After negotiations in Geneva between U.S. and Chinese officials, both countries will be partially pausing tariffs for 90 days starting May 14th. The U.S. will drop its tariffs to 30% (due to the 20% “fentanyl tariffs”), and China will drop its tariffs to 10%.

The market has rallied as expected, and many tariff-prone stocks that would’ve otherwise been crushed in a long-term trade war have seen their stocks soar. President Donald Trump has also said that tariffs on China will never go back to the level of 145% even if these tariffs expire without both sides reaching an agreement.

If you think that this pause will lead to a permanent resolution of the trade war, it’s worth buying up some stocks that could be major beneficiaries. Here are three to look into:

ACM Research (ACMR)

ACM Research (NASDAQ:ACMR) is a U.S.-based company, but it sells its products extensively in China. The stock surged nearly 11% when the tariff pause was announced, and it could deliver more gains in the coming weeks, especially if this pause leads to a comprehensive deal.

ACM Research (NASDAQ:ACMR) is a U.S.-based company, but it sells its products extensively in China. The stock surged nearly 11% when the tariff pause was announced, and it could deliver more gains in the coming weeks, especially if this pause leads to a comprehensive deal.

This company manufactures semiconductor manufacturing equipment that is focused on wafer processing. It makes wafer cleaning and packaging equipment essential for manufacturing AI chips, and the AI sector in China has been seeing accelerated demand ever since DeepSeek caused a surge in investments and gave companies in China confidence that they could compete.

ACMR stock is still down 18% from the March peak this year, but I believe it is sitting at very undervalued levels. A short-seller named Kerrisdale posted a bullish report on ACMR Research a few months ago. It called ACM Research as one of China’s national champions in the semiconductor wafer fabrication equipment (WFE) industry and pointed out that the company’s Shanghai Arm (ACM Research Shanghai Inc) is worth much more.

Currently, ACM Shanghai is worth $6.39 billion vs. $1.57 billion for ACM Research, which owns 81.1% equity in ACM Shanghai. That alone should be enough reason for looking deeper here.

The consensus price target at $35.8 implies 45.5% upside potential.

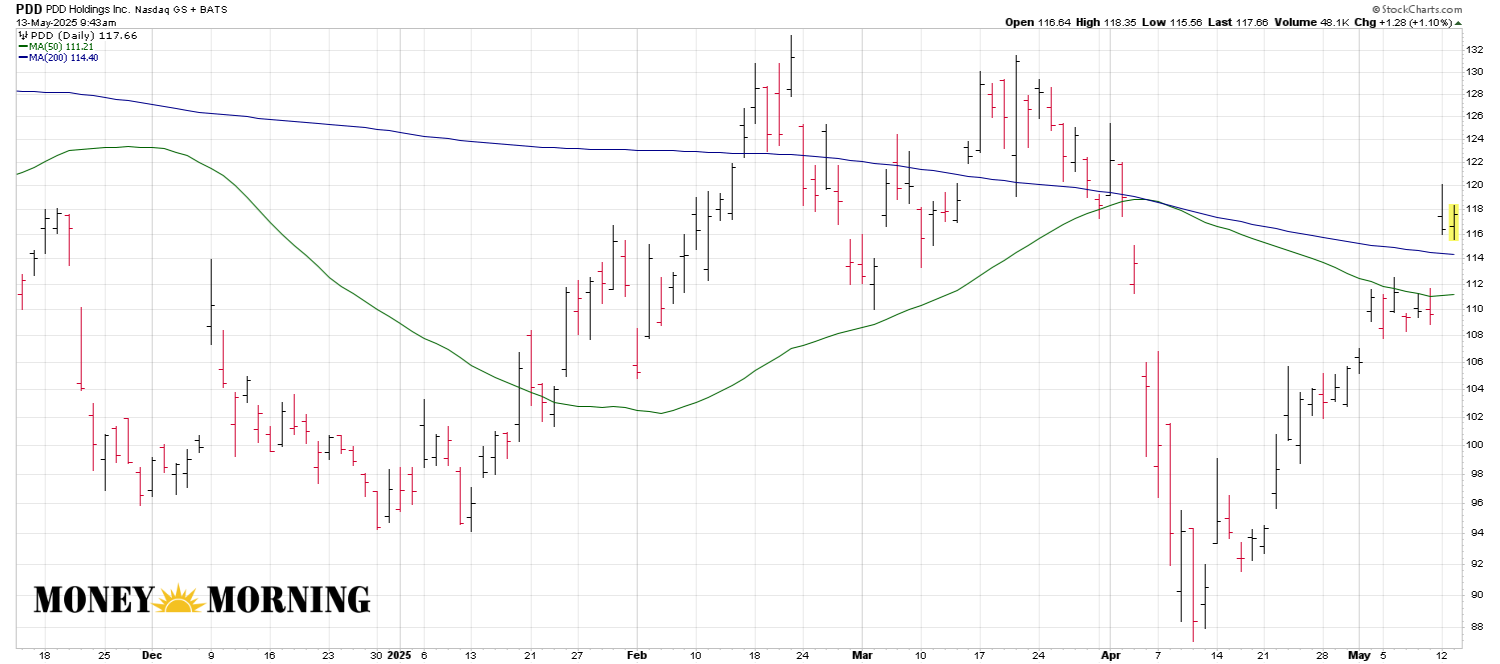

PDD Holdings (PDD)

PDD Holdings (NASDAQ:PDD) owns Pinduoduo in China and also owns Temu. It still has a lot to lose from the trade war, since the de minimis suspension will remain in effect. But even then, the company will have to pay much less on its exports. Even if items on Temu cost 30% more, it won’t completely collapse the business.

PDD Holdings (NASDAQ:PDD) owns Pinduoduo in China and also owns Temu. It still has a lot to lose from the trade war, since the de minimis suspension will remain in effect. But even then, the company will have to pay much less on its exports. Even if items on Temu cost 30% more, it won’t completely collapse the business.

You should also keep in mind that a lot of bearishness has already been priced in here. The stock trades at just 11 times earnings. This is also a company that isn’t nearly as reliant on the U.S. as many people think. U.S.-derived revenue from Temu is a small portion of PDD Holdings, and the current discount Wall Street has on this stock due to tariff concerns is a bit excessive.

The company has $45.5 billion in cash vs. just $1.46 billion of debt. The 3-year revenue growth rate is at 52.4% annually, and the 3-year EBITDA growth is at 109% annually. Both are better than 95% and 97.5% of its industry peers. Net margin is also at 28.5%. Future 3-5Y revenue growth is also expected to be around 17% to 18% annually.

Paying just 11 times earnings for a high-growth, high-margin business with almost no debt is definitely a bargain.

The consensus price target at $144.24 implies 24% upside.

Boeing Co (BA)

Boeing (NYSE:BA) has had lots in the past year, and the trade war with China may not look like big news if you compare it to the drama that took place after a door fell out.

Boeing (NYSE:BA) has had lots in the past year, and the trade war with China may not look like big news if you compare it to the drama that took place after a door fell out.

But the resumption of deliveries to China could lead to a boost for Boeing, as China is a massive aerospace market. Previously, Boeing confirmed that Chinese customers had stopped accepting new planes due to the tariff environment, with some jets even being returned to the U.S. after Chinese companies refused delivery. China has since lifted the Boeing delivery ban.

Boeing’s executives had expected to deliver approximately 50 jets to Chinese airlines this year, with 41 already in production or assembled. Chinese clients are expected to accept 25 out of the 30 remaining 737 MAX jets produced before 2023. The tariff pause might spare Boeing the considerable time and cost of finding alternative buyers for these aircraft. China accounts for a tenth of Boeing’s commercial backlog and is forecast to constitute a fifth of the global aircraft demand over the next two decades.

Even without China, BA stock is not a bad bet as interest rates eventually come down and relieve Boeing of the multi-billion debt servicing.

— Omor Ibne Ehsan

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning