The Nasdaq Index has been on the edge of correction territory as most tech stocks have pulled back considerably due to tariff fears being compounding on previous doubts about the AI rally. Magnificent Seven stocks have spearheaded the stock market’s gains, but as trends point to a possible long-term reversal, many think they could also lead the way back down.

With that in mind, should you buy or sell the Magnificent Seven stocks? It’s not a good idea to tag all seven stocks with the same rating, so let’s take a look at each one.

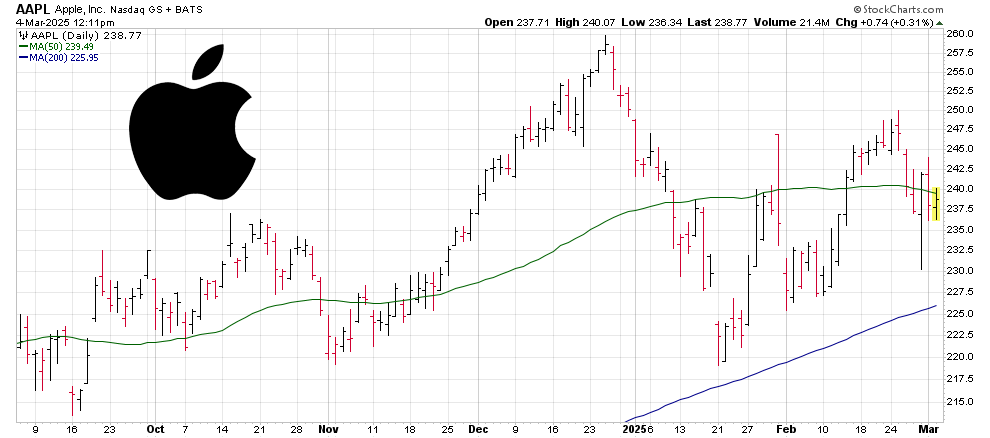

Apple (AAPL)

Apple’s (NASDAQ:AAPL) financials have been quite sluggish as China sales have plunged, and there has been a general slowdown in most of its metrics. Its products have also failed to excite customers, though its recent lineup of “Air” products could recover growth down the line.

Apple’s (NASDAQ:AAPL) financials have been quite sluggish as China sales have plunged, and there has been a general slowdown in most of its metrics. Its products have also failed to excite customers, though its recent lineup of “Air” products could recover growth down the line.

The latter is why the stock hasn’t made a big move to the downside and is up 36.7% in the past year. Its AI rollout has been quite lukewarm, but Apple’s coming out with more affordable products and spending $500 billion in U.S. manufacturing. This should boost growth, but it’s debatable how much.

Analysts expect 8.7% EPS growth this year, along with 4.6% revenue growth. Paying 32 times forward earnings for this growth leaves significant downside risk, and the stock has historically traded at cheaper levels on average.

The consensus price target of $243.9 implies just 2% upside potential from here, so a “Hold” rating fits AAPL stock best.

Amazon (AMZN)

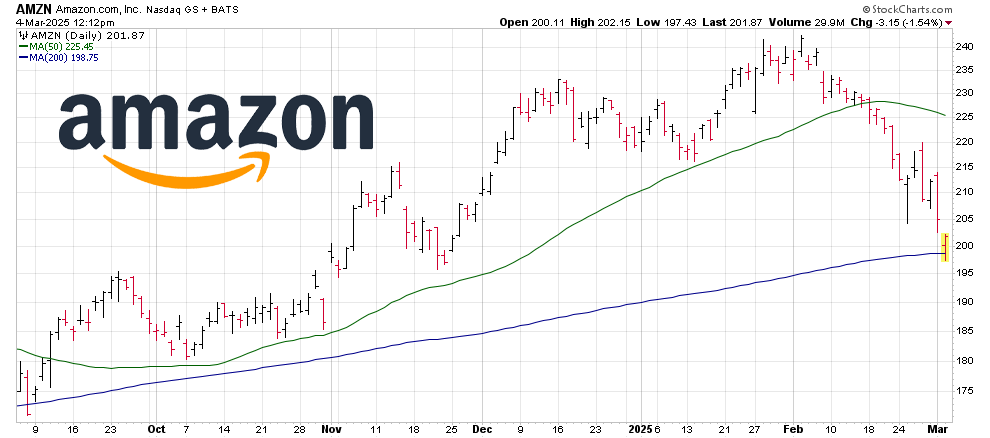

Amazon (NASDAQ:AMZN) is much more involved in AI and data centers due to AWS and its investments in AI startups like Anthropic. This is mainly why the stock has taken a bigger hit from the recent AI selloff.

Amazon (NASDAQ:AMZN) is much more involved in AI and data centers due to AWS and its investments in AI startups like Anthropic. This is mainly why the stock has taken a bigger hit from the recent AI selloff.

The stock is down 17.7% in the past month and has declined below $200. The stock looks pretty attractive at these levels as its cloud business is still hot, and the business has solid growth rates. EPS is expected to grow 14.3% this year, and revenue growth is expected to be 9.6%.

You’re paying 32 times forward earnings, but investors have historically paid a big premium for AMZN stock. The recent decline also leaves less downside risk, and the consensus price target of $260.65 implies 31.13% upside. It might be a good idea to start buying the dip, though a prolonged AI selloff can obviously drag it down more.

Alphabet (GOOG, GOOGL)

Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) has tumbled 18.4% in the past month. This is mainly due to fears that AI chatbots will have a negative impact on Google’s search volume.

Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) has tumbled 18.4% in the past month. This is mainly due to fears that AI chatbots will have a negative impact on Google’s search volume.

However, it seems like an overreaction since Google itself is making some solid progress with its own AI models. It also trades at just 19 times forward earnings, which is pretty cheap compared to most other AI stocks.

Alphabet owns the world’s two most popular websites by traffic volume, and analysts expect its EPS to grow by 11.8% this year, along with an 11.4% revenue growth. I believe GOOG stock is a solid long-term buy as the AI hype rally didn’t drive it up to dangerously overvalued levels, and any pullback is unlikely to be as extreme.

The consensus price target of $209.13 implies 23.21% upside.

Meta Platforms (META)

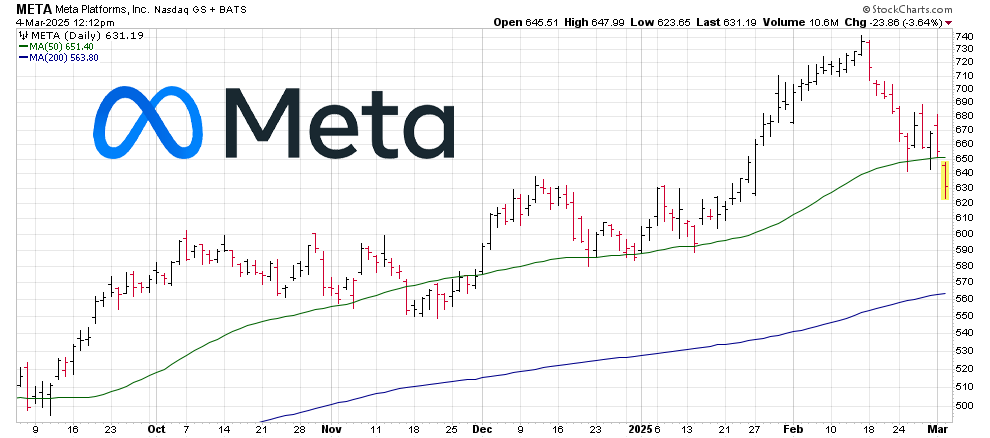

Meta Platforms (NASDAQ:META) has been a multibagger stock from its trough in 2022 and is still up over 532%. The advertising growth, along with its aggressive investments in AI, has made it a growth stock again.

Meta Platforms (NASDAQ:META) has been a multibagger stock from its trough in 2022 and is still up over 532%. The advertising growth, along with its aggressive investments in AI, has made it a growth stock again.

A broader market rally will naturally drive up META stock, but as market sentiment sours, taking some profits here is not a bad idea. Meta’s debt load has grown from $14 billion in Q1 2022 to $49 billion in Q4 2024.

A lot of that is going into AI.

The core “Family of Apps” business is a mature cash cow, so Meta is unlikely to stay a growth stock unless its AI gamble pays off big.

The consensus price target of $719.3 implies 14.9% upside.

Microsoft (MSFT)

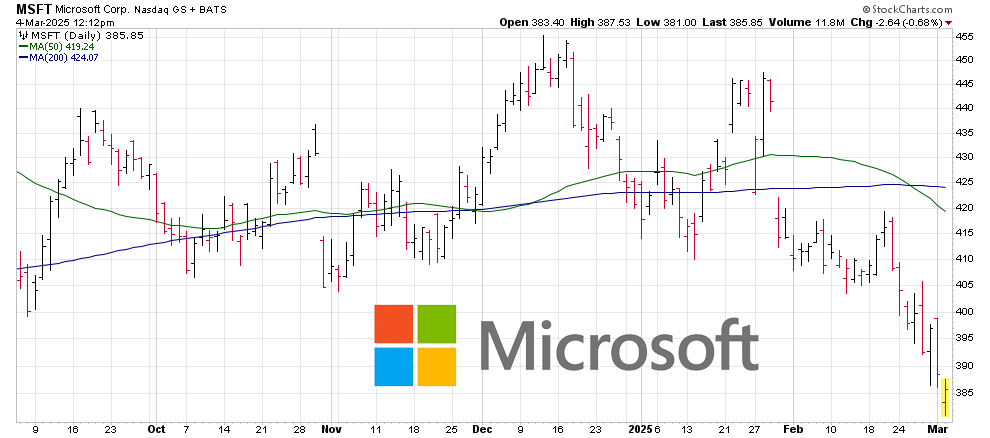

Microsoft (NASDAQ:MSFT) is partially responsible for the recent bout of panic in the stock market. It canceled some of its data center leases, which contradicted its earlier doubling-down on AI.

Microsoft (NASDAQ:MSFT) is partially responsible for the recent bout of panic in the stock market. It canceled some of its data center leases, which contradicted its earlier doubling-down on AI.

I see MSFT as an evergreen investment since white-collar businesses can’t function without Windows and Microsoft Office products. It is also heavily involved in AI, and Azure is not that far behind AWS.

The recent correction has already priced in much of the bearishness. Unless the broader market sees a severe tech selloff, I don’t see much downside risk.

The consensus price target of $511 implies 32.5% upside.

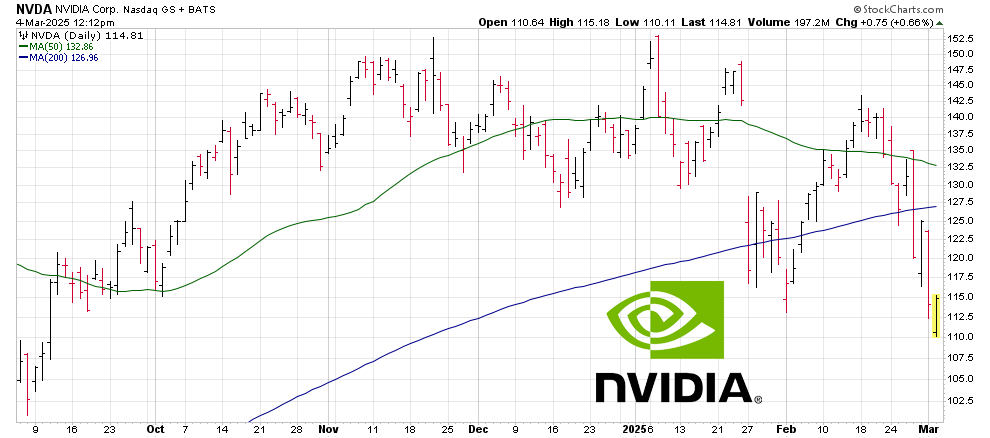

Nvidia (NVDA)

Nvidia’s (NASDAQ:NVDA) fate hinges entirely on the AI narrative. The stock is down 12.7% in the past month. This could be the start of a cyclical downturn in the broader semiconductor market like in 2022.

Nvidia’s (NASDAQ:NVDA) fate hinges entirely on the AI narrative. The stock is down 12.7% in the past month. This could be the start of a cyclical downturn in the broader semiconductor market like in 2022.

The growth rates have been solid so far but Nvidia hasn’t beat estimates too significantly, and tariffs and chip restrictions could shave off billions off of its sales if they materialize.

if you think companies will keep pouring money into AI, the dip could be worth buying. But given the risk of a long-term cool-off in AI stocks, it’s better to hold off on buying the dip.

The consensus price target of $169.6 implies 49.8% upside.

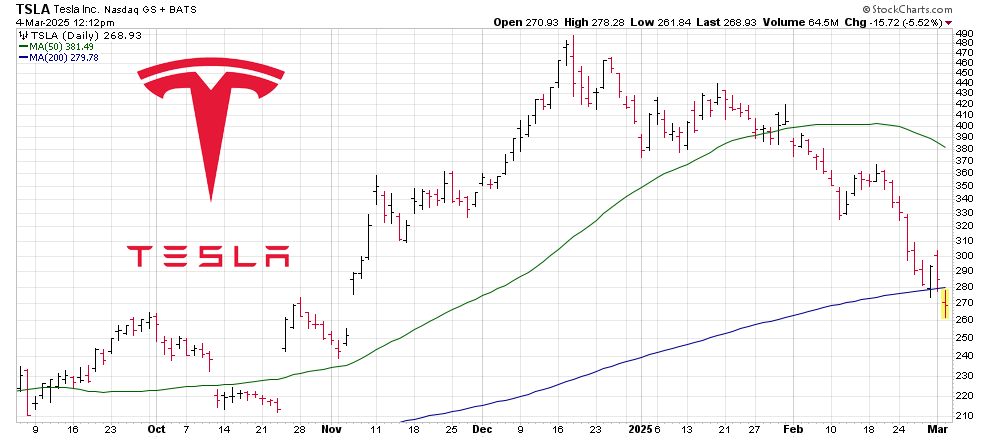

Tesla (TSLA)

Tesla (NASDAQ:TSLA) was the biggest winner in the months after Trump’s election, but the stock has plunged since then as fundamentals are not that great here.

Tesla (NASDAQ:TSLA) was the biggest winner in the months after Trump’s election, but the stock has plunged since then as fundamentals are not that great here.

Bulls think Tesla’s full-self-driving and planned robotaxi launch could drive it up, eventually becoming a robotics play due to Optimus robots. However, I think the market is too optimistic about both of these catalysts. Optimus robots are remotely controlled at showcase events, and they are likely over a decade away from being truly autonomous.

As for FSD, it’s debatable how much value that would add to Tesla once it is launched. Q4 2024 automotive revenue fell 8% year-over-year, with European sales down 38-63% in January 2025. On top of that, Musk’s involvement in politics is shaving off a good portion of Tesla’s customer base, and his attention seems to be on DOGE instead.

Protectionism already gives Tesla free rein in the U.S., and the profit hit on Tesla does not seem to be worth any market share gains once EV subsidies are pulled back.

I wouldn’t buy the dip here as it still trades at 100x forward earnings with worsening top and bottom-line metrics.

— Omor Ibne Ehsan

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning