If you are still looking at NVIDIA (NVDA) as the next big thing in AI you’re going to miss the real opportunity.

The next great boom in artificial intelligence isn’t about who builds the engine, it’s about who builds the car that the engine drives.

While NVIDIA and AMD (AMD) are dominating headlines for their breakthrough chips, the real story for investors is unfolding one layer higher. A new generation of AI service companies is emerging to bring that compute power to the world. These companies are now providing better profit opportunities for investors than NVIDIA as a result.

Think of it this way: if NVIDIA is building the internal combustion engine of the AI age, companies like CoreWeave (CRWV) , Vultr, Oracle (ORCL) , and IBM (IBM) are building the cars. They’re taking raw GPU power and turning it into infrastructure – packaged, scalable, and accessible – for businesses that don’t have the time, talent, or capital to build their own data centers.

This is the access layer of AI.

Just as Amazon Web Services turned cloud computing into a utility, these companies are poised to do the same for generative AI.

In the process, they will unlock the next multi-trillion-dollar wave of innovation, not just for tech giants, but for every industry that touches data.

Why AI Compute Is the New Utility

For most businesses, the problem isn’t building AI models, it’s getting access to the power needed to run them.

Training large language models, running generative simulations, or deploying recommendation engines all require massive GPU compute power. But that infrastructure is expensive, complex, and in short supply.

That’s where this new wave of AI service companies comes in.

Firms like CoreWeave and Vultr are stepping into the gap, offering plug-and-play access to NVIDIA (NVDA) and AMD (AMD) chips without the burden of hardware ownership. They’re building the backend so the rest of the world can build AI products.

This is more than cloud computing—it’s purpose-built infrastructure for the AI economy.

Just like electricity or bandwidth became modern utilities, AI compute is now on the same path. And the companies who deliver it – efficiently, reliably, and scalable- are becoming the new power brokers.

How Investors Can Play This Trend

Wall Street is catching on quickly.

On Monday, Vultr, a privately held cloud provider, announced a $329 million debt raise from a syndicate including Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, KeyBank, and Wells Fargo.

The company didn’t disclose the interest rate but noted that it was “dramatically lower” than past deals. That signals that institutional investors now see GPU infrastructure as an investable, scalable asset class. They want in early, which is why Vultr got attractive rates for the debt.

Compare that to CoreWeave, which raised $2 billion in debt last month at 9.25%, down from 14% in 2023. That kind of rate compression shows two things: one, demand is growing. Two, lenders believe these businesses are maturing fast.

Compare that to CoreWeave, which raised $2 billion in debt last month at 9.25%, down from 14% in 2023. That kind of rate compression shows two things: one, demand is growing. Two, lenders believe these businesses are maturing fast.

Even as Microsoft and Amazon spend tens of billions in cash on their AI infrastructure, smaller, focused players like Vultr and CoreWeave are tapping the debt markets to scale rapidly.

Unlike the chipmakers, these firms are building recurring-revenue platforms to serve as the infrastructure for the AI economy.

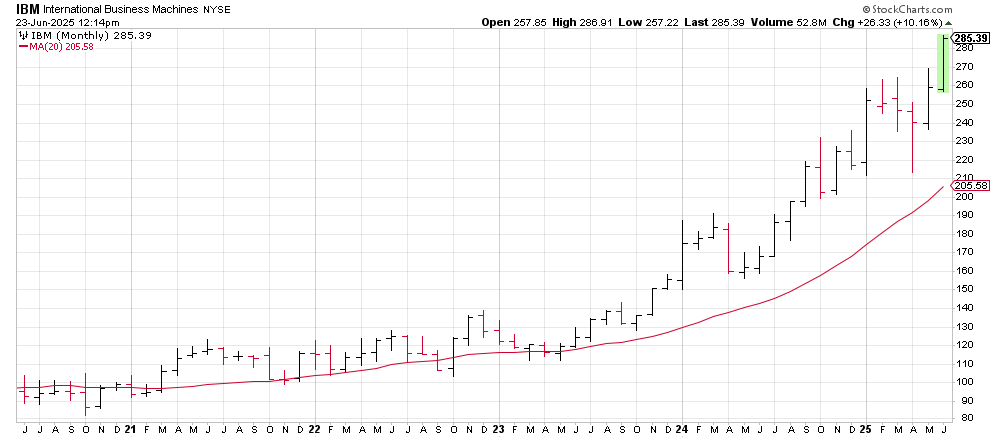

This trend isn’t just about speculation. IBM, often overlooked in this space, has quietly become one of the best-performing AI service stocks of the past year.

The Overlooked Operator in the AI Infrastructure Boom

While investors chase the high-growth names renting out racks of H100s, IBM has quietly carved out a critical role in the AI ecosystem, just not where most people are looking.

IBM isn’t competing with CoreWeave or Vultr to be the fastest GPU hyperscaler. Instead, IBM is focused on enterprise-grade AI deployments through its watsonx.ai platform and a deep partnership with NVIDIA.

This makes it the preferred provider for businesses in highly regulated industries like finance and healthcare that need trust, compliance, and integration, not just raw speed.

Just last week, Dan Ives of Wedbush Securities raised his price target on IBM, noting its rising importance as an “unexpected operator” in the AI boom. IBM shares have quietly gained 70% over the past year, far outpacing even NVIDIA, which is up just 14% over the same period.

For what its worth, we presented the IBM AI Underdog investment opportunity in January 2024 and maintain the company’s bullish outlook with a price target of $350.

IBM won’t deliver 10x gains overnight, but it may become one of the most reliable infrastructure names in the entire AI trade.

Three Ways to Invest in the AI Services Boom

Three Ways to Invest in the AI Services Boom

Here’s a quick look at three of the most important companies shaping the AI service layer—and how each fits into the broader infrastructure story.

IBM: The Enterprise Layer

IBM has emerged as the trusted AI service provider for legacy industries. With watsonx.ai, NVIDIA partnerships, and a hybrid cloud stack built for compliance, IBM is enabling AI deployment inside the world’s most complex organizations.

- Use case: Regulated enterprise AI, secure hybrid cloud

- Customer base: Finance, healthcare, government

- Edge: Trust, integration, and consistent profitability

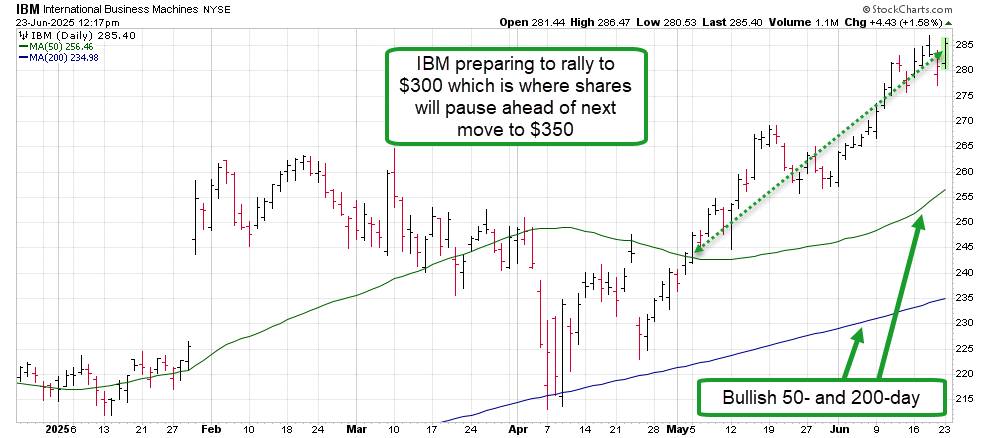

Shares of IBM are trading in a strong long-term bull market trend as the stock approaches the $300 price. Investors should expect to see some technical resistance at $300 as round-numbered resistance will be strong, but the break above that price will target IBM’s next rally to $350.

How do you invest in IBM?

How do you invest in IBM?

Long-term investors can take one of two approaches to investing in the bullish trend of IBM stock.

- Simple buy and hold strategy.

- Long-term LEAPs option strategy

- The January 15, 2027 $300 calls currently trade for $3,870 per contract.

- A move to our price target of $350 by the end of 2025 would value these options at $7,079, a profit of 82.9% based on theoretical (Black Scholes Model) pricing.

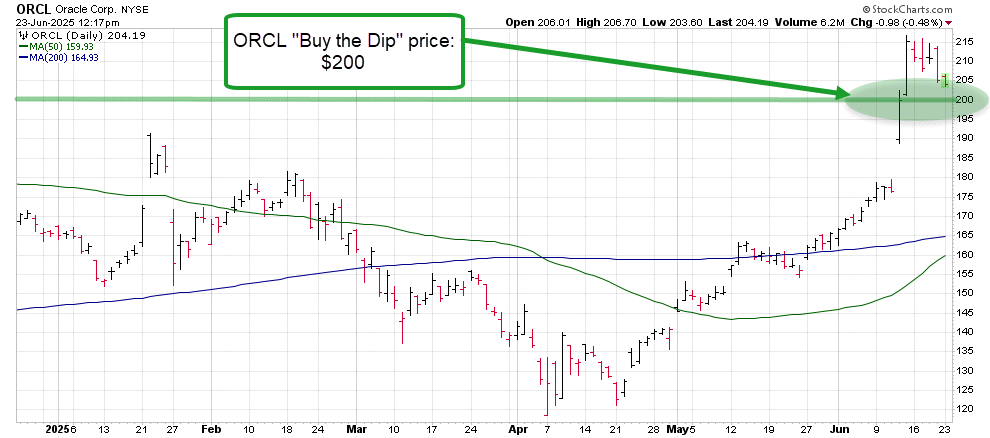

Oracle (ORCL): The AI-Optimized Cloud

Oracle is making an aggressive push into AI by combining its strength in enterprise data with a next-gen cloud stack purpose-built for AI training. Its close collaboration with NVIDIA and Cohere gives it a unique foothold as the enterprise cloud alternative to AWS and Azure.

- Use case: Data-rich AI training and deployment

- Customer base: Global enterprises, especially in ERP and data-heavy sectors

- Edge: AI + structured data + GPU infrastructure = enterprise moat

Like IBM, Oracle has been on a long-term bull market run that is now outpacing the likes of NVIDIA and AMD. The companies expanding business to compete with AWS and Microsoft, both of which ORCL shares are outperforming.

After a long-term consolidation in ORCL stock price, shares are now on the cusp of a new bullish run as momentum is increasingly bullish.

Oracle shares are preparing to complete a new Golden Cross patter over the next few weeks. That completed Golden Cross will forecast stronger momentum and higher prices for the next 3-6 months.

How do you invest in ORCLE?

How do you invest in ORCLE?

Like IBM, investors should take a long-term outlook on Oracle shares as their trends strengthen.

A buy and hold approach puts investors in position to benefit from the stock making a run to our price target of $265 over the next 12 months.

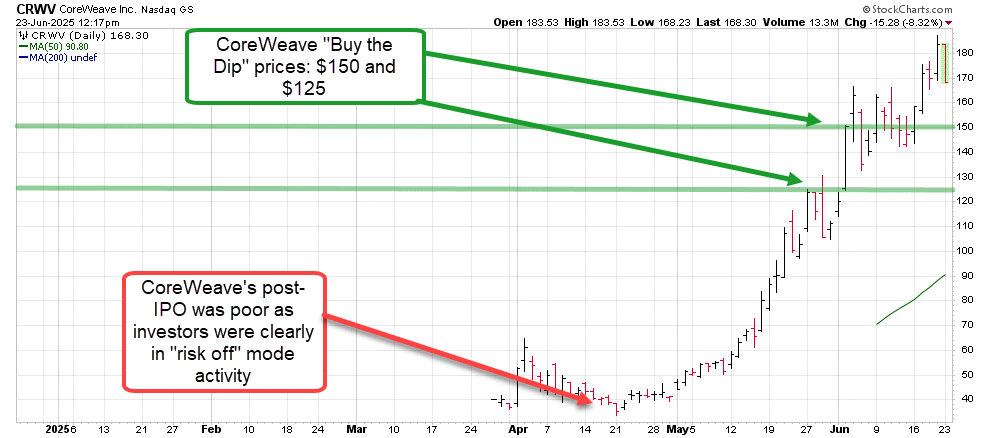

CoreWeave (CRWV): The AI Hyperscaler

CoreWeave is the poster child of the AI infrastructure boom. With over 250,000 GPUs across 30+ data centers, billion-dollar contracts with OpenAI and Microsoft, and the backing of NVIDIA, it’s building the backbone of the generative AI era.

- Use case: Training/inference for LLMs and genAI platforms

- Customer base: AI labs, hyperscalers, SaaS builders

- Edge: Scale, speed to market, deep GPU supply chain integration

How do you invest in CoreWeave?

CoreWeave presents itself as a perfect “buy the dip” opportunity.

Shares have exploded 400% since their lows posted in April as investos have clawed their way into the stock for fear of missing out, In May, the company posted earnings results that were below Wall Street’s expectations, but investors were more impressed with CoreWeave’s 400+% year-over-year revenue growth as the company is heavily in expansion mode.

Investors will want to watch for an opportunity to buy the dip on CoreWeave as the company pulls back from its highs to $150.

That $150 price was the last strong consolidation that CoreWeave stock has seen and should serve as support. Further declines would likely target $125, which would serve as the next “buy the Dip” price trigger.

Vultr: The IPO to Watch

Vultr: The IPO to Watch

While still private, Vultr may be the dark horse of the AI infrastructure trade. The recent $329 million debt raise—led by some of Wall Street’s biggest banks—signals strong confidence in the company’s balance sheet and business model. Vultr claims the new credit facility is priced hundreds of basis points lower than CoreWeave’s, suggesting strong operational performance and profitability.

With over 1.5 million customers across 32 global data center regions, and backing from AMD in a $333 million round that valued the company at $3.5 billion, Vultr is rapidly scaling its platform. It rents out GPUs from both AMD and NVIDIA and focuses on small-to-medium businesses and developers looking for high-performance AI compute at a lower cost.

The company hasn’t confirmed its timeline, but a second-half 2025 IPO is now looking increasingly likely. If that happens, Vultr will become one of the first pure-play public investments in the emerging GPU cloud service sector.

The AI Service Bottom Line

We’re entering the second chapter of the AI era. The chips were the first story. But now comes the infrastructure—how those chips are accessed, monetized, and scaled.

Companies like CoreWeave, Oracle, IBM, and Vultr are laying down the rails for the next AI boom. And just like AWS built the backbone of the internet economy two decades ago, this new breed of AI service providers may be laying the groundwork for the next one.

Smart investors should be watching this list closely, because the next biggest winners in AI might not be the chipmakers. They will be the ones who make those chips usable by the rest of the world.

— Chris Johnson

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning