The market baked in blockbuster expectations for Amazon‘s (AMZN) Q2 2025 earnings. This is mainly due to Microsoft (MSFT) and Meta Platforms (META) reporting unprecedented beats earlier this week. Naturally, one would expect Amazon to do even better, as AWS is the largest cloud computing platform.

Amazon ended up beating, but not to the extent the market expected. Amazon reported $167.7 billion in sales, up 13% year-over-year from $148 billion in the year-ago quarter. Analysts expected $162.1 billion. EPS also beat expectations of $1.33, as Amazon posted $1.68 per share vs. $1.26 in the year-ago quarter.

Why AMZN stock still declined

AWS-derived revenue is to blame specifically. It grew 17.5% year-over-year to $30.9 billion, slightly above estimates of $30.7 billion, and contributed $10.2 billion in operating income (over half of Amazon’s total). In comparison, Microsoft’s Azure grew 39% year-over-year and sees another 30%+ gain next quarter.

On the other hand, Amazon sees 10-13% year-over-year sales growth in Q3. This implies that AWS is not expected to grow at the rate of its biggest counterparts anytime soon.

As such, Wall Street’s problem is that Amazon’s massive CapEx is not translating into growth fast enough. Amazon plans to ramp up capital expenditures to over $100 billion this year.

It’s not the be-all and end-all for Amazon.

It’s not the be-all and end-all for Amazon.

Amazon’s exposure to AI may be overestimated by the market, since, unlike Microsoft and Google, Amazon does not have a suite of software products to integrate AI into, and its own AI models are quite obscure. The main generative AI exposure comes from other AI companies that need capacity.

A beat is a beat regardless, and the company still has more room to rectify this shortcoming. AWS’ backlog increased 25% to $195 billion in Q2, and as CapEx translates into more capacity, it will eventually translate into more revenue. Microsoft still outshines Amazon here, with $368 billion in contracted backlog across its cloud platforms.

Azure may surpass AWS, but investors will still reward AMZN stock for the growth it has.

Should you buy the dip on AMZN stock?

You are paying less than 33 times earnings for AMZN stock after the recent 8.5% plunge. This is far less than the historical median of over 90 times earnings. The bottom-line progress has been solid so far, and even if Wall Street keeps paying 33 times trailing earnings, the stock should comfortably outperform the broader market if earnings expectations are matched.

It’s more likely that investors will pay more for the stock as growth gains steam, and Amazon will keep outperforming estimates. Analysts have remained bullish, with top analysts raising their price target despite the stock sinking. The highest price target on AMZN stock is $305 now.

It’s more likely that investors will pay more for the stock as growth gains steam, and Amazon will keep outperforming estimates. Analysts have remained bullish, with top analysts raising their price target despite the stock sinking. The highest price target on AMZN stock is $305 now.

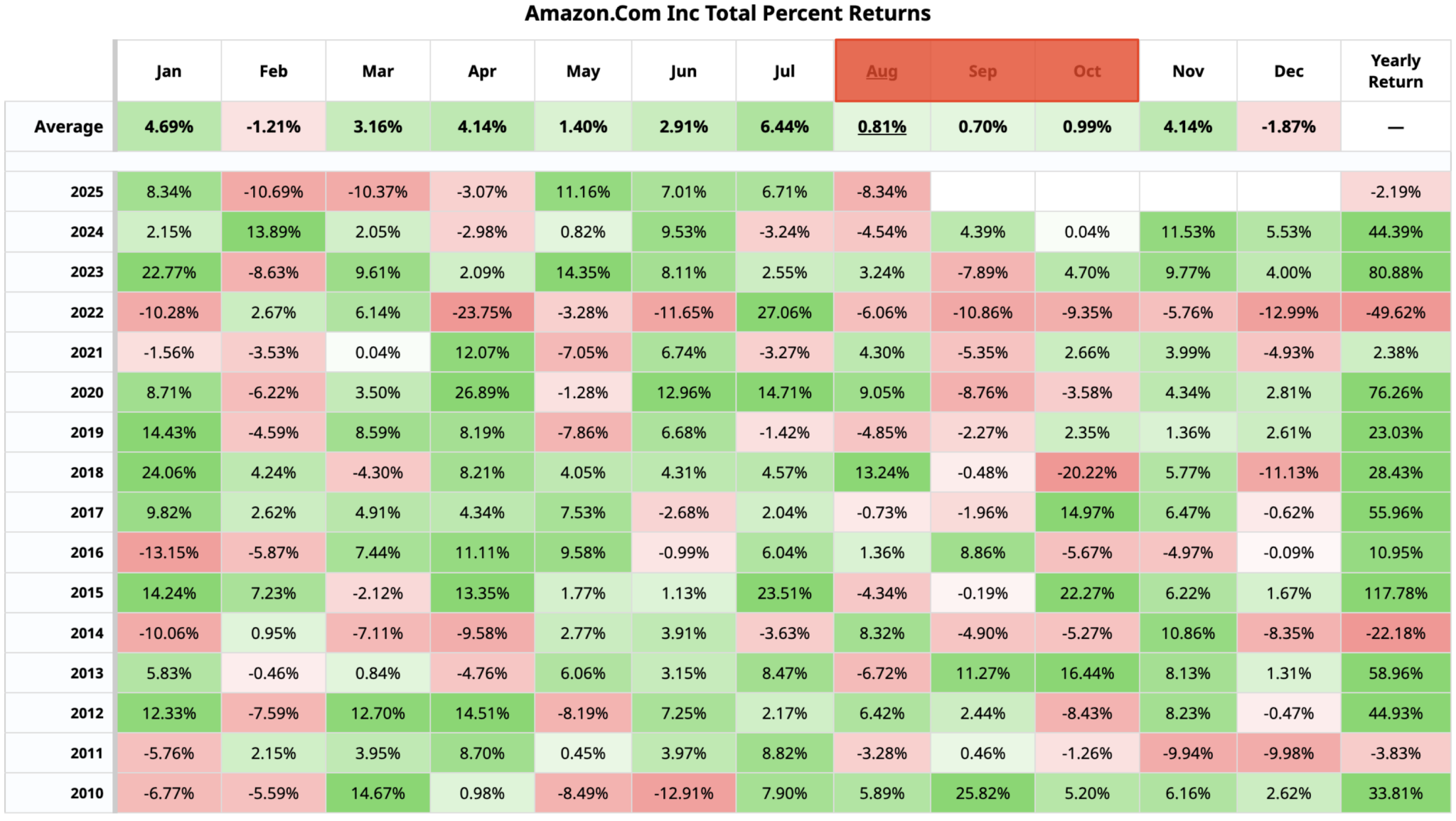

Anyhow, I would stay a little more careful in the short term. The stretch from August to October has been less than ideal for AMZN stock.

The decline today is a continuation of this trend. However, a decline in August also means it’s more likely that the worst of the summer is behind us. I lean bullish and see AMZN stock well above $240 by the end of this year if the broader economy cooperates.

The decline today is a continuation of this trend. However, a decline in August also means it’s more likely that the worst of the summer is behind us. I lean bullish and see AMZN stock well above $240 by the end of this year if the broader economy cooperates.

— Omor IE

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning