The market has taken a sledgehammer to many growth stocks over the past two years. The Nasdaq and the Russell 2000 are both sitting below their year-to-date levels despite the recent bounce. Plus, a handful of mega-caps have continued dominating the market after the tariff pause news.

A hypersensitive Wall Street is punishing every earnings shortfall. Pzena Investment Management calculated that the price hit for companies that miss estimates is running at a 30‑year high.

I believe the pendulum is set to swing because valuation gaps this high rarely stick around for too long. Even if the underperformance from these companies continues, they are unlikely to be too bad at these lows. It’s worth being aggressive on some growth stocks during dips. Here are three:

Trade Desk (TTD)

The Trade Desk (NASDAQ:TTD) has been a screaming buy ever since it crashed in the first three quarters of the year. I’ve recommended buying the dip as it bottomed out, and it is up almost 60% from its trough now. The recovery is still far from over.

The Trade Desk (NASDAQ:TTD) has been a screaming buy ever since it crashed in the first three quarters of the year. I’ve recommended buying the dip as it bottomed out, and it is up almost 60% from its trough now. The recovery is still far from over.

Investors overreacted when the company missed its own guidance in Q1, and the spook was warranted since The Trade Desk has been known to outperform expectations quarter after quarter. But the market only acted on one quarter being bad, and Trade Desk went on to restart beating estimates with its most recent quarterly report. It beat EPS estimates by 33.2%, and revenue estimates were beaten by 7.1%. That trend is likely to continue.

The stock is still down 47% from its peak and has plenty of upside potential. The earnings multiple still looks expensive at 90 times, but investors have historically paid 145 times earnings for TTD stock. 3-year EBITDA growth is at 45.2% annually, and it is better than 85% of all companies in the software industry. Paying ahead for that growth is not a bad idea.

The consensus price target of $87.88 implies 18.93% upside, but price targets go as high as $135.

CAVA Group (CAVA)

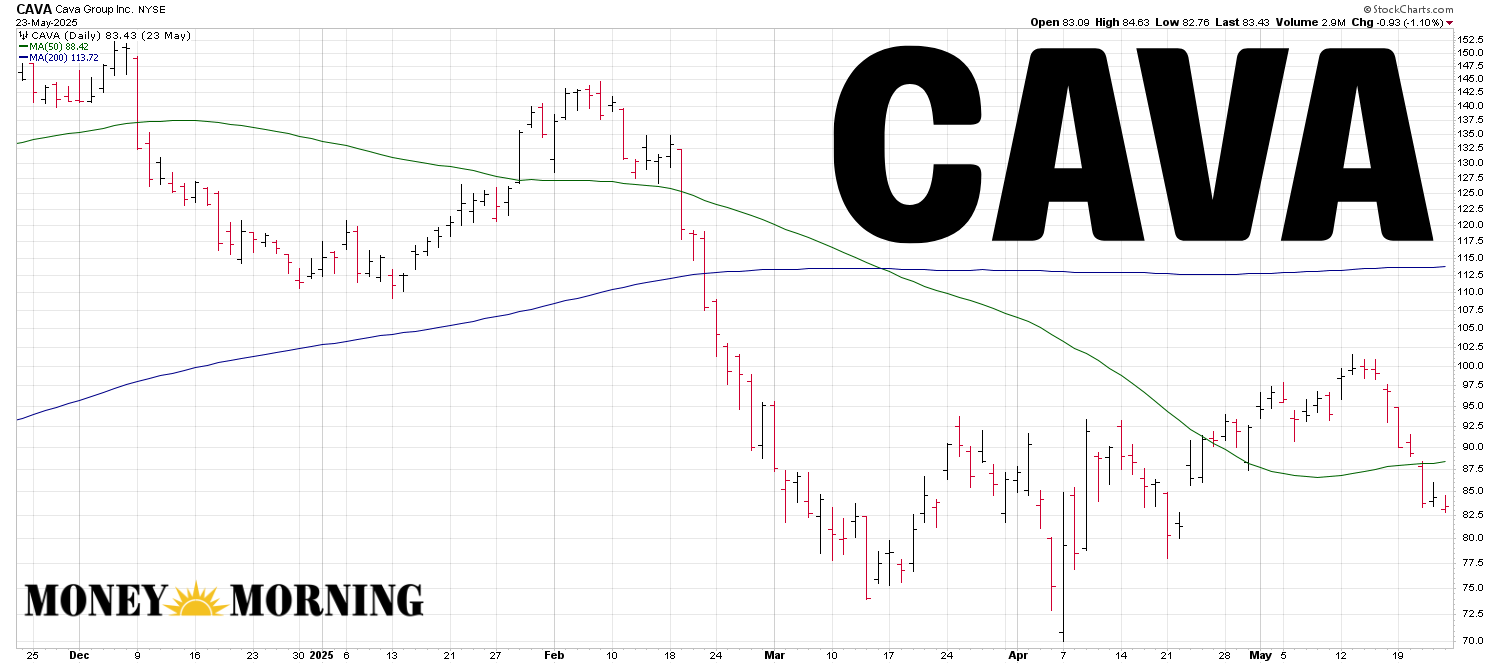

CAVA Group (NYSE:CAVA) is a fast-casual Mediterranean restaurant chain. It had a very strong post-IPO run and traded very expensively before tumbling as market sentiment shifted. Same-store sales and revenue growth have remained great, but have begun to decelerate compared to previous quarters. A high proportion of sales growth is now driven by price increases rather than increased customer traffic, which some investors view as a less sustainable long-term driver.

CAVA Group (NYSE:CAVA) is a fast-casual Mediterranean restaurant chain. It had a very strong post-IPO run and traded very expensively before tumbling as market sentiment shifted. Same-store sales and revenue growth have remained great, but have begun to decelerate compared to previous quarters. A high proportion of sales growth is now driven by price increases rather than increased customer traffic, which some investors view as a less sustainable long-term driver.

Regardless, the company has lots of pricing power, and CAVA stock sits at a 44.7% discount. It trades at 69.5 times earnings vs. the 222.5 premium investors have paid on average. Future growth is expected to be strong, and the bottom line has had stellar growth in recent years. The 3-year EBITDA growth rate is at 101.7%, and analysts see 22.5% annual revenue growth this decade.

The consensus price target of $118.2 implies 41.7% upside, but price targets go up to $175. Net income only turned positive in Q4 2023, so I see plenty of runway until the company runs out of pricing power. There’s also a good chance that the company will go international.

Cogent Communications (CCOI)

Cogent Communications (NASDAQ:CCOI) is an internet service provider company and also has colocation in data centers. The stock declined recently due to its underwhelming Q4 2024 earnings. It reported service revenue of $252.3 million, down 7.3% year-over-year. It has also seen declining customer connections as total customer connections fell by 10.3% year-over-year.

Cogent Communications (NASDAQ:CCOI) is an internet service provider company and also has colocation in data centers. The stock declined recently due to its underwhelming Q4 2024 earnings. It reported service revenue of $252.3 million, down 7.3% year-over-year. It has also seen declining customer connections as total customer connections fell by 10.3% year-over-year.

Q1 financials weren’t that great either. Cogent’s EPS came in at -$1.09, which is 4 cents worse than analyst expectations. The debt burden is also significant.

However, it’s not as bad as you may think. The declining customer connections are due to the company acquiring Sprint’s wireless business in 2023, which is when it inherited lots of legacy contracts. Many of these are unprofitable connections, and a phase-out is not bad for Cogent.

Profitability is also improving as non-GAAP gross margin increased to 44.6% in Q1 2025, up from 38.7% in Q4 2024. Net cash provided by operating activities increased to $36.4 million in Q1 2025, up from $14.5 million in Q4 2024. The company is well-positioned to capture demand from data centers and high-capacity networks due to how expansive its fiber network is. It has also seen growth in revenue from leasing IPv4 addresses, with a 42% increase from Q1 2024 to Q1 2025.

The consensus price target of $67.5 implies 44% upside, but price targets go up to $93.

— Omor IE

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning