You’ll find undervalued stocks in most market conditions as investors get overly bullish on certain industries and leave others behind and value them irrationally. These stocks then eventually recover once the pendulum swings the other way.

Everyone has been piling into the hottest tech and AI stocks recently, and this has undone the risk-off sentiment investors had two years back. The rotation of gains into these hot tech companies has lifted them significantly, but it has ended up crushing certain stocks, which now trade well below the fair price. These undervalued stocks could end up delivering triple-digit returns on their way back up.

Of course, it is hard to say when that will happen, but the cheap stocks we’ll be looking into have limited downside risk and significant upside potential in the coming years. Let’s take a look.

Dollar General (DG)

Dollar General (NYSE:DG) is one of the hardest-hit retail stocks you can buy. The stock is down 71% from its November 2022 peak, which is quite shocking when you put more thought into it. Dollar General was supposed to be a beneficiary of any economic volatility and has the reputation of being the place where people go if they are in a cash crunch.

However, the opposite happened. The company’s lower-income customer base was disproportionately impacted by persistent inflation and higher borrowing costs. This led to reduced discretionary spending and weaker-than-expected same-store sales growth of 0.5% year-over-year in Q3 2024. Q3 diluted EPS dropped 29.4% year-over-year to $0.89.

Customers also reported cluttered stores and this was while Walmart (NYSE:WMT) and Dollar Tree (NASDAQ:DLTR) were making products much more competitive price-wise.

Customers also reported cluttered stores and this was while Walmart (NYSE:WMT) and Dollar Tree (NASDAQ:DLTR) were making products much more competitive price-wise.

Nonetheless, I think Dollar General has what it takes to successfully turn the ship around. It is reducing employee turnover and streamlining fulfillment centers to cut costs and improve inventory management while adjusting its product mix to put essentials and competitive pricing first.

Dollar General’s growth is still positive and it is profitable. Analysts expect mid-single-digit top-line growth to continue and the margin squeeze to start reversing in the 2026 fiscal year. There’s a price target as high as $170. I also think this also could be a stealth real estate play since it operates 92% of its stores under triple-net leases.

And finally, you can sit on its 3.15% dividend yield as you wait for DG to make a recovery.

The Hershey Company (HSY)

Hershey Co (NYSE:HSY) has been flat in the past five years and is down over 43% from its May 2023 prices as Ivory Coast (the world’s largest cocoa producer) saw severe flooding and the supply shock caused soaring cocoa prices. Just as the company started to recover, cocoa prices again spiked to $13,000/metric ton in late 2024 due to poor West African harvests. Input costs soared and this led to adjusted gross margins falling. Management expects this to last through 2025 and warned of a mid-30% adjusted EPS decline in 2025 as cocoa hedges expire.

That said, HSY is among the cheapest stocks you can buy considering how solid the brand is. Q4 results have been pretty good as Hershey reported adjusted EPS of $2.69, surpassing analysts’ expectations of $2.38 by 13%. Net income recovered by 128.2% year-over-year to $796.6 million. Q4 revenue also grew 8.7% year-over-year to $2.89 billion.

That said, HSY is among the cheapest stocks you can buy considering how solid the brand is. Q4 results have been pretty good as Hershey reported adjusted EPS of $2.69, surpassing analysts’ expectations of $2.38 by 13%. Net income recovered by 128.2% year-over-year to $796.6 million. Q4 revenue also grew 8.7% year-over-year to $2.89 billion.

You may have to wait for this recovery to fully play out as Hershey’s still expects margin pressures in 2025, but I think the negatives are more than priced in right now. You’re also getting a 3.4% dividend yield as a sweetener.

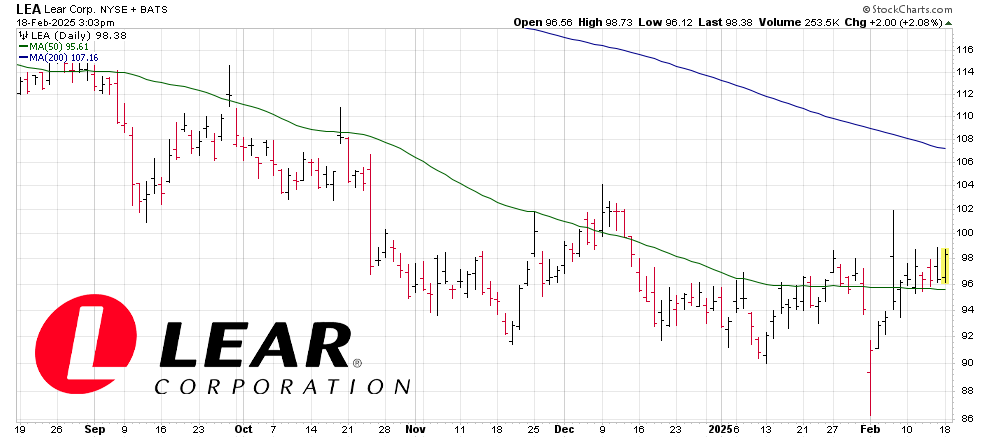

Lear Corp (LEA)

Lear Corp (NYSE:LEA) isn’t as well-known. The company makes automotive seating and electrical systems. LEA stock has been continuously declining since 2021, but I think a turnaround could be just around the corner as automakers start getting hold of their bearings with interest rates coming down globally.

The stock is down about 51% from its 2021 peak, but analysts expect the company’s bottom line to finally start growing starting this year, with 0.45% growth, though 2026 is expected to see 20.6% EPS growth. Revenue is also expected to start recovering from 2026 with mid-single-digit growth. It expects free cash flow of up to $430-630 million this year.

I believe the recovery should also lift the stock as you’re just paying 7.6 times forward earnings and just a fifth of sales for the stock.

I believe the recovery should also lift the stock as you’re just paying 7.6 times forward earnings and just a fifth of sales for the stock.

Analysts think it can reach up to $170, which implies about 74% upside from here.

— Chris Johnson

The legendary stockpicker who built one of Wall Street's most popular buying indicators just announced the #1 stock to buy for 2026. His last recommendations shot up 100% and 160%. Now for a limited time, he's sharing this new recommendation live on-camera, completely free of charge. It's not NVDA, AMZN, TSLA, or any stock you'd likely recognize. Click here for the name and ticker.

Source: Money Morning