AI stocks across the board have been falling in the past week, and the bearishness surrounding AI stocks has only increased after Microsoft (NASDAQ:MSFT) started to cancel its data center leases. Wall Street is now scrutinizing AI stocks much more than usual, with AI stocks like Palantir (NASDAQ:PLTR) down almost 30% in the past five days. The Nasdaq Index has also broken below 19,000 points.

Nvidia (NASDAQ:NVDA) is likely the only thing that could cause a rebound in AI optimism if its earnings beat analyst expectations considerably. If that does not happen, the market could move into correction territory over the coming weeks.

That said, not all AI stocks are trading at nosebleed valuations right now. Many have declined well before the recent bout of uncertainty and they offer solid upside potential with relatively muted downside risk. Here are three such AI stocks to look into:

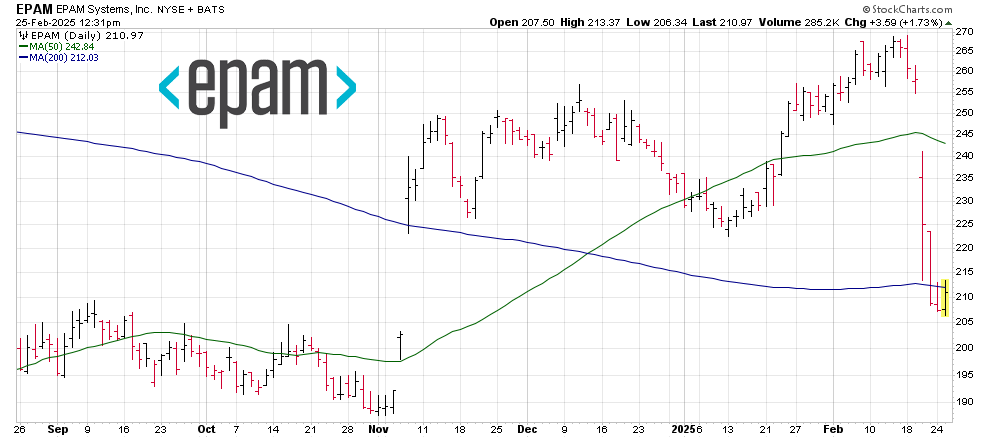

EPAM Systems (EPAM)

EPAM Systems (NYSE:EPAM) mainly offers software engineering services and has cloud/AI products for clients. Software Engineering services drive most of its revenue, but it is becoming more and more involved with AI and automation.

Like many high-tech stocks, it tumbled in late 2021 after a 200% rally from its pre-COVID prices and never recovered. The stock started 2025 on a good trajectory but it declined by over 20% after it posted disappointing financial guidance. For Q1 2025, EPAM guided for adjusted EPS of $2.22 to $2.32, below the $2.59 consensus. Full-year 2025 adjusted EPS guidance of $10.45–$10.75 also missed expectations of $11.32.

However, this is a profitable AI growth stock trading at less than 20 times forward earnings. This may be a good time to buy as most of the bearishness is priced in at around $200. The company grew its revenue at over 20% annually in the past three years and it is expected to continue growing its top line by double digits this year.

However, this is a profitable AI growth stock trading at less than 20 times forward earnings. This may be a good time to buy as most of the bearishness is priced in at around $200. The company grew its revenue at over 20% annually in the past three years and it is expected to continue growing its top line by double digits this year.

The consensus price target of $268.4 implies 26% upside.

UiPath (PATH)

You’d have to pay more for UiPath (NYSE:PATH), but it seems worth it as this company is heavily involved with automation software technology. It is a robotic process automation software company. The stock is down over 47% in the past year on top of the earlier decline since the 2022 tech selloffs.

The company’s CEO transition was unexpected in May 2024 when Rob Enslin departed and co-founder Daniel Dines came back, and this also coincided with a significant reduction (later raised) in full-year revenue guidance from $1.56 billion to $1.41 billion. Q2 2025 results showed improved metrics (e.g., 19% growth in ARR), but the stock’s rally stalled due to lingering skepticism about execution under new/returning leadership.

On top of that, despite later raising revenue guidance for FY2025 to $1.42 billion to $1.43 billion, analysts expect a decline in EPS.

On top of that, despite later raising revenue guidance for FY2025 to $1.42 billion to $1.43 billion, analysts expect a decline in EPS.

Nonetheless, the dip seems to be worth buying now as a lot of skeptics are doubting the company’s execution. The AI+robotics industry is just starting to take off high R&D could end up driving a resurgence if the automation boom sticks around. UiPath is still profitable and trades at 28 times forward earnings, along with revenue growth expected to be around double digits going forward. The consensus price target of $17.44 implies 39% upside.

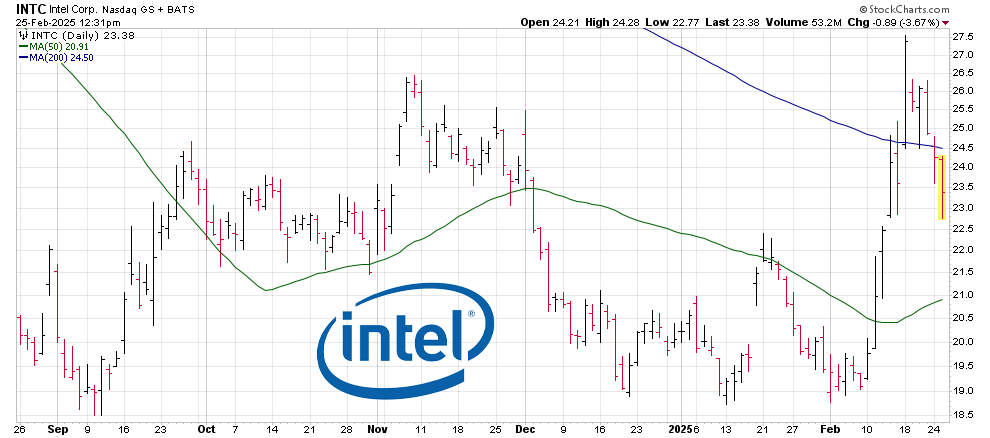

Intel (INTC)

Intel (NASDAQ:INTC) has been one of the biggest disappointments in the semiconductor sector. It is one of the biggest chipmakers, and you’d expect such a company to quickly catch up in AI chips, but that has not happened yet. Instead, both revenue and profits have been plunging, and the stock has slipped.

This doesn’t mean the entire business is bad. Intel’s parts are worth more than the whole, and most shareholders are starting to warm up to the idea of splitting the business. Broadcom (NASDAQ:AVGO) is exploring a bid for its CPU/GPU design teams and make Broadcom a direct competitor to Nvidia in the AI space. TSMC (NYSE:TSM) is also mulling a bid to acquire Intel’s fabrication plants internationally.

The latter may not go through, but if the discussions do turn more serious, the stock could deliver solid upside. It is now at a price where further downside risk is quite low, so betting on a potential break-up is a good idea.

The latter may not go through, but if the discussions do turn more serious, the stock could deliver solid upside. It is now at a price where further downside risk is quite low, so betting on a potential break-up is a good idea.

The consensus price target of $26.88 implies 15.1% upside.

— Omor Ibne Ehsan

Your 12 income checks supercharged with 21% yields [sponsor]Imagine having 12 new monthly income checks, carrying the potential of up to 21% yields.This is possible because of a tested strategy to get paid out regularly, like a paycheck. For over a decade, I have helped more than 26,000 investors secure 12 new monthly payouts. Meaning, you know exactly how much you'll make every month... Because of some stocks that pay us 8%,13.4%, and even 21.6% yields. See it for yourself here.

Source: Money Morning