It’s finally here, the beginning of earnings season as three of the largest banks on Wall Street gave us their quarterly earnings results Friday morning.

The good news is that all the big banks came in with earnings per share results that were better that expected for the last quarter. Revenue for all three grew at an average of 7%, slightly lower than last quarter reflecting lighter activity in both loans and investment banking.

You’ll recall that just a few weeks ago CoreWeave (CRWV) saw its IPO fall flat on the market as institutional and retail investors backed away from the offering in the days ahead of its debut. This is a great “on the street” expectations of what the investment banks are considering for their outlook.

JP Morgan is Concerned About the Consumer

Consumer activity has slowed at the banks level as well. From credit card usage to loans, the consumer has clearly pulled back on their activity. This sentiment was also voiced by the airlines over the last three weeks as consumers are cutting back on travel ahead of the summer season.

JP Morgan’s Jamie Dimon appears to be stockpiling cash like Warren Buffett did in the closing months of 2024. The move goes along with Dimon’s view that the economy is heading towards a recession in 2025 as trade wars and the potential return of inflation will pressure consumers to a breaking point.

The bank backs that outlook by announcing that it has increased its provisions for credit losses to $3.3 billion from $1.9 billion last year. This is the figure that the bank uses to budget for losses due to its customers not being able to pay back loans. The increase is the largest since the country’s last recession.

The bank backs that outlook by announcing that it has increased its provisions for credit losses to $3.3 billion from $1.9 billion last year. This is the figure that the bank uses to budget for losses due to its customers not being able to pay back loans. The increase is the largest since the country’s last recession.

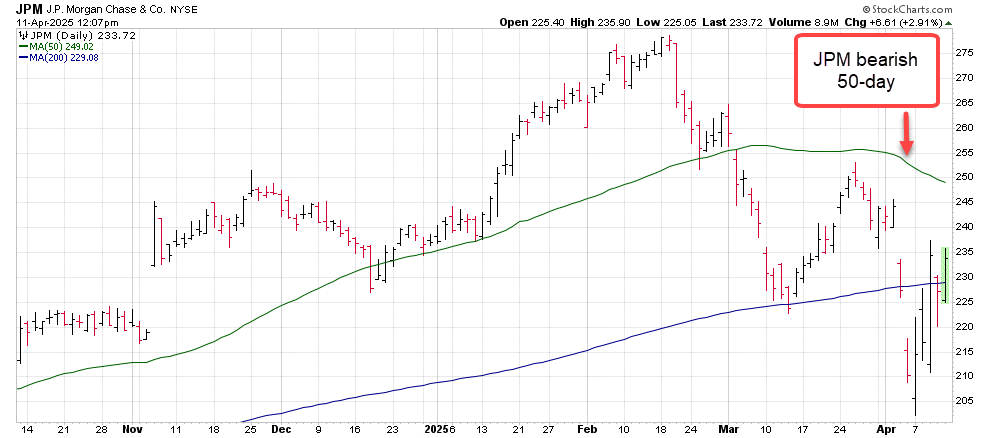

What to Expect from JP Morgan Chase Stock

Shares of JPM have been trading in the $230 range for the last month as they try to hold on to their 200-day moving average. Just two weeks ago, the stock’s 50-day moving average turned bearish suggesting that the path of least resistance is to the $200 price level.

JP morgan Chase’s earnings report backs up the fact that it is one of the “Best in Breed” banking stocks, however the market’s continued uncertainty and overall bearish tone will add pressure to the stock, likely forcing it into a short bear market with prices dipping below $200.

What the Financial Industry is Signaling

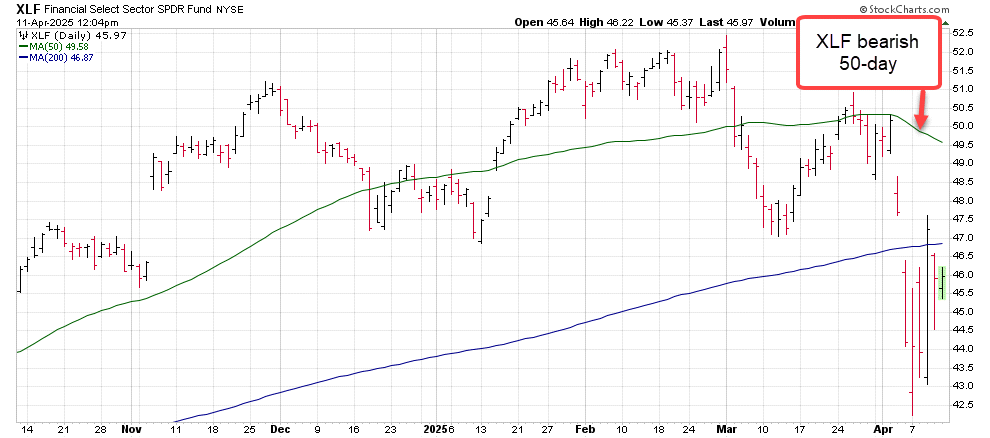

This week, the financial stocks – as represented by the SPDR Financial ETF (XLF) – saw buying as investors tried to “buy the rumor” ahead of the earnings season.

With just a few of the stocks in the ETF having reported their quarterly results its too soon to call a “sell the news” warning, but things don’t look great.

The XLF shares are now trading below their 200-day moving average. That trendline is seen by many on Wall Street as the “line in the sand” when it comes to the 4–6-month technical health of a trend.

Furthermore, the Financial ETF’s 50-day moving average shifted to a bearish trend just last week. A bearish trend of the 50-day for a stock, index or ETF is a consistent sign that a trend has turned unfriendly for investors.

Furthermore, the Financial ETF’s 50-day moving average shifted to a bearish trend just last week. A bearish trend of the 50-day for a stock, index or ETF is a consistent sign that a trend has turned unfriendly for investors.

Next week’s earnings season will continue early for the financials with companies like Goldman Sachs, Citibank and Bank of America reporting their results in the first two days of the week.

Failure of these companies to spark a Hail Mary style rally will send the financial ETF further into its intermediate-term bearish trend.

This is important to you because the financials are usually one of the swing sectors when it comes to whether the economy is heading towards a recession and bear market.

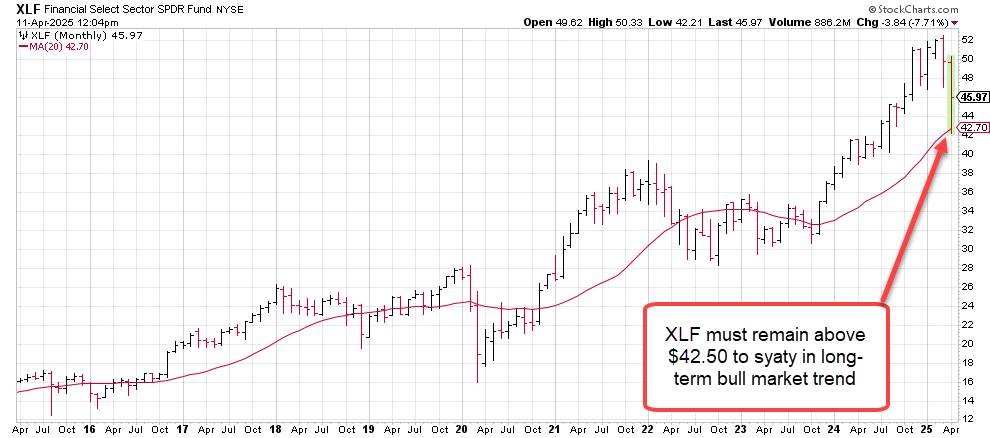

With that in mind, you should maintain a cautious eye on the XLF’s $42.50 price level. This level is the current price of the ETFs 20-month moving average.

That trendline is the line of demarcation between a long-term bull and bear market meaning that a close below $42.50 at the end of April will signal that the market is indeed heading towards a bear market that will drop prices another 10-20% as the earnings season continues.

— Chris Johnson

Out of 23,281 Stocks... Only ONE is This Profitable and Undervalued. [sponsor]$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning