Micron Technology (MU) is one of the biggest memory chipmakers globally. It sells DRAM, NAND flash, and SSDs. All of these are required for data centers, phones, laptops, desktops, and even cars. The industry has followed a cyclical trajectory for decades, with MU stock surging whenever supply is tight.

However, things are changing, and this bullish cycle may last much longer than you may assume. The company’s primary competitors are Samsung and SK Hynix, both based outside the U.S. It is no longer a commodity bet as memory demand is high and foreign competitors are facing pressures due to the U.S. nearshoring and onshoring trends, plus tariffs.

In fact, Micron has sold out its entire high-bandwidth memory (HBM) capacity through 2026 with fatter margins. Cloud vendors (AWS, Azure, Google) are in a capex arms race, and accelerating orders are expected in the coming years.

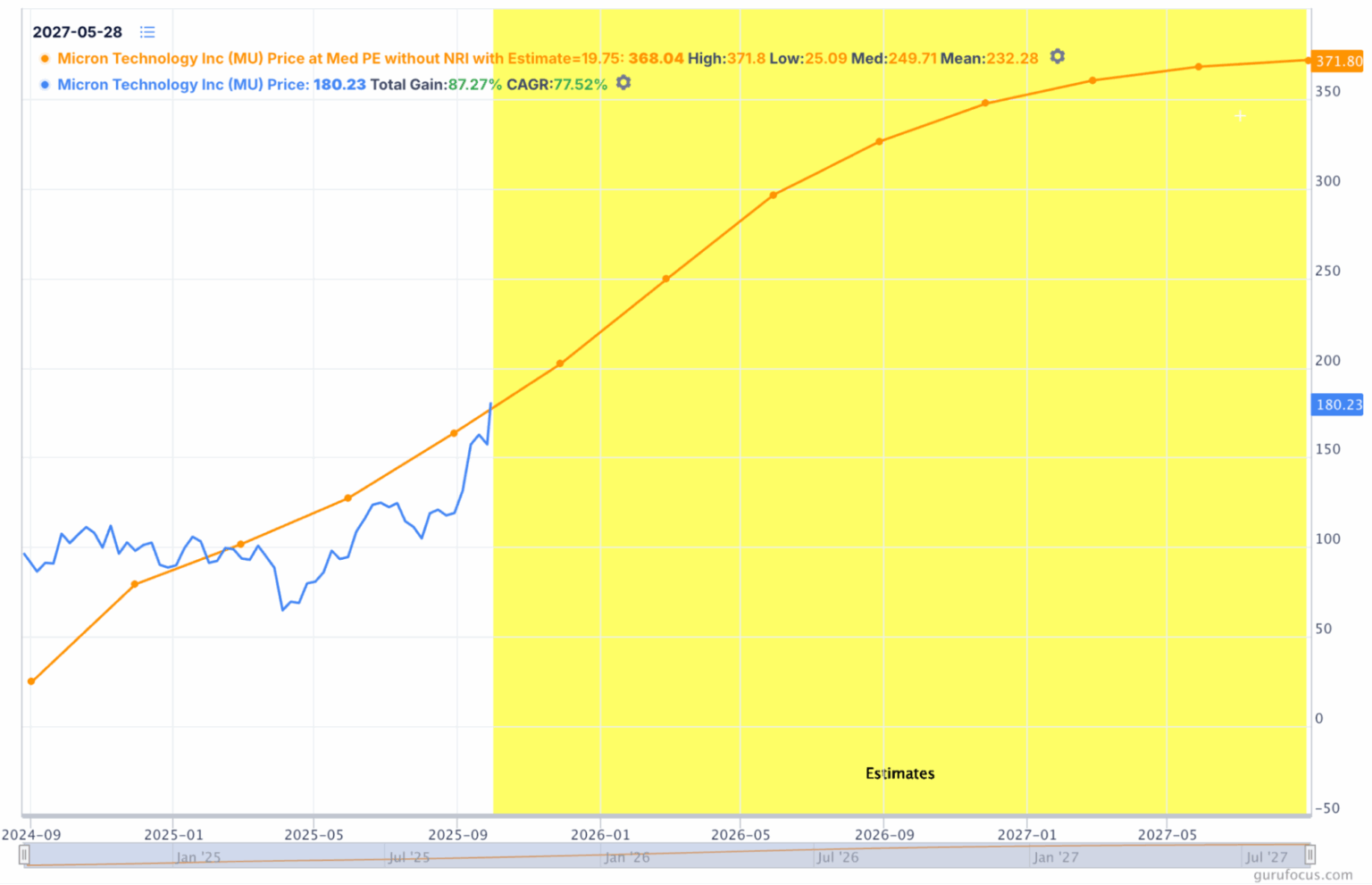

Will MU stock reach $300?

I believe MU stock could surpass $300 as early as mid-2026.

The growth is stellar, and investors are paying just 11 times forward earnings for the stock. Historically, this would have been a fair price due to Micron’s slow 3-year revenue growth rate of 6.6% annually, but the multiple does not make much sense today.

The growth is stellar, and investors are paying just 11 times forward earnings for the stock. Historically, this would have been a fair price due to Micron’s slow 3-year revenue growth rate of 6.6% annually, but the multiple does not make much sense today.

Micron posted 46% year-over-year revenue growth in its Q4 2025 earnings report with a 28.3% net income margin. Analysts expect the high growth to continue in the coming years if hyperscaler CapEx continues ballooning, so the stock could easily double or more in a scenario where Micron can sustain double-digit sales growth.

— Omor IE

— Omor IE

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning