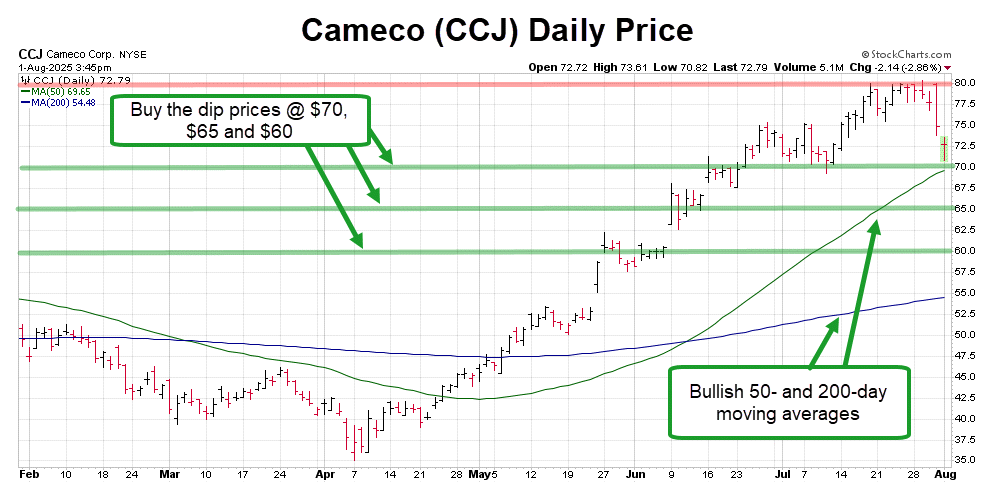

Shares of Cameco (CCJ) have lost 10% since their latest earnings results. The move is generating a potential buy the dip opportunity for investors following this healthy correction generated by a “sell the news” reaction to positive earnings.

For the latest quarter, Cameco beat Q2 expectations with EPS of CAD0.71 (vs. CAD0.51 est.) and revenue of CAD877M, up 47% year-over-year.

Management reaffirmed its overall 2025 financial outlook but significantly raised guidance for the Westinghouse segment due to higher expected revenue from the Dukovany project, the first nuclear power plant built on Czech territory.

Cameco owns a 49% stake in Westinghouse Electric Company, with the remaining 51% held by Brookfield Renewable Partners (BEP) and its institutional partners.

Westinghouse’s 2025 adjusted EBITDA forecast was raised to $525M–$580M (from $355M–$405M), with net earnings now projected at $30M–$80M, reversing a prior loss outlook.

Despite the strong earnings update, Cameco shares dropped more than 10% from recent highs heading into the call, an example of a classic “sell the news” move.

This happens when good news is fully priced in ahead of an event. Early buyers and traders often take profits after the event, creating short-term downside pressure despite bullish fundamentals.

The pullback also fits the definition of a healthy correction within a broader uptrend. Shares are now trading near $70, which is likely to act as technical support for two reasons:

- Round-number support – $70 served as resistance in late June and early July and is now a logical area for buyers to step in.

- 50-day moving average – The trendline sits just below current levels and has remained in a strong bullish slope since early May, ahead of Cameco’s 67% rally.

Bottom Line:

Bottom Line:

Cameco’s bullish trend remains intact. The current pullback offers a “buy the dip” setup with $70 as key support. A rebound from here could target $100 over the next six months.

If $70 breaks, additional support is expected at $65 and $60—each level presenting long-term investors with attractive entry points to dollar-cost average into the position.

— Chris Johnson

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning