.89 billion, handily beating estimates of $3.77 billion, while non-GAAP EPS jumped to $3.34, topping consensus by 8%.

The company’s AI-fueled platform continues to drive momentum across small businesses and consumers. Yet, guidance for Q2 earnings came in a little light at $3.63-$3.68per share versus expectations around $3.84, but the stock is still up 4% premarket.

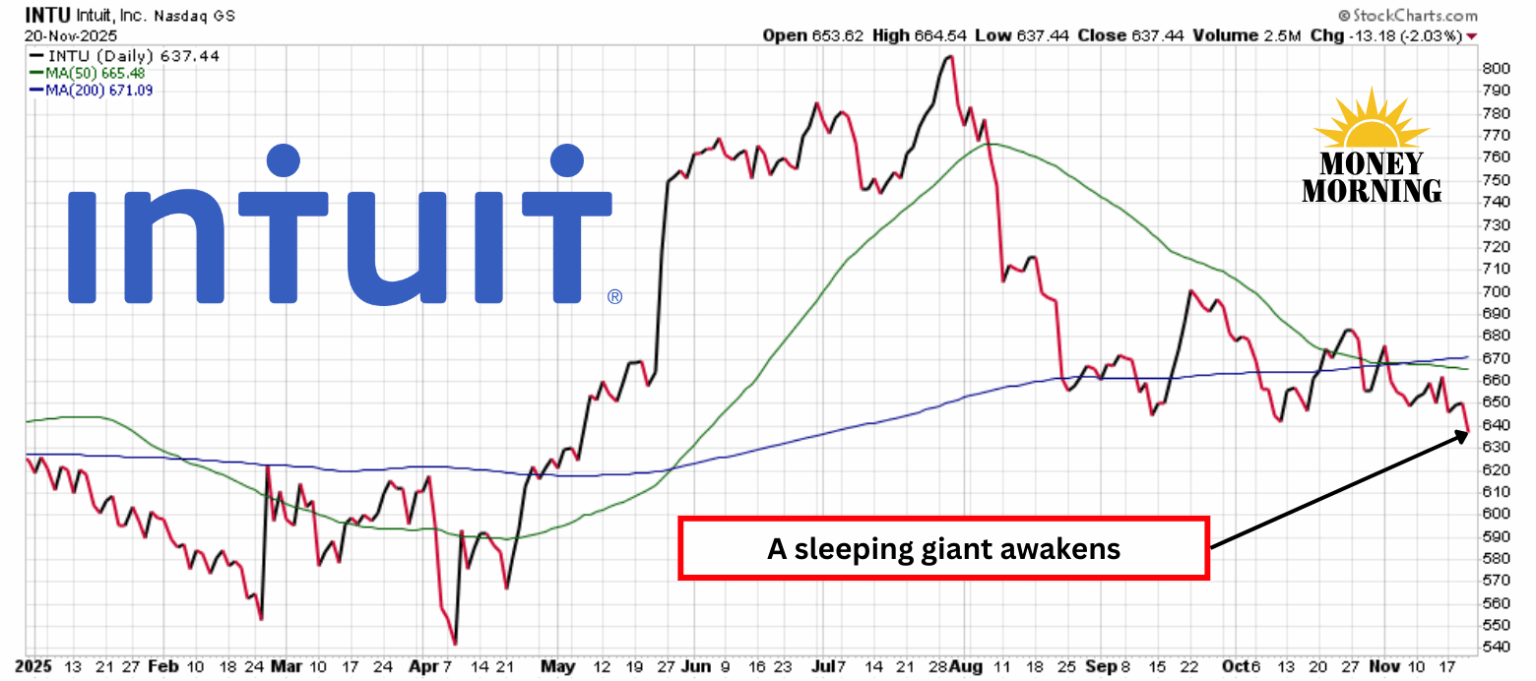

With INTU shares down over 20% from recent highs and up just 1.4% year-to-date amid broader market volatility, this pullback screams opportunity. Trading near $650 per share, Intuit stands out as the most compelling fintech buy right now – blending defensive moats with explosive AI-driven growth.

AI and Platform Momentum Shine Through

Intuit’s outperformance was broad-based. The Small Business and Self-Employed segment powered ahead, with Online Ecosystem revenue surging around 40%, fueled by QuickBooks advancements and AI agents adopted by 2.8 million users – saving customers hours on accounting and accelerating payments.

Consumer revenue climbed 21%, TurboTax was up 27%, and Credit Karma accelerated to 15% to 27% growth depending on metrics, thanks to year-round financial tools and AI personalization.

Margins also expanded sharply, with non-GAAP operating income rising as AI efficiencies kicked in. Management reaffirmed full-year revenue guidance at around $21 billion (implying 12% to 13% growth) and EPS at $22.98 to $23.18 (14% to 15% growth), signaling confidence despite conservative near-term profit outlook tied to ongoing AI investments.

These “done-for-you” AI features aren’t hype – they’re delivering real productivity gains, higher retention, and cross-sell in an ecosystem spanning QuickBooks, TurboTax, Credit Karma, and Mailchimp.

Why Intuit Deserves a Spot in Your Portfolio Today

Why Intuit Deserves a Spot in Your Portfolio Today

In a fintech landscape littered with high-burn disruptors, Intuit is the rare profitable powerhouse. Its 40%+ operating margins dwarf peers, backed by sticky subscription revenue and a massive moat in tax and small-business software. AI isn’t a bolt-on; it’s part of Intuit’s core – powering personalized insights, automation, and mid-market expansion via partnerships with accounting firms.

At current levels, INTU trades at a reasonable forward P/E of 24x given mid-teens EPS growth projections over the next five years, generous buybacks ($851 million in Q1 alone), and a 15% dividend hike yielding 0.7%. While pure-play fintechs swing wildly, Intuit’s resilience through cycles – plus a $100 billion addressable market – makes it the steady compounder disguised as fintech.

Bottom Line

The post-earnings dip is a gift for patient investors. Intuit isn’t just surviving the AI wave, it’s leading it with tangible results. For investors seeking fintech exposure without the volatility, INTU is the overlooked gem poised for outsized returns.

At its September Analyst Day conference, CFO Sandeep Aujla highlighted this growth, pointing out, “About 10 years ago, we were less than $5 billion in size, growing 8%. Today, we are four times that size – nearly $20 billion – growing at double the rate at 16%, with 40% operating margins, and the best is yet to come.”

The discount the stock offers makes this the perfect time to buy, getting in before the rest of the market awakens to this sleeping platform titan.

— Rich Duprey

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning