If you’re like me, when you see an outsized dividend yield, you stop and immediately do the mental math. How much would we get back in payouts from, say, a 9.3% payer if we were to invest $10,000? Or $20,000? Or $100,000?

But savvy contrarians we are, we know to push back on this initial reaction and look deeper.

That’s because of something I know pretty much goes unsaid among contrarian income investors like us: Those big yields can be (and usually are) a danger sign. Truth is, a rising dividend is only one possible reason for a high payout.

And in fact, it’s the least likely one.

More often, a high yield stems from something we want no part of: a plunging share price. Consider Vail Resorts (MTN), with a current yield of around 6% as I write this.

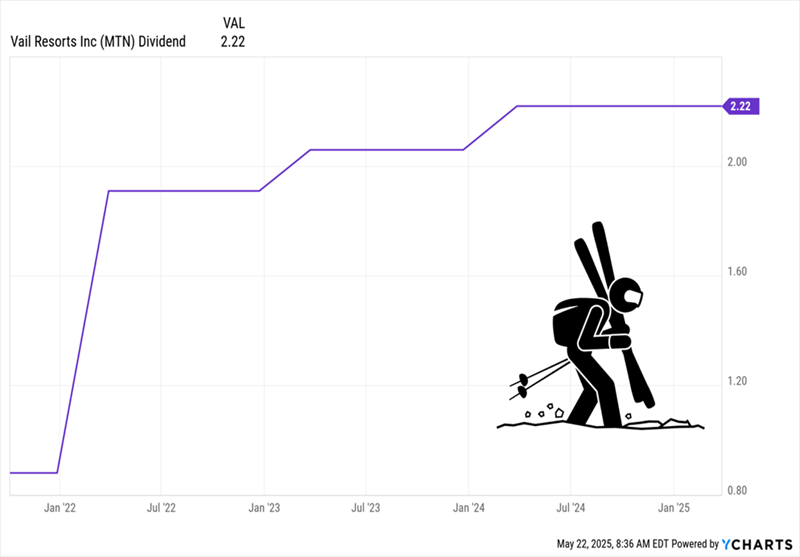

Sounds great, right? Too bad the high current yield papers over a litany of problems. The first? Slowing dividend growth (indeed, it’s come to a stop!) as inconsistent winters hamper visits to its resorts.

MTN’s Dividend Goes Back to the Bunny Hill

The (literally!) tough climate has put pressure on MTN’s free cash flow (FCF), resulting in a jump in its payout ratio: As I write this, Vail’s payout occupies an uncomfortable 84% of the last 12 months of FCF.

The (literally!) tough climate has put pressure on MTN’s free cash flow (FCF), resulting in a jump in its payout ratio: As I write this, Vail’s payout occupies an uncomfortable 84% of the last 12 months of FCF.

If you’re looking for one main reason for the slowdown in payout growth, that’s it.

The company is also still reckoning with the aftermath of a strike by ski patrollers at its Park City, Utah, resort last season, resulting in closed lifts and long lineups. Worse, the work stoppage came right in the middle of the year-end holidays—adding to the PR nightmare.

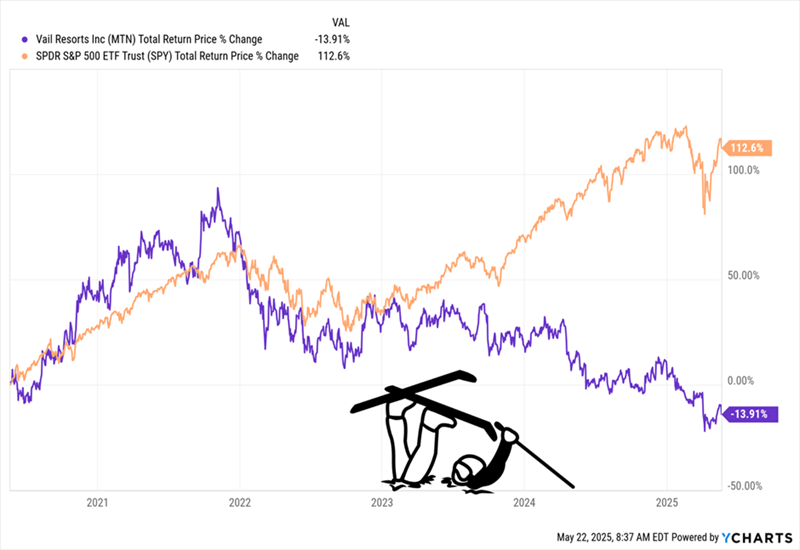

With all that in mind, it’s not hard to believe that the stock has drastically underperformed the market: Even when you include reinvested dividends, MTN’s total return is 14% in the red in the last five years—while the S&P 500 returned 113%!

6% Yield Fails to Make Up for “Downhill” Total Return

This is all a (perhaps long winded!) way of saying we need to look beyond the shiny veneer of a high yield. I’ve got a proven tool for doing just that, which we’ll get into next. We’ll also delve into two “authentic” dividend growers for you to consider, too.

This is all a (perhaps long winded!) way of saying we need to look beyond the shiny veneer of a high yield. I’ve got a proven tool for doing just that, which we’ll get into next. We’ll also delve into two “authentic” dividend growers for you to consider, too.

Shareholder Yield Beats Dividend Yield in Every Way

At the end of the day, a dividend stock has three ways to pay us:

- Its current payout: This, of course, is the dividend we get after we buy.

- Dividend growth, which increases the yield on our original buy and acts like a “magnet” on the share price, with the rising payout pulling the share price up.

- Share buybacks, which cut the number of shares outstanding, juicing earnings per share and other per-share metrics.

Buybacks get a bad rap, but they shouldn’t, because when they’re done right (i.e., when the stock is cheap), they can seriously juice our returns. This is another problem with the current yield—it tells us nothing about this buyback effect.

This is where my favorite measure of how much a company is rewarding shareholders comes in. It’s called shareholder yield, and it includes buybacks and dividends.

Visa’s Shareholder Yield Crushes Its “Headline” Yield

To see it in action, let’s consider payment-processing giant Visa (V), a holding in my Hidden Yields dividend-growth advisory. The stock really does nothing but move up and to the right, powered by global economic growth and its “tollbooth” role on the rising tide of digital payments.

Unfortunately, most investors miss out on this megatrend-powered stock because they look at its low current yield—just 0.66% as I write this—and move on.

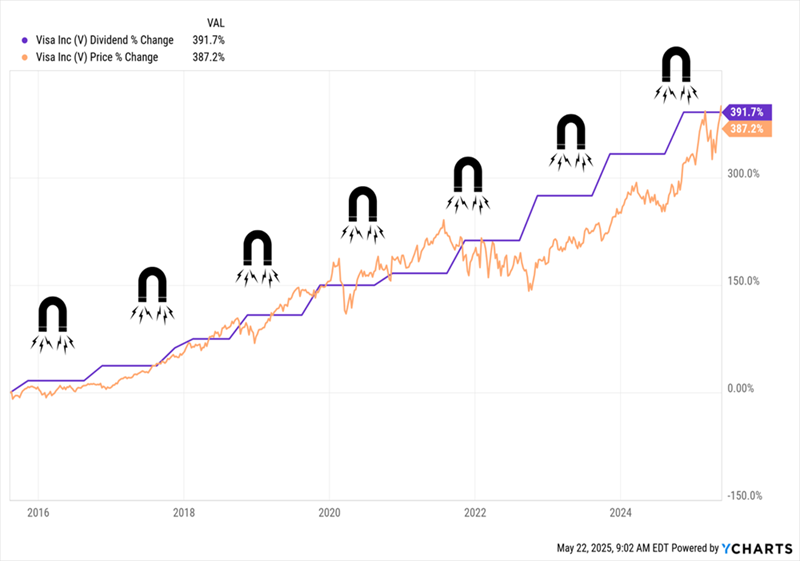

But let’s ignore that for a second and zero in on Visa’s payout growth, which has been strong: The dividend is up 392% in the last decade. It’s no coincidence that the share price has gained almost the exact same amount:

Visa’s “Dividend Magnet” in Action

And because of that payout growth, investors who bought Visa a decade ago are yielding 3.4% on their original buy now. Sure, that doesn’t exactly knock our socks off, but it is five times greater than today’s 0.66% current yield.

And because of that payout growth, investors who bought Visa a decade ago are yielding 3.4% on their original buy now. Sure, that doesn’t exactly knock our socks off, but it is five times greater than today’s 0.66% current yield.

Now let’s move on to buybacks: Visa has taken 21% of its shares off the market in the last five years, making all those per-share metrics look better. By the way, if you don’t think buybacks matter, check out how Visa’s share price took off starting in early 2024, when management really amped up its buyback action:

Share Count Dives, Stock Price Soars

The beautiful thing about shareholder yield is that it combines all three types of shareholder rewards: current dividend, payout growth and buybacks. Let’s look at how to calculate it—then I’ll drop a stock with an even higher shareholder yield.

The beautiful thing about shareholder yield is that it combines all three types of shareholder rewards: current dividend, payout growth and buybacks. Let’s look at how to calculate it—then I’ll drop a stock with an even higher shareholder yield.

How to Calculate Shareholder Yield

To calculate shareholder yield, take the amount a company spent on share repurchases in the preceding 12 months, deduct any cash brought in through share issuances, then add in the total spent on dividends.

You then take that sum and divide it into the company’s market cap, or the value of all its outstanding shares.

In Visa’s case, that comes out to $4.43 billion spent on dividends and $18.98 billion spent on buybacks, for a total of $23.4 billion in total shareholder returns in the 12 months ended March 31, 2025.

With a $686.4-billion market cap, we can say that Visa sports a 3.4% shareholder yield—again about five times more than the current dividend yield of 0.66%.

Now, in light of Visa’s strong recent gains—and the fact that its share price has caught up to its payout growth (we prefer a lag for extra “snap back” upside”)—we consider Visa a “hold.” But that’s not the case for our next shareholder-yield champ, which is a smart “buy” now.

Beyond Visa: This Stock Delivers an Eye-Popping 8.7% Shareholder Yield

ConocoPhillips (COP) is an oil producer and explorer that’s primed to thrive under Trump 2.0’s drive to drill. With permit approvals likely returning to the breakneck pace of 2018 to 2020, COP is near the top of the winners’ list here.

That, in turn, will help drive up the dividend, which yields 3.6% and whose growth has been flat for more than a year. The stock will get an assist from the company’s ultra-safe dividend payout ratio of about 42% of its last 12 months of FCF.

Meantime, COP’s shareholder yield is far higher than the 3.6% yield on its dividend alone. In the last 12 months, COP spent $3.7 billion on dividends and $5.7 billion on buybacks, for a total of $9.4 billion on all shareholder rewards. Divide that by COP’s $107.8-billion market cap and you get a shareholder yield of 8.7%

Management’s shareholder friendliness is one reason to like the stock. Its bright future as permitting accelerates is another. Both set up a timely opportunity to buy.

— Brett Owens

URGENT: Our 2 Top Buy Signals Just Flashed BUY on These 5 Stocks [sponsor]

As we just saw, when you combine a high shareholder yield and a powerful “Dividend Magnet” and you get something very special indeed: Two proven indicators that can point you to the next big winners in dividend stocks.

These two unloved “profit signals” are, in fact, the key to my dividend-investing strategy. They’ve helped me guide my readers to BIG winners, like:

- TD Synnex (SNX), with an 83% total return in just 3 years.

- Concentrix (CNXC), which handed us 111.8% in just 1 year, and …

- Texas Instruments (TXN), which returned a stellar 148% in 5 years!

We’ve done it with far less risk than investors who’ve chased the latest “hot” tech stock—or (heaven forbid) the newest meme coin.

The best news? Right now, I’m zeroing in on 5 other stocks poised to ride their powerful Dividend Magnets (and strong shareholder yields) to new heights.

I’ve zeroed in on 5 more stocks poised to ride their Dividend Magnets—and impressive shareholder yields—to new highs. Click here and I’ll give you my full strategy in a free investor briefing. You’ll also get to download an exclusive Special Report that unmasks all 5 of these accelerating dividends.

Source: Contrarian Outlook