Some stocks have been trading far below their intrinsic value and doing so well before the current correction. These stocks have been pushed even lower recently. There is now a wide gap between market price and intrinsic worth.

If you’re willing to look beyond the short-term volatility, these stocks offer solid upside potential and minimal downside risk. Historically, undervalued stocks have delivered outsized returns when the market corrects its mispricing. These returns are even better if you buy stocks with underlying businesses that have staying power.

Here are three to look into:

Wal Mart de Mexico (WMMVY)

Wal Mart de Mexico (OTCMKTS:WMMVY) is the largest retail chain in Mexico and Central America. It operates under the Walmart brand.

Wal Mart de Mexico (OTCMKTS:WMMVY) is the largest retail chain in Mexico and Central America. It operates under the Walmart brand.

The stock is up only 3.3% in the past five years due to it struggling in the past year. The stock traded sideways from mid-2022 to early 2024, but the trajectory turned negative as WMMVY struggled with flat year-over-year store traffic in Mexico.

Its efforts to invest in margins through promotions and pricing strategies have not yielded significant improvements either, so EBITDA performance has also been weaker than expected.

WMMVY’s fourth-quarter 2024 results fell short of analyst expectations, with adjusted EPS missing consensus estimates by 6%. This underperformance prompted JPMorgan to downgrade the stock from “Overweight” to “Neutral” and lower its price target.

However, the market seems to have gone too far. WMMVY now seems undervalued at its current price. It is still a very profitable company and is on solid footing. Analysts expect accelerating EPS growth from 4.72% in 2025 to almost 9% next year and above 10% in 2027. Revenue growth is also expected to hover around 7-8% in the coming years.

The consensus price target of $34.18 implies 29.47% upside. Even the lowest price target implies 21.2% upside.

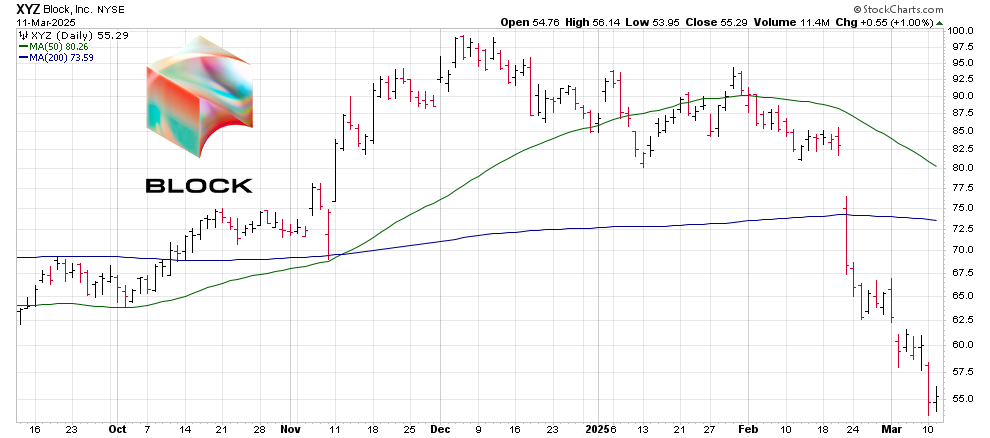

Block (XYZ)

Block (NYSE:XYZ) is a fintech company that declined significantly after the post-COVID bubble popped. It started to recover in 2024, but its recent decline has undone all of its gains. XYZ stock has now gone down 32.3% in the past year.

Block (NYSE:XYZ) is a fintech company that declined significantly after the post-COVID bubble popped. It started to recover in 2024, but its recent decline has undone all of its gains. XYZ stock has now gone down 32.3% in the past year.

Block reported weaker-than-expected revenue and profit for Q4 2024, missing analysts’ estimates for both earnings per share and revenue. It is facing growing competition from rivals like Toast, Clover, and Shift4 in the point-of-sale market. Moreover, fears of weakening consumer demand have added to its woes.

Despite all the negatives, I think the current valuation is more than prices in all the bearish sentiment. Growth has slowed down recently, but the long-term outlook is quite stellar. EPS is expected to more than double from 2025 to 2029, and you’re only paying a bit over 12 times forward earnings.

Revenue is also expected to grow 9.1% for the full year and grow at around 10% annually on average in the next decade. It should deliver solid long-term upside.

The consensus price target of $95.62 implies 72.35% upside.

Dollar General (DG)

Dollar General (NYSE:DG) is a company analysts expected to perform well during hard times. The company has a customer base of lower-income people, and considering the impact of high inflation in the past two years, its customer base was expected to grow massively.

Dollar General (NYSE:DG) is a company analysts expected to perform well during hard times. The company has a customer base of lower-income people, and considering the impact of high inflation in the past two years, its customer base was expected to grow massively.

Instead, the opposite happened. The company’s low-income customer base was hit much harder by inflation and was forced to reduce even some essential purchases. It didn’t help that Dollar General’s stores were reported to be disorganized and understaffed.

As such, DG stock is down over 51.22% in the past year. It has made about a 15% recovery from its trough, and while further shocks could still happen, I think DG is a solid long-term buy. This is a recognizable name and is a brand with solid staying power. The store count is still increasing, and DG remains profitable.

Strategic initiatives such as “Back to Basics” and “Project Elevate” will likely improve the condition of its stores. Plus, analysts expect revenue growth to remain steady at around 4-5% in the coming years. EPS is expected to decline by 24% in FY2025 (ending in January), but a recovery is expected from then on.

The current price leaves very little room for more downside, and you’re also getting a 3% dividend yield while you wait for a recovery.

— Omor Ibne Ehsan

The old way of investing in tech giants is over. A NEW strategy unlocks 146X more income on the SAME underlying stocks (like Meta, Apple, and Amazon) -- WITHOUT options trading. Click here to uncover the NEW MAG-7 alternative.

Source: Money Morning