Super Micro Computer (NASDAQ:SMCI) has been one of the worst-performing AI stocks if you bought it near its peak back in early 2024. It got caught up in significant drama, and while it has started making a recovery from its trough recently, many still see it as a risky bet. I’m personally bullish here, but I also think many of the company’s competitors are great picks and can deliver triple-digit returns over the coming years.

The data center and cloud computing industry is big enough to accommodate all these growth stories. The AI server market remains red-hot, and research from Gartner projects data center spending to jump 15.5% to $367 billion in 2025. The companies in this sector are trading at bargain valuations compared to most other AI bets. Here are three to look into:

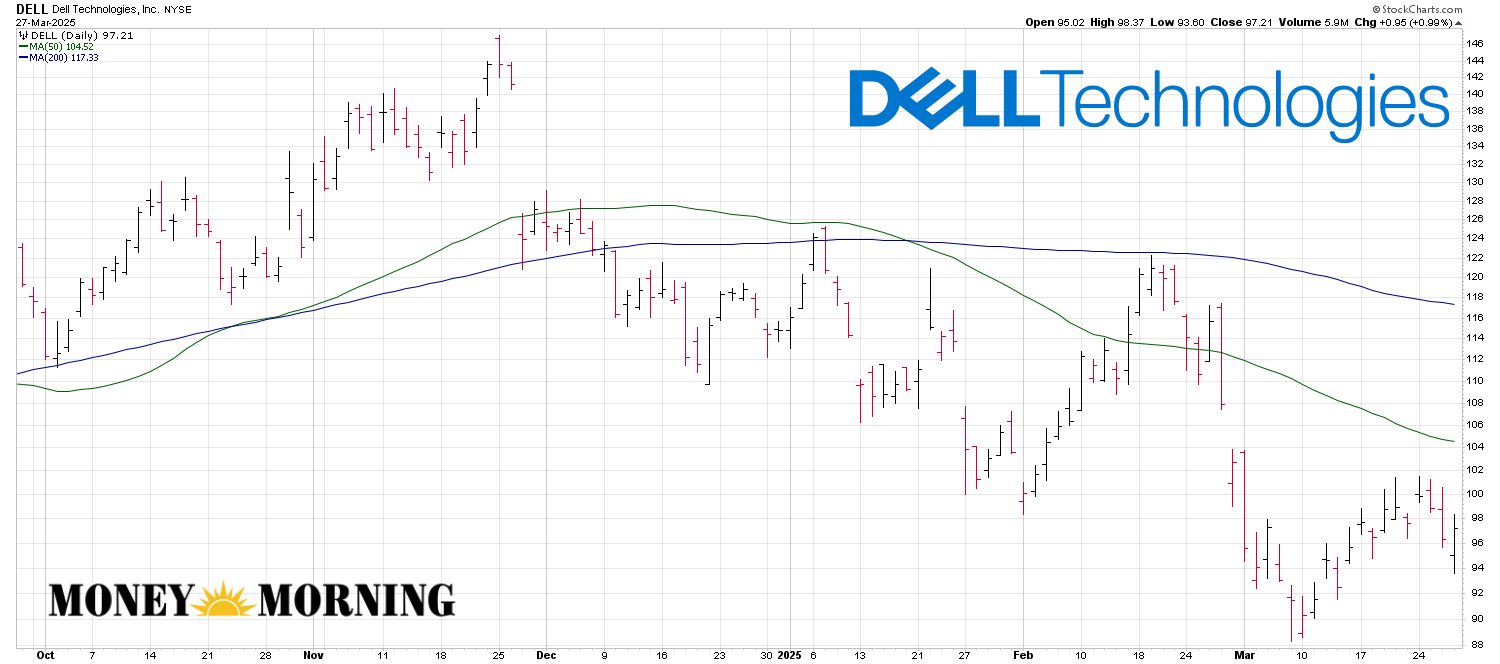

Dell (DELL)

This is the obvious pick and is likely the first competitor that pops into mind. If you’re choosing between Dell (NYSE:DELL) and Super Micro, and you’re confident that the industry is going to do great over the coming years, it’s a better idea to buy both.

Dell stock boasts solid metrics and trades at a surprisingly cheap valuation. Right now, the stock is at a discount. If the AI narrative takes off and data center growth continues its upward trajectory, DELL could easily deliver multibagger gains from here. It is down over 39.5% from its May 2024 peak and is trading at just 15 times earnings right now. DELL stock also comes with a 2.17% dividend yield.

Dell stock boasts solid metrics and trades at a surprisingly cheap valuation. Right now, the stock is at a discount. If the AI narrative takes off and data center growth continues its upward trajectory, DELL could easily deliver multibagger gains from here. It is down over 39.5% from its May 2024 peak and is trading at just 15 times earnings right now. DELL stock also comes with a 2.17% dividend yield.

Dell suffers from a legacy brand image tied to laptops and PCs. Many investors haven’t caught on to its transformation. These days, the company is far more cutting-edge and leans heavily into the AI data center industry. Dell is positioned to ride the wave and deliver outsized returns if data center spending keeps climbing.

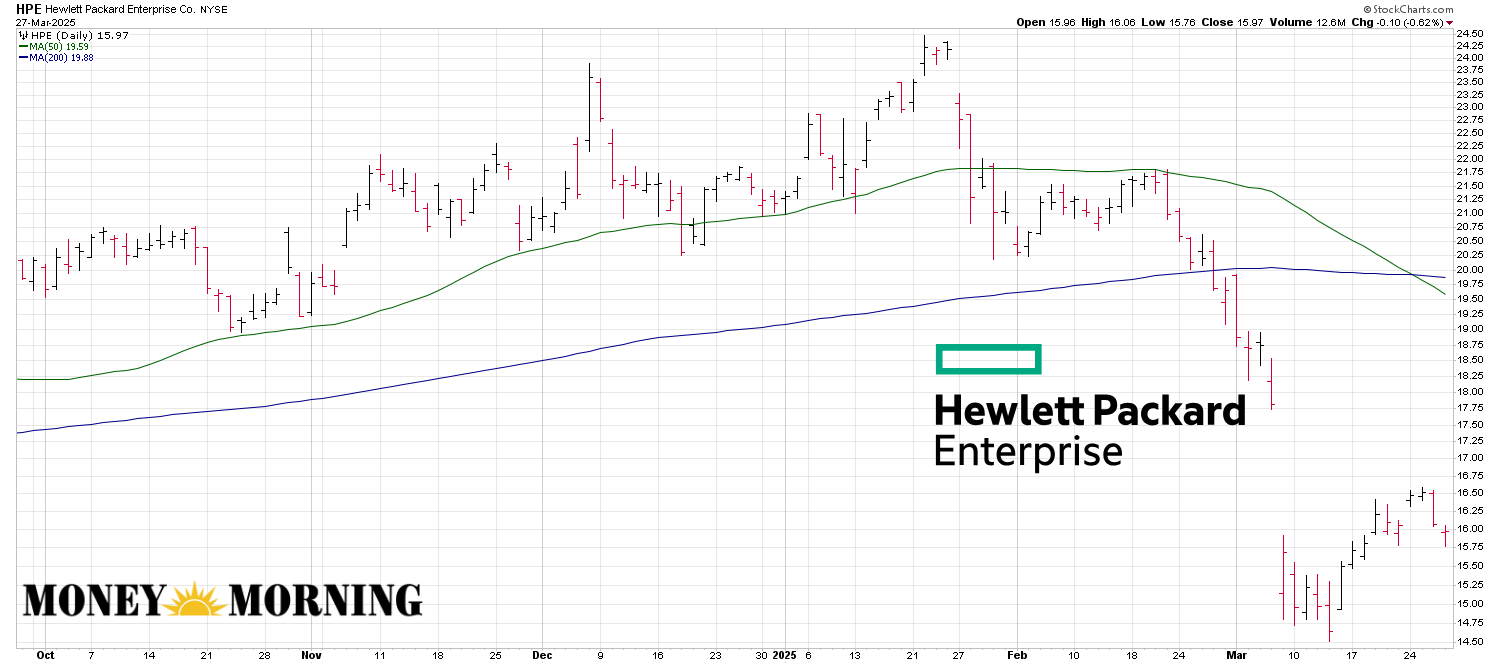

Hewlett Packard Enterprise (HPE)

Hewlett Packard Enterprise (NYSE:HPE) is a data center and enterprise tech company. Recently, HPE’s stock has taken a hit and is down 32.5% from its January 2025 peak. The company reported solid Q1 2025 revenue of $7.85 billion, up 16% year-over-year, but its guidance for the full year disappointed investors as it only projected 7-11% growth.

Margins also slipped, with non-GAAP gross margin dropping to 29.4%. HPE projects adjusted EPS of $1.70-$1.90, whereas analysts had expected $2.13. Hewlett-Packard announced that it was cutting 2,500 jobs on top of that.

Margins also slipped, with non-GAAP gross margin dropping to 29.4%. HPE projects adjusted EPS of $1.70-$1.90, whereas analysts had expected $2.13. Hewlett-Packard announced that it was cutting 2,500 jobs on top of that.

Regardless, I see HPE as a solid long-term buying opportunity because it trades at a dirt-cheap valuation. It trades at less than 8 times earnings right now and also pays a 3.25% dividend. The stock could easily deliver multibagger gains in the long run as the data center industry grows.

This is a well-established data center company with serious upside potential. Any dips are worth scooping up since these stocks tend to perform well over time and recover strongly. It’s hard to imagine HPE falling much lower than its current price.

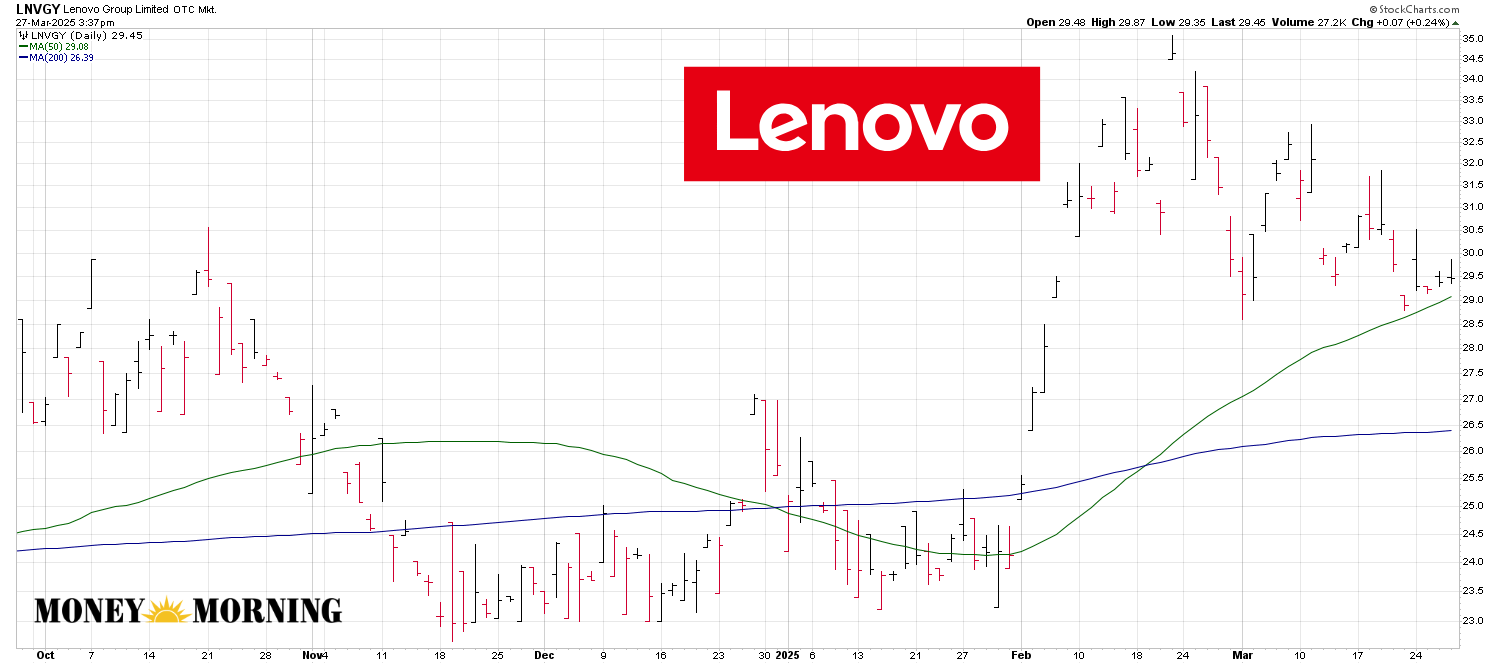

Lenovo Group (LNVGY)

Lenovo Group (OTCMKTS:LNVGY) makes a wide range of electronics and has been aggressively pushing into AI-driven technologies and data center operations.

The stock has steadily climbed over the past two years and has nearly doubled from its trough back in 2022. Recent quarters have been a home run. For Q3 of fiscal year 2024/25, Lenovo reported a 20% year-on-year revenue jump to $18.8 billion, with net income doubling to $693 million. The Infrastructure Solutions Group, which handles data centers, turned profitable again, driven by demand for AI servers.

The stock has steadily climbed over the past two years and has nearly doubled from its trough back in 2022. Recent quarters have been a home run. For Q3 of fiscal year 2024/25, Lenovo reported a 20% year-on-year revenue jump to $18.8 billion, with net income doubling to $693 million. The Infrastructure Solutions Group, which handles data centers, turned profitable again, driven by demand for AI servers.

Unlike many Chinese firms, Lenovo sidesteps global scrutiny with a stellar reputation across markets. It’s headquartered in Hong Kong but operates in 180 countries, and it’s seen as a reliable, innovative leader. Profitability is rock-solid, with a 3.08% dividend yield that pays out semiannually. It is pouring cash into AI, and R&D spending was up 14% to $621 million in the last quarter alone.

Analysts see 42% EPS growth and 18.14% revenue growth for FY2025. You’re paying less than 13 times forward earnings for this stock. Moreover, the company has operations beyond just data centers and has a strong electronics segment. Even if AI hype cools, this non-AI business can keep it growing. LNVGY also comes with a 3.35% dividend yield.

— Omor Ibne Ehsan

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning