A stock market selloff was due after the post-Trump election euphoria sent artificial intelligence stocks and other growth areas skyrocketing. Those massive runs followed countless triple-digit rebounds off the stock market’s 2022 lows.

The Trump election gains were wiped out over the last several weeks. The quick correction was healthy and represents a great opportunity to buy into the AI trade at more reasonable levels.

Even though there could be more downside in the near term, long-term investors should start to dip their toes into beaten-down AI stocks because no one knows if the bottom is already in.

The earnings growth picture remains impressive, with S&P 500 EPS projected to jump 13.3% in 2025 and 13.7% in 2026. The Fed is still projected to lower interest rates in 2025.

More than anything else, earnings and interest rates drive the stock market over the long haul.

Long-term investors don’t need to time the market exactly, because that is extremely difficult. What all great investors should do is buy into weakness because the stocks everyone wanted a few weeks ago cost 20%, 30%, and 40% less.

Buy this Top-Ranked AI Stock Down 45% from Its Highs?

Marvell Technology, Inc. (MRVL) is a leader in data infrastructure semiconductor solutions. MRVL boasts that its “custom silicon and system-level connectivity platforms enable hyperscalers to design and implement their own unique AI data-center architectures optimized for their own unique applications.”

Marvell’s products such as data center switches, DCI optical modules, enterprise switches, Ethernet controllers, and beyond are vital for efficient data transfer and advanced technologies including AI.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Marvell’s upbeat earnings outlook earns it a Zacks Rank #1 (Strong Buy) following its beat-and-raise Q4 report on March 5.

The company said that its AI silicon programs “entered volume production” and it continues to see strong growth from its interconnect products. Marvell also “secured multiple new design wins, including several custom silicon programs that will fuel future growth,” according to CEO Matt Murphy.

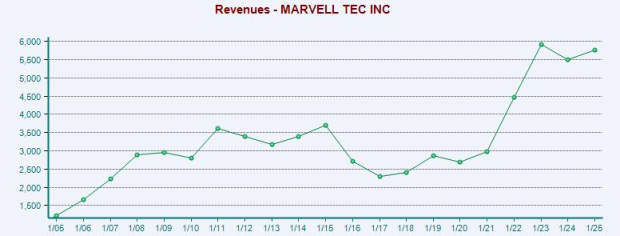

Marvell is projected to grow its revenue by 44% this year (its FY26) and 19% next year to soar from $5.77 billion last year to $10 billion next year. The AI-related boom is expected to help MRVL boost its adjusted earnings by 75% this year and 28% next year.

Why Did MRVL Stock Tumble?

Despite the solid fourth quarter and strong outlook, MRVL tanked after its March 5 report. The tech company’s Q1 2026 revenue forecast fell short of lofty expectations, sparking fears of slowing AI infrastructure spending. MRVL also got caught up in the DeepSeek and the recent AI-everything selloffs.

Marvell’s AI boom has come at the expense of many of its legacy segments. The tech firm posted a GAAP loss of -$1.02 a share last year.

Marvell’s losses are concentrated in shrinking legacy/non-AI data center markets such as carrier infrastructure. Macroeconomic softness and inventory missteps have hurt, leading to GAAP losses.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Thankfully, Marvel’s $1.68 billion in annual operating cash flow (fiscal 2025) demonstrates it’s not bleeding cash. Plus, it returned $933 million to stockholders through repurchases and dividends last year.

On top of that, 28 of the 32 brokerage recommendations Zacks has for MRVL are “Strong Buys.”

Is Marvel a Must-Buy Home Run Stock at These Levels?

Marvel stock has climbed 335% in the past decade to outpace the Zacks Tech Sector’s 275%. More recently, MRVL crushed tech, up 235% during the last five years vs. its sector’s 133%.

The outperformance includes its 45% tumble from its late-January peaks (tanking from $127 a share to ~$70 at the close on Wednesday). Marvel trades roughly 80% below its average Zacks price target.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

MRVL fell from its most overbought RSI levels in the past decade to some of its most oversold. Marvel is attempting to find support near its long-term 200-week moving and its May 2023 breakout levels.

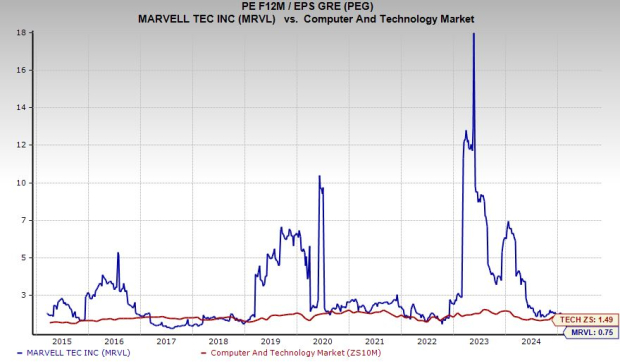

Marvel’s selloff, mixed with its earnings growth picture has it trading at a 50% discount to the Zacks Tech sector and 95% below its highs at a Price/Earnings-to-Growth ratio of 0.75. MRVL is trading at its decade-long lows in terms of its PEG ratio even though the stock has climbed 335%.

— Benjamin Rains

Want the latest recommendations from Zacks Investment Research? [sponsor]Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report.

Source: Zacks