The tech sector has still held strong so far, and many have said the AI rally is back after the market recovery in the past two weeks. You could ride that wave by parking a sliver of your portfolio in carefully chosen hypergrowth names that might become multibaggers.

The current environment is still full of opportunities. Wall Street is combing the market for “the next Nvidia” and will bid up any tech stock with a hypergrowth business. Of course, I wouldn’t bet a very meaningful amount of your portfolio into these stocks. But if you put a 3% to 5% slice into these high-risk, high-reward stocks, that small stake could balloon if one of those businesses becomes the next powerhouse. Here are three hypergrowth tech stocks to look into. All of them have over 40% one-year revenue growth.

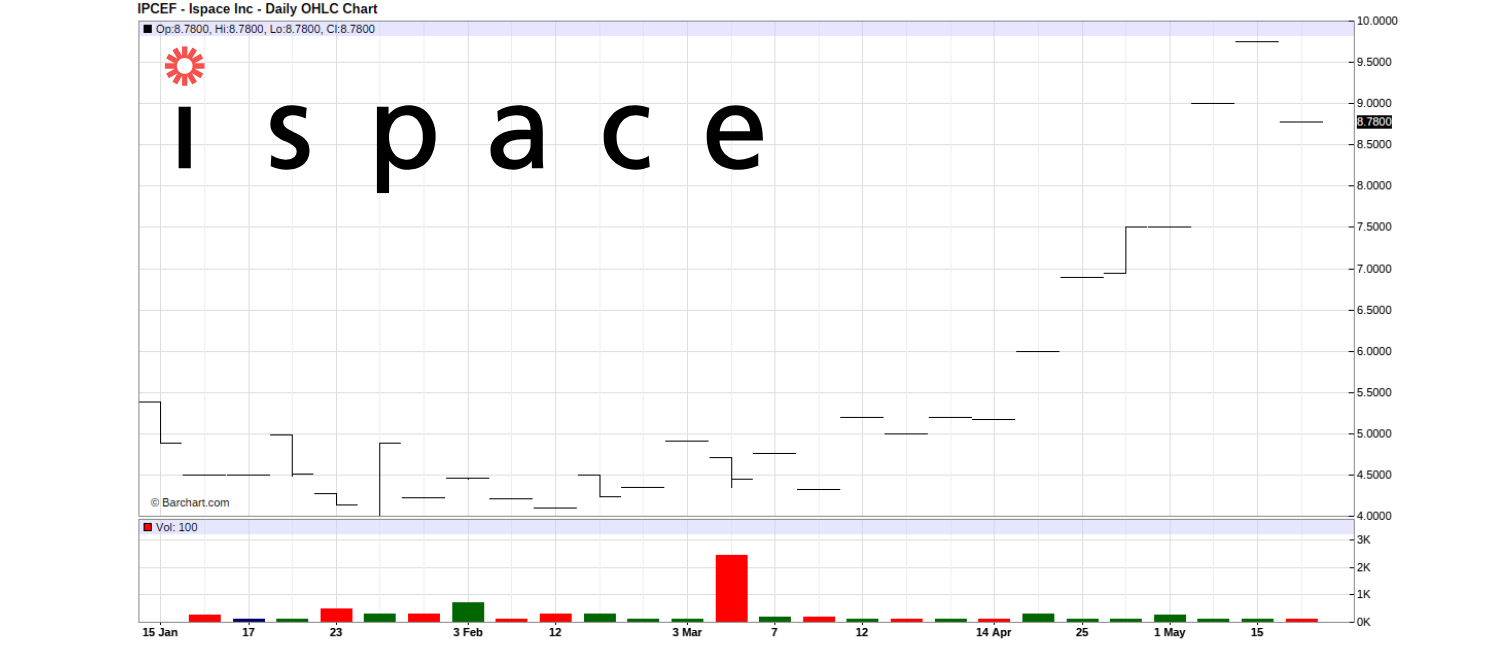

ispace Inc (IPCEF)

ispace Inc (OTCMKTS:IPCEF) has been gaining a lot of steam in the past few weeks, but it is still quite unknown on Wall Street. This Japanese company has nearly $1 billion in market capitalization, but it is less talked about than even some penny stocks.

ispace Inc (OTCMKTS:IPCEF) has been gaining a lot of steam in the past few weeks, but it is still quite unknown on Wall Street. This Japanese company has nearly $1 billion in market capitalization, but it is less talked about than even some penny stocks.

If the company sticks the landing on its next mission and begins collecting steady payload fees, I believe the market will wake up fast, and the stock could deliver multibagger gains within a few years.

It is building a larger lander to deliver Draper’s NASA CLPS payloads to the far‑side Schrödinger Basin in 2026, and Draper just released an additional $7.7 million toward that contract in March 2025 .

The global space economy is forecast to triple to $1.8 trillion by 2035 with a 9% CAGR. Transport to the Moon is a high‑margin niche inside that surge. There’s also more interest about another human moon landing, which could send IPCEF stock even higher if it materializes.

Aeva Technologies (AEVA)

Aeva Technologies (NASDAQ:AEVA) has been on an explosive rally in the past few weeks. It is up 588% since the middle of March, and while it is fundamentally overvalued at the moment, it might be worth considering if you are comfortable buying high for the long-term potential.

Aeva Technologies (NASDAQ:AEVA) has been on an explosive rally in the past few weeks. It is up 588% since the middle of March, and while it is fundamentally overvalued at the moment, it might be worth considering if you are comfortable buying high for the long-term potential.

This company specializes in hardware and perception software, and this includes LiDAR. LiDAR has long been seen as a subset of the electric vehicle industry, and something that was doomed due to major EV companies being disinterested in it due to the cost. But the recent AI rally is driving hype around robotics, and this is starting to be a lifeline for the sector.

LiDAR is much better than cameras or radar, and the only factor that is stopping it from dominating is the cost. Costs are starting to come down, and many EV companies have experimented with it, but the biggest opportunity now is the robotics industry, which is heavily using LiDAR.

AEVA stock has done much better than other LiDAR plays, but that’s for a reason. Startups that land contracts are building up the credibility that can help them land even more business down the line.

It got a $50 million investment from a Fortune 500 company and a development program with a top 10 global passenger OEM. It also has a multi-year contract with Daimler worth around $1 billion over its lifespan.

Red Cat Holdings (RCAT)

If you want exposure to the small military drones sector, Red Cat Holdings (NASDAQ:RCAT) is one of the only pure-plays you can invest in. The company already owns the Army’s Short‑Range Reconnaissance (SRR) program of record, it keeps booking fresh government orders, and it just lined up enough capital to scale production.

If you want exposure to the small military drones sector, Red Cat Holdings (NASDAQ:RCAT) is one of the only pure-plays you can invest in. The company already owns the Army’s Short‑Range Reconnaissance (SRR) program of record, it keeps booking fresh government orders, and it just lined up enough capital to scale production.

It was recently hit with a short-seller report about the company overstating revenue, but I’m more focused on the long-term revenue potential here. Over the next decade, small military drones will move from niche gear to standard kit because armies want cheap, expendable eyes in the sky.

Teal’s Black Widow quadcopter beat well‑funded rivals and became the Army’s SRR drone last November. it is already delivering early production batches, and it forecasts $25 million to $65 million of SRR sales this year. Beyond SRR, the company markets the Edge 130 fixed‑wing and the smaller Fang FPV loitering drone and sees another $30 million of 2025 revenue from those platforms. If we combine all of it, the company expects $80 million to $120 million in sales this year.

I’m definitely skeptical, but you won’t find surefire bets if you’re looking for multibaggers.

— Omor IE

Out of 23,281 Stocks... Only ONE is This Profitable and Undervalued. [sponsor]$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning