Wall Street shook off slightly ‘hot’ January inflation data on Wednesday as the bulls continued to hold their ground around the S&P 500 and the Nasdaq’s 50-day moving averages.

Nothing has moved the bulls out of their holding pattern to start 2025. The DeepSeek artificial intelligence news, big tech earnings, and possible tariff battles have been nothing more than blips on the radar.

Today’s episode of Full Court Finance at Zacks dives into two under-the-radar growth-focused tech stocks—Nu Holdings and Wix.com Ltd.—to consider buying before their upcoming earnings releases.

Warren Buffett’s $15 Fintech Stock: Why NU is a Must-Buy for Investors

Nu Holdings Ltd. (NU Quick) is a fintech and digital financial services powerhouse rapidly expanding its reach in Brazil, Mexico, and Colombia.

The Brazilian fintech firm has shaken up the banking and financial services sector in large economies with huge populations via its app, credit cards, loans, and more.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Nu grew its customer base by 23% YoY in Q3 to reach 110 million. Nu is one the largest digital banking platforms outside of Asia and one of the largest financial institutions in Latin America, boasting that more than 1 in every 2 Brazilian adults is a customer.

Nu is projected to grow its adjusted earnings by 75% in 2024 and 39% in 2025 after expanding its bottom line from $0.02 to $0.24 between 2022 and 2023.

Nu grew its revenue by 68% in 2023. Nu’s revenue is expected to jump 47% and 35%, respectively to double its revenue from $8 billion in FY23 to $16 billion in FY25.

This backdrop is why Warren Buffett’s Berkshire Hathaway owns Nu shares.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Nu’s earnings revisions have stagnated recently and investors were disappointed that it didn’t provide better guidance last quarter. Still, Nu has topped our EPS estimates by 20% in the past two quarters and the stock already took a big hit.

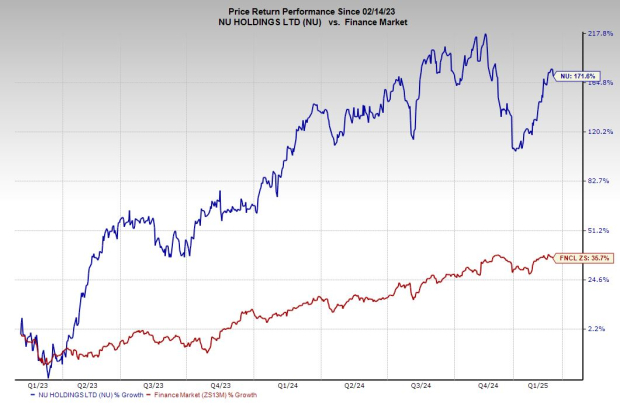

NU stock tanked after its Q3 earnings release. It has recovered a sizeable chunk of that pullback after buyers stepped in at its 52-week lows.

Nu has jumped 170% in the past two years (vs. Tech’s 76%) and 15% since its December 2021 IPO. At around $13.80 a share, NU trades 14% below its peaks and its average Zacks price target.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

NU stock might face selling pressure after its comeback took it from oversold RSI levels to overbought. But its long-term outlook remains intact.

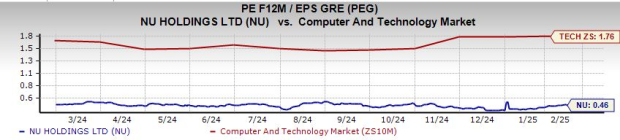

NU’s valuation levels have improved, trading at a 98% discount to its all-time highs at 22.1X forward 12-month earnings and 18% below Tech. The fintech stock’s 0.5 PEG ratio (factoring in its earnings growth) represents a 72% discount to Tech.

Nu reports its Q4 earnings results on February 20.

Buy This Soaring AI-Boosted Tech Stock for at Least 35% Upside?

Wix.com Ltd. (WIX) sells intuitive, user-friendly tools to help its customers essentially DIY (do-it-yourself)-style build their website through Wix’s array of offerings. The company over the last handful of years raced to introduce far more features to attract professional website builders to expand its reach and boost profits.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Wix’s ongoing portfolio makeover and artificial intelligence features have helped it successfully grow beyond DIY. The company grew its Q3 revenue by 13%, with ‘Partners’ revenue up 30%. “Bookings growth accelerated to 16% y/y in Q3, driven by Studio momentum, ramping benefits from our AI product suite, robust commerce activity and strong business fundamentals,” CFO Lior Shemesh said in prepared Q3 remarks.

Wix has gone all-in on profitability to accommodate the higher interest rate environment that no longer values growth at all costs.

Wix swung from a GAAP loss of -$7.35 a share in 2022 to +$0.55 in 2023 and +$1.60 in the trailing 12 months. The software company said last quarter that is “well-positioned to achieve and surpass the Rule of 40” (revenue growth rate + profit margin exceeding 40%) in FY24, a full year ahead of schedule.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Wix is projected to grow its revenue by 13% in 2024 and 14% in FY25 to reach $2 billion. This growth outlook matches its 2023 top-line expansion. Meanwhile, it is projected to grow its adjusted earnings by 39% in 2024 and another 20% in FY25.

Wix’s upbeat earnings revisions lands it a Zacks Rank #2 (Buy). The recent EPS revisions positivity is part of a stellar run that began in early 2022. Plus, the company topped our EPS estimates by an average of 20% in the trailing four quarters.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

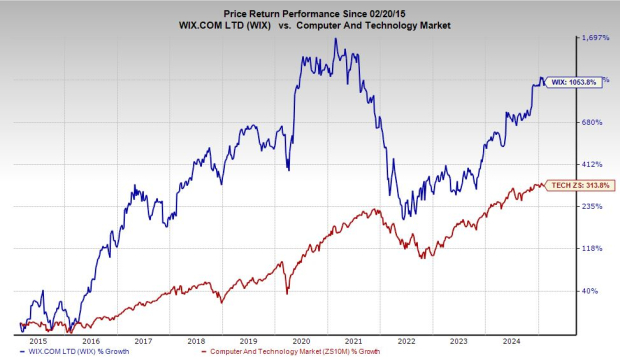

WIX stock has ripped 165% higher in the last two years to double the Tech sector, including a 75% run in the past 12 months vs. Tech’s 22%.

The website software stock has climbed 1,050% in the past decade to triple Tech. Yet, Wix trades 35% below its 2021 peaks. WIX is holding ground at its 2020 breakout levels and 50-day moving average.

The biggest things holding Wix stock back are its valuation and balance sheet. If it can continue to grow its earnings, and start generating more cash and larger margins the stock could continue to march toward its records.

Wix is set to release its Q4 results on February 19.

— Benjamin Rains

Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report.

Source: Zacks