There have been two consecutive years of 20%+ returns in the S&P 500, but you should keep in mind that a third year of outsized gains is quite rare. based on market data since 1928, there’s little chance of that happening. In fact, many would agree that this extended bull run has created a dangerous environment, especially for stocks that don’t have the fundamentals to survive a correction.

Tech stocks have rallied back to 2021 levels but appear to be turning a corner for the worse. Even bullish investors acknowledge a correction is coming. They’re only bullish now as they think a correction is further off.

The bulls may be right, but it’s a good idea to look into some precarious names just in case the broader market doesn’t cooperate. Some companies have a narrow path to success, and if broader market conditions worsen, their weak fundamentals could send them toward zero. Here are three such stocks to sell:

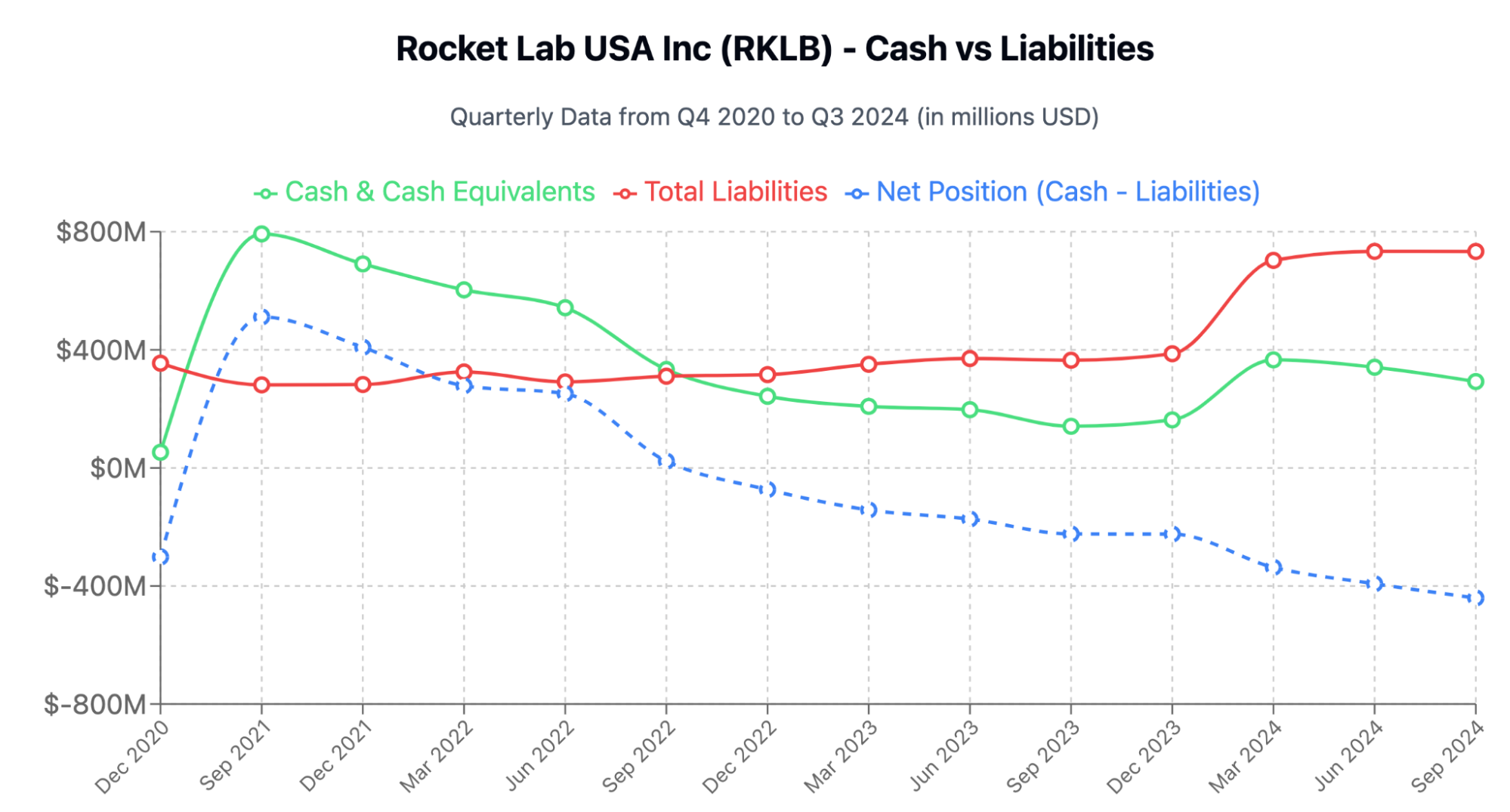

Rocket Lab (RKLB)

Things have been great for Rocket Lab (NASDAQ:RKLB) as the stock is up over 363% in the past year. It has already corrected by 33% from its peak and bounced off $20, so investors are optimistic it will rally back up again. I don’t think such a rally would last long.

Things have been great for Rocket Lab (NASDAQ:RKLB) as the stock is up over 363% in the past year. It has already corrected by 33% from its peak and bounced off $20, so investors are optimistic it will rally back up again. I don’t think such a rally would last long.

It is a good idea to look into the fundamentals here. If I was asked to name some space companies that went public and managed to turn into a profitable success story, I’d struggle to name even one. Virtually every space stock has disappointed its shareholders in the long run due to how capital-intensive the industry is.

Rocket Lab is expected to be an outlier due to the 55% year-over-year revenue growth in Q3 and a backlog of $1.05 billion. It is also the closest public space stock to SpaceX and its upcoming Neutron rocket could compete with SpaceX’s Falcon 9. It is expected to debut in 2025 and start commercial launches in 2026.

Neutron launches are expected to sell for an average price of $50-55 million per launch, with projected gross margins of 40-50%, and could turn it into a profitable company. With its $10.4 billion market cap, that’s already priced in.

However, I think it’s unlikely that it will meet timelines, and even if it does, it’ll struggle to compete with SpaceX. SpaceX’s Falcon 9 currently charges around $70 million and SpaceX’s launch volume will allow it to lower prices more if it has to compete. Moreover, I do not think it will land government contracts like SpaceX does, especially since Musk now has influence over the government. Rocket Lab is already taking on more debt due to the cash burn.

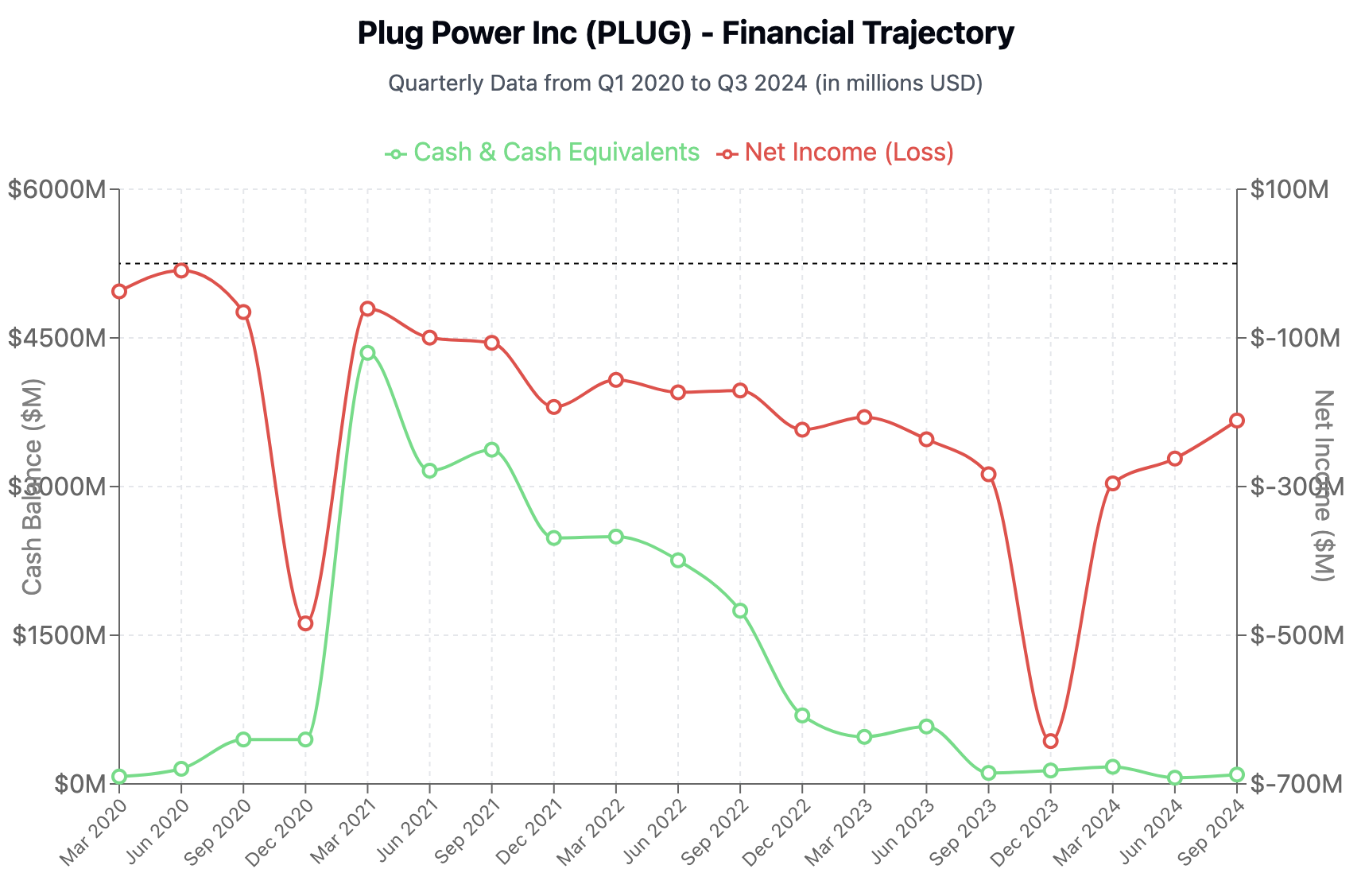

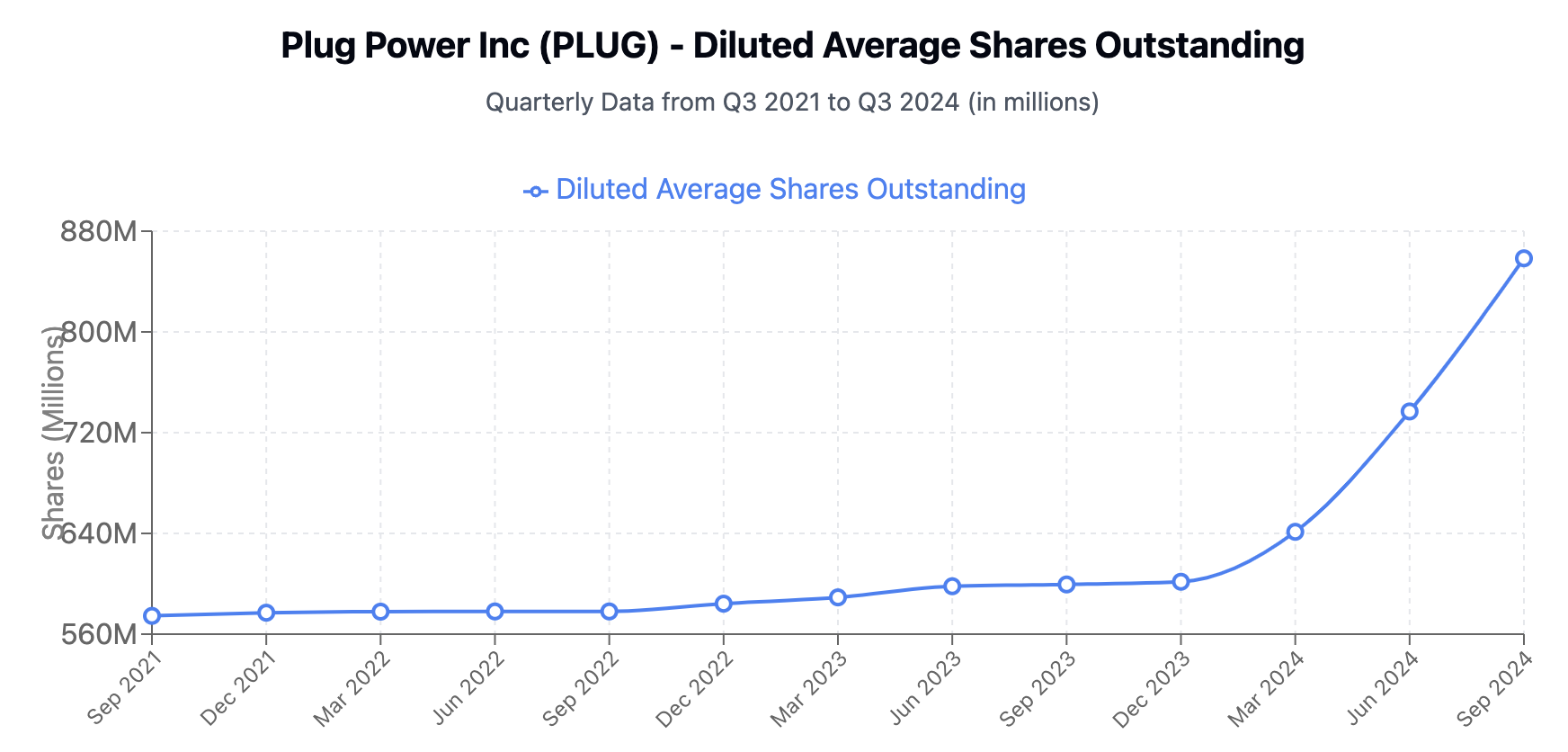

Plug Power (PLUG)

Plug Power (PLUG)

Plug Power (NASDAQ:PLUG) hasn’t been that lucky and the stock has been continuously declining since its initial run in 2021. The company makes hydrogen fuel cell systems, and considering the narrative has failed to bring it fruit during the Biden Era, things are probably going to be even tougher in the next four years for this stock.

Plug Power (NASDAQ:PLUG) hasn’t been that lucky and the stock has been continuously declining since its initial run in 2021. The company makes hydrogen fuel cell systems, and considering the narrative has failed to bring it fruit during the Biden Era, things are probably going to be even tougher in the next four years for this stock.

The Trump administration could pull back most subsidies for clean energy programs, and that would most likely cause the stock to head to zero. The hydrogen fuel cell market has been getting more competitive as companies with deeper pockets enter. On the other hand, Plug Power’s financials have headed in the opposite direction.

Losses have only trended away from the breakeven line and the cash balance is now low enough that Plug Power is turning to dilution.

Losses have only trended away from the breakeven line and the cash balance is now low enough that Plug Power is turning to dilution.

As such, I think it is only a matter of time until it enters a cycle of more dilution and reverse stock splits.

As such, I think it is only a matter of time until it enters a cycle of more dilution and reverse stock splits.

Core Scientific (CORZ)

Core Scientific (NASDAQ:CORZ) is mostly a Bitcoin (BTC-USD) mining company. But much like most Bitcoin mining companies in the past year, it has been trying to sell itself as a data center and an AI HPC company. Most Bitcoin miners have failed to take advantage of Bitcoin’s increase in price and were hit hard by the halving. Miners delivered stellar gains in the last cycle, but they’ve barely delivered any upside in the current one.

Core Scientific (NASDAQ:CORZ) is mostly a Bitcoin (BTC-USD) mining company. But much like most Bitcoin mining companies in the past year, it has been trying to sell itself as a data center and an AI HPC company. Most Bitcoin miners have failed to take advantage of Bitcoin’s increase in price and were hit hard by the halving. Miners delivered stellar gains in the last cycle, but they’ve barely delivered any upside in the current one.

CORZ has been an outlier here. It filed for Chapter 11 bankruptcy in 2022 but it successfully got back on its feet in early 2024 after it reduced its debt by $400 million through the conversion of equipment lender and conversion note holder debt to equity. The stock has surged since then as it secured HPC hosting contracts with CoreWeave with potential revenue exceeding $8.7 billion over 12-year agreements. CoreWeave’s biggest client (by far) is Microsoft (NASDAQ:MSFT), which has started to cancel its data center contracts.

I don’t think the contract with CoreWeave be able to reach its full potential, and even if it did, the earnings don’t seem enough to justify the price. If you add in a broader market correction with weak Bitcoin performance, CORZ could start tumbling again. Outstanding shares increased by nearly 50% in Q3 2024, and it’ll likely increase more since it needs to service the huge debt pile and build out the infrastructure for the contracts it has landed.

Its Altman-Z score of -7.37 also implies a high risk of bankruptcy.

— Omor Ibne Ehsan

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning