Gold has rallied almost 37% over the past year due to uncertainty plaguing the economy. The rally has accelerated in recent weeks as gold is being seen as a perfect hedge against both inflation and a recession. Recent comments from the Federal Reserve’s meeting and today from Chicago Fed’s Goolsbee indicate that the Fed is just as uncertain as the rest of us and is waiting for further data before they decide on cuts.

As such, gold could surge even further since no one knows how much retaliatory tariffs will cause a spike in inflation if it materializes in the first place. Gold stocks will be the biggest beneficiary of this since their financials have the best exposure to gold. Historically, gold miners lag gold price surges initially but catch up as financials improve, and the stocks below should fit the pattern.

i-80 Gold Corp. (IAUX)

i-80 Gold Corp (NYSEAMERICAN:IAUX) is a Nevada-focused mining company that is developing a portfolio of advanced-stage gold and polymetallic projects.

Q3 2024 revenue took a hit and dropped sharply year-over-year due to lower production and sales volume. It reported losses and missed analyst expectations. Cash burn is high as i-80 invests heavily in its projects, and its debt load is at $177 million, though it has gone down for two quarters straight.

Q3 2024 revenue took a hit and dropped sharply year-over-year due to lower production and sales volume. It reported losses and missed analyst expectations. Cash burn is high as i-80 invests heavily in its projects, and its debt load is at $177 million, though it has gone down for two quarters straight.

On the flip side, management has launched a two-phase recapitalization plan to generate free cash flow and restructure debt.

The current market cap of $281 million leaves significant room for upside as gold rallies. The Mineral Point Project alone has an NPV of $614 million at $2,175/oz, with 3.4 million ounces of indicated gold resources. At gold prices of $2,900 per ounce, the NPV increases significantly to $2.1 billion. Today, gold is even higher. Add in Granite Creek, McCoy-Cove, and Ruby Hill, and the resource upside is huge.

The consensus price target of $3.5 implies 411% upside.

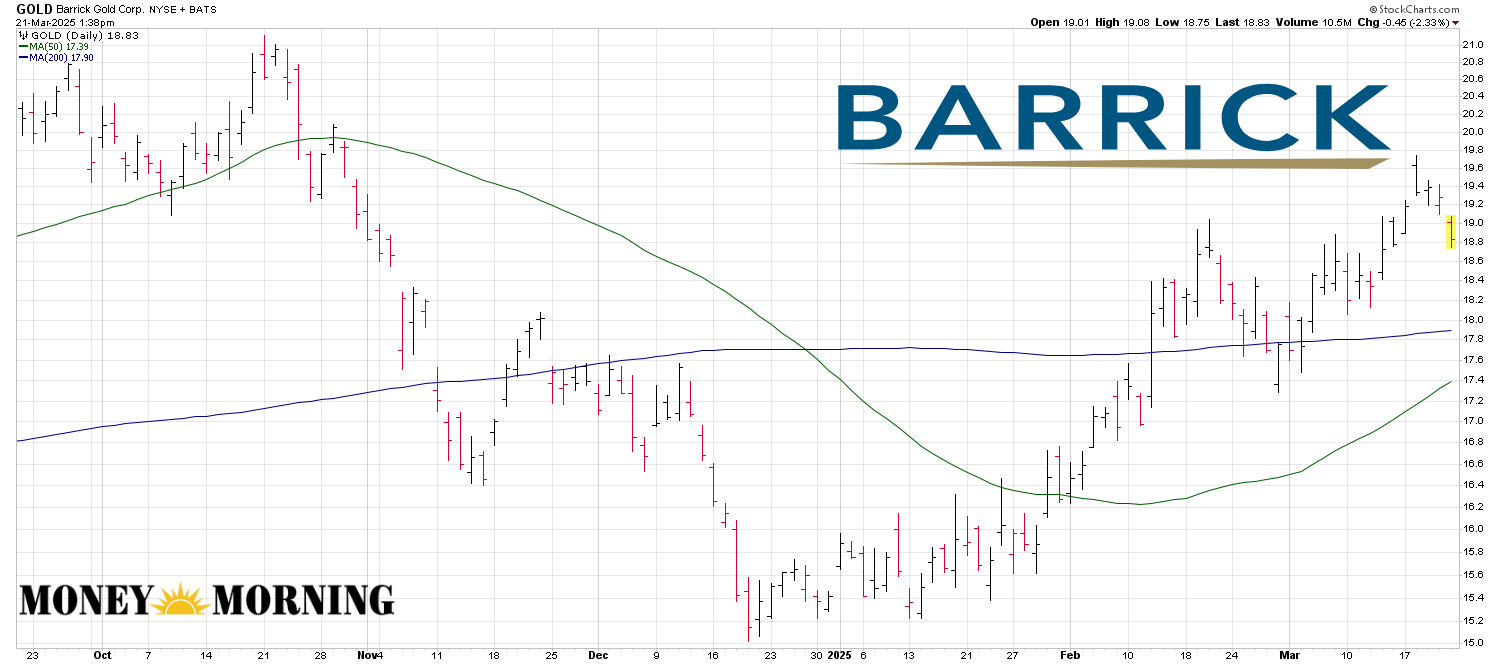

Barrick Gold (GOLD)

Barrick Gold (NYSE:GOLD) is up only 18.6% over the past year but could surge significantly due to the latest rally in gold. It is one of the largest gold producers, and it also has a strong foothold in copper.

In 2024, Barrick produced nearly 3.9 million attributable ounces of gold and about 430 million pounds of copper. For the full year 2024, Barrick reported net earnings of $2.14 billion, up 69% year-over-year. Operating cash flow grew 20% to $4.5 billion, and free cash flow more than doubled to $1.3 billion. Adjusted net profit after tax hit about $800 million, or $0.45 per share, up 70% from the same quarter in 2023. Barrick also launched a $1 billion share buyback program in February 2025.

In 2024, Barrick produced nearly 3.9 million attributable ounces of gold and about 430 million pounds of copper. For the full year 2024, Barrick reported net earnings of $2.14 billion, up 69% year-over-year. Operating cash flow grew 20% to $4.5 billion, and free cash flow more than doubled to $1.3 billion. Adjusted net profit after tax hit about $800 million, or $0.45 per share, up 70% from the same quarter in 2023. Barrick also launched a $1 billion share buyback program in February 2025.

Early 2025 updates suggest this strength is carrying forward. Barrick’s March 14, 2025, annual report press release shows solid progress in its projects and is expected to drive a 30% increase in gold equivalent ounces by 2030. Management expects initial benefits to materialize this year.

EPS growth is expected to be around 18% this year and next year. It’s a cash cow that will rape in the dough if gold keeps climbing.

The consensus price target of $23.75 implies 26% upside, but it has a price target of $38, which implies over 118% upside potential.

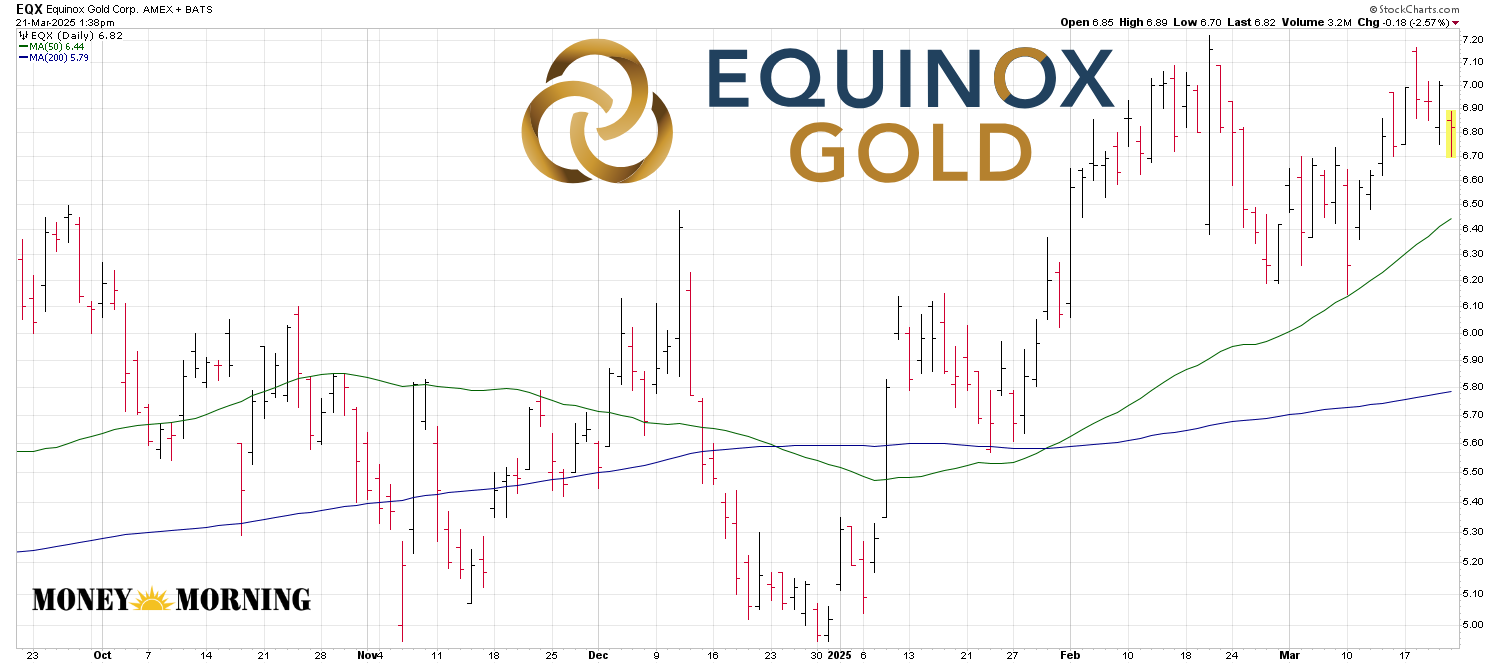

Equinox Gold (EQX)

Equinox Gold (NYSEAMERICAN:EQX) surged significantly in late 2024 and boomed early during COVID before a selloff. The stock has been stable since late 2022 and has more than doubled from its trough.

Equinox ended 2024 with approximately $240 million in cash and equivalents, $105 million available on its revolving credit facility, and an additional $100 million undrawn accordion feature.

Equinox ended 2024 with approximately $240 million in cash and equivalents, $105 million available on its revolving credit facility, and an additional $100 million undrawn accordion feature.

It also significantly reduced debt. It paid down $180 million in Q4 2024 alone. This included settling a $40 million obligation to Orion Mine Finance for the Greenstone stake and converting $140 million in convertible notes to equity. The company expects to reduce more debt this year. It targets a debt-to-EBITDA ratio of 1x by 2026.

The market doesn’t seem to fully price in the potential of the Calibre merger. If approved, the combined entity would boast massive reserves, enhanced liquidity (trading on the NYSE), and a stronger balance sheet as cash flows from both companies synergize.

That said, the merger with Calibre isn’t finalized. Debt is still over $1.4 billion, and a sharp drop in gold prices (unlikely but possible) could strain finances. Still, the consensus leans positive. The consensus price target of $35 implies 413% upside.

— Omor Ibne Ehsan

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning