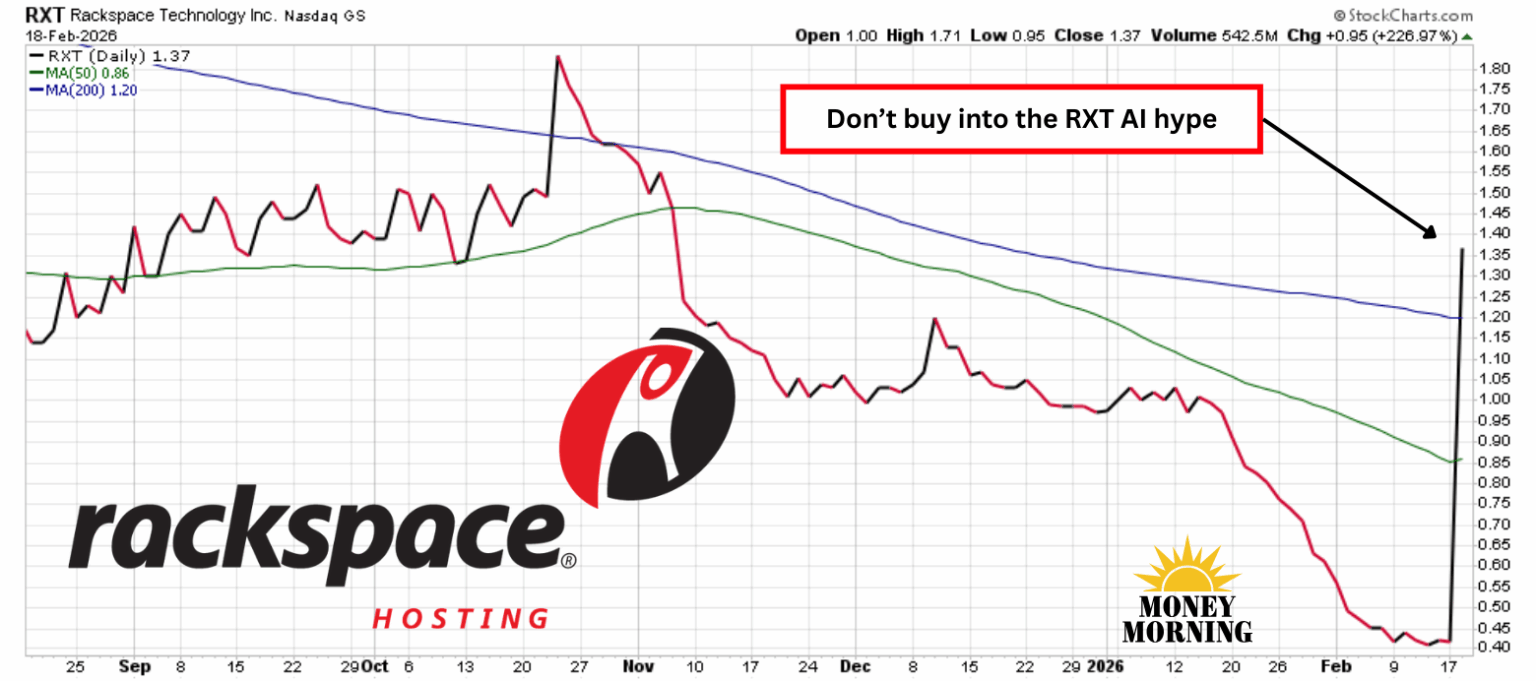

Rackspace Technology (RXT) shares skyrocketed 227% following Wednesday’s announcement of a strategic partnership with Palantir Technologies (PLTR). The stock, which had been languishing at around $0.42 per share, surged as investors reacted to the news of this AI-focused collaboration.

The deal positions Rackspace as a key provider of governed managed operations for Palantir’s Foundry data operating system and Artificial Intelligence Platform (AIP), encompassing implementation expertise, cloud hosting, data migration, and a secure operating model tailored for regulated industries. It leverages Rackspace’s private cloud and U.K. sovereign data centers to slash deployment times from months or years to weeks, accelerating AI adoption for enterprises.

While this partnership appears to validate Rackspace’s 25 years of expertise in managing mission-critical enterprise workloads and empowers Palantir to expedite Foundry and AIP rollouts, investors should still steer clear of RXT stock.

A History of Struggles

Rackspace was once a pioneering force in cloud computing, but today is a troubled entity plagued by stagnant or declining revenues, relentless losses, and a catastrophic erosion of shareholder value. After being taken private by Apollo Global Management in 2016, the company relisted in 2020 amid high hopes. Since then, RXT shares have plummeted over 95%, reflecting a dizzying collapse from its post-IPO highs and a stark testament to its fall from grace as a former cloud leader.

While the company saw growth early on, sales have since reversed course. By 2023, revenue dipped to $2.96 billion, followed by a further slide to $2.74 billion in 2024, marking consecutive years of contraction. Wall Street expects a decline for 2025 to $2.68 billion. Intensifying competition in cloud services, where giants like AWS and Azure dominate, leave smaller players like Rackspace scrambling for scraps.

Compounding the revenue woes are persistent operating losses. Rackspace has reported quarterly net losses for years, with no signs of profitability on the horizon. While net losses significantly narrowed through Q3 of 2025, next week’s earnings aren’t expected to produce a profit either. Even the company’s founder, Richard Yoo, warned in 2023 that Rackspace was “on a trajectory of death. It will not be around.”

The Palantir deal threw Rackspace a life preserver, but there are substantial doubts about its ability to execute.

Financial Precariousness Raises Doubts

Financial Precariousness Raises Doubts

Capitalizing on the partnership is hampered by Rackspace’s precarious balance sheet. The company carries approximately $2.76 billion in long-term debt, contributing to total liabilities exceeding $4 billion against just $3 billion in assets. This imbalance results in a negative equity position, with a debt-to-equity ratio in the red, signaling severe financial leverage risks. Cash reserves stood at just $144 million at the end of Q3, barely sufficient for aggressive expansion amid ongoing cash burn.

The partnership also highlights Rackspace’s limited readiness: it currently employs only 30 Palantir-trained engineers for data migration and problem-solving. Plans to scale this to over 250 within 12 months sound ambitious, but given the firm’s dicey finances and history of cost-cutting, doubts about its chances of success are rampant. Multiple CEO changes since 2019 further undermines confidence in strategic execution.

Bottom Line

The explosive surge in RXT shares after the Palantir deal is largely fueled by AI hype, not sustainable fundamentals. With years of declining revenue, mounting losses, and financial constraints, this is no bargain – it’s a gamble. There are plenty of profitable, growing AI players like Palantir itself to invest in and not risk losing your money.

— Rich Duprey

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning