If you’re looking for outsized gains that can boost your portfolio’s returns to beat the benchmark, growth stocks are always the go-to. Unfortunately, the recent rally makes it quite difficult to find the right growth stocks to buy since most are at nosebleed valuations and are still rallying. It may seem like none of these growth stocks have triple-digit potential.

However, there are still a few undervalued growth stock candidates that can deliver such returns. The stars would have to align for them to do it, but these stocks are trading cheaper than most of their peers and have the growth potential to deliver substantial gains by the end of this year. We will be taking a look at three such growth stocks:

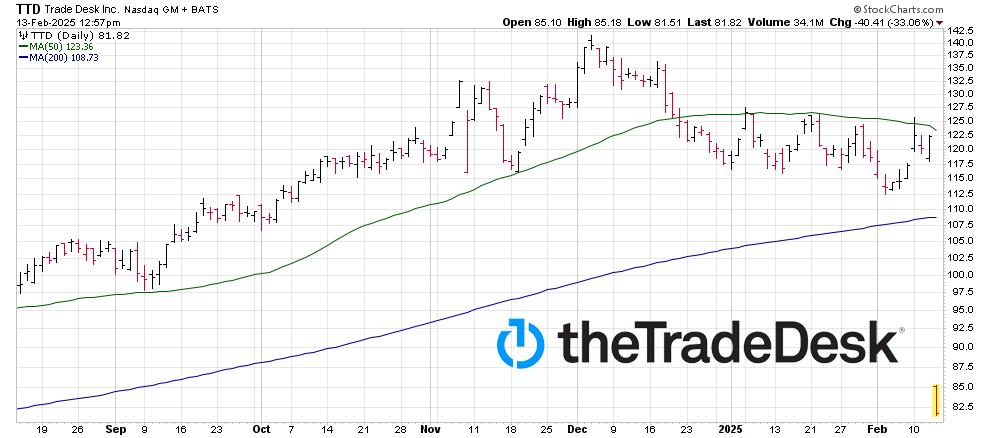

The Trade Desk (TTD)

The Trade Desk (NASDAQ:TTD) plunged massively after its Q4 earnings call and is down 40% from its peak in December. The company reported Q4 revenue of $741 million, which grew 22% year-over-year but missed its own guidance of “at least $756 million” and consensus estimates of $760 million.

Moreover, Q1 2025 revenue guidance of $575 million (up 17% year-over-year) and adjusted EBITDA of $145 million fell short of analyst expectations ($582 million and $193 million, respectively). Plus, Block & Leviton launched an investigation into potential securities law violations, citing the revenue miss as a key trigger. Investors who suffered losses are being urged to join the probe.

The Trade Desk is also seeing a slew of downgrades and price target reductions from various analysts. The current price target of $129.3 still implies 55.8% upside potential.

Regardless, I’m still bullish here despite the amount of bearishness gripping the company. Wall Street usually outdoes things, and while the recent miss is pretty bad, it is still recoverable and a 40% dip seems more than worth buying.

TTD processed $12 billion in ad spend in Q4 2024, with CTV being its fastest-growing channel. Analysts expect a 21% revenue CAGR through 2026 and political ad spending in the coming years are positive catalysts that could push the stock back up.

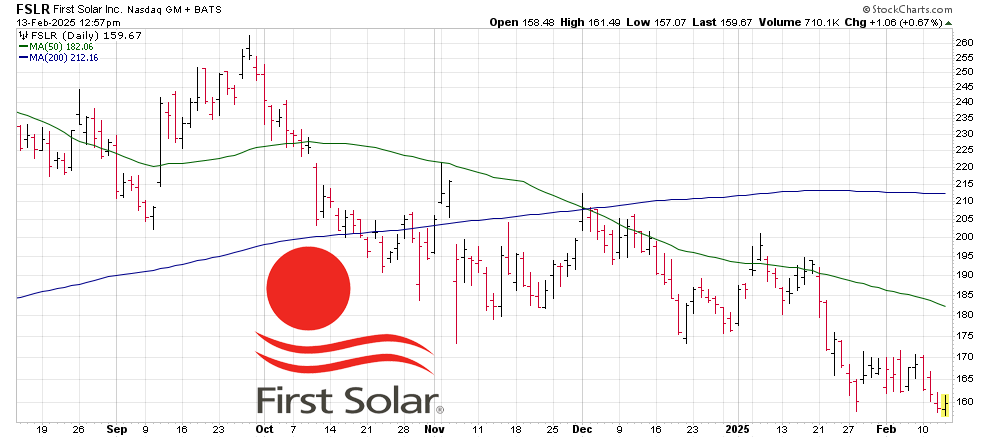

First Solar (FSLR)

First Solar (FSLR)

First Solar (NASDAQ:FSLR) has also been sliding down and has declined 30.8% in just the past six months. It is down almost 47% from its June 2024 peak. And that’s despite optimism from analysts due to the technological edge it has in the solar industry.

Manufacturing defects in Series 7 panels (produced in 2023–2024) led to a $50–$100 million warranty charge to address premature power loss risks. It also revised its 2024 sales guidance to $4.1–$4.25 billion (from $4.5 billion midpoint) due to contract terminations and unfavorable pricing in markets like India.

The biggest risk bears see is the expiration of tax credits and the freezing of other Biden-era incentives. However, the Trump administration could offset that greatly as the U.S. could impose significant tariffs on foreign solar manufacturers in the coming years. Since First Solar is U.S.-based, it has a lot to gain from that. The solar market is projected to grow at a 19.68% CAGR to $541.84 billion by 2031.

All that said, it is one of the stocks that could deliver triple-digit gains this year. It has a 75 GW sales backlog and the consensus price target of $276.4 implies some 72.9% upside potential in the coming year. Q4 2024 results (due Feb 25) are expected to show 44% year-over-year EPS growth to $4.69. This could lead to a turning point for the stock if it manages to outperform these estimates. If not, shareholders will likely go through more pain before it turns the corner.

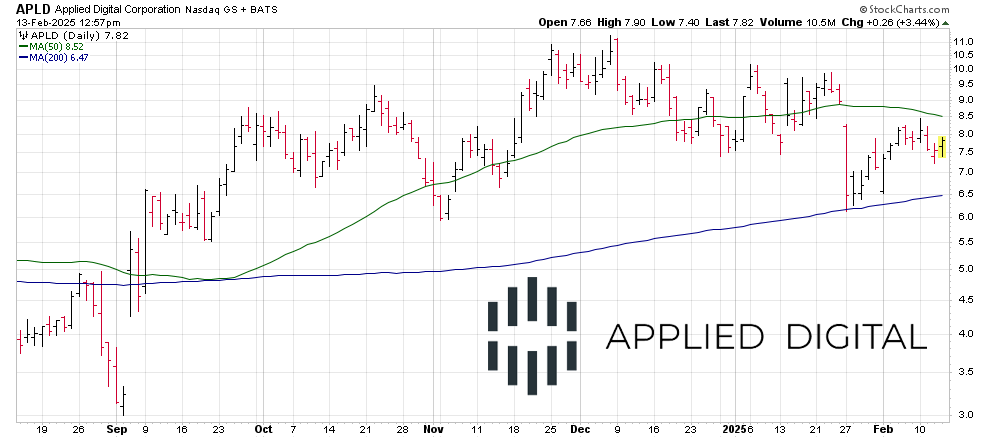

Applied Digital (APLD)

Applied Digital (APLD)

Applied Digital (NASDAQ:APLD) is a pretty controversial play, but it has significant potential. Bears are mostly worried about this company’s links to the crypto market, but I believe it isn’t something to worry much about.

Applied Digital is making a quick transition into an AI data center company and should no longer be looked at as a crypto miner. It secured a $5 billion perpetual equity financing facility with Macquarie Asset Management for its Ellendale HPC campus, with an initial $900 million investment.

Moreover, it closed a $375 million debt financing agreement with Japan’s SMBC to expand hyperscale data center capacity and completed a $450 million convertible notes offering to fund AI infrastructure projects.

Cloud services revenue grew by 523% and carried the Q2 FY2025 revenue up 51% year-over-year to $63.9 million. Its technical infrastructure is Nvidia (NASDAQ:NVDA)-endorsed and analysts have a consensus price target of $12, implying 52.3% upside. With that in mind, there’s a good chance this stock will deliver triple-digit gains if the AI rally continues.

— Omor Ibne Ehsan

— Omor Ibne Ehsan

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning