It’s literally been the one stock that has represented the strongest theme driving the market higher, and it just broke.

Shares of Palantir (PLTR) have posted an amazing 300% return over the last year. To put that into perspective, the average return for the Magnificent Seven stocks is 63% including 169% gains from NVIDIA (NVDA).

Palantir’s rapid rise to the top of the AI trade has more to do with the sentiment surrounding the stock than it does the P/E ratio and other measures that stocks are held up against.

The run, which will likely continue quickly, has more to do with the stock’s expectations than it does anything else.

Let’s dive into the long-term bullish outlook for Palantir and where you may want to “buy the Dip.”

Palantir and the Wall of Worry

“Stocks climb a wall of worry”.

Most investors have heard it but they don’t want to understand how it can propel a stock higher.

The best way to portray Palantir’s Wall of Worry is with a chart of the current analyst recommendations for the stock.

Currently, 19% of the Wall Street analysts recommend shares of Palantir as a “buy”. Let’s just give you the raw number, it’s 3. Despite Palantir’s great performance, only 3 analysts rate the stock a “Buy”.

Just compare that to NVIDIA’s 48 buy recommendations.

The situation creates a problem for NVIDIA and an opportunity for Palantir due to the “Wall of Worry”.

Palantir is emerging as a different company than it was a year or two ago.

Earnings per share and revenue are consistently beating analysts’ expectations. In addition, Palantir’s management is now issuing forward-looking guidance that is better than Wall Street’s expectations.

Put simply, Wall Street is on the wrong side of the Palantir trade, which is likely to help shares over the next 6-12 months.

In November, Alex Karp, CEO of Palantir, was interviewed on CNBC and the subject of Wall Street’s expectations came up.

The CEO expressed the relationship between Wall Street and Palantir with this quote…

“People have been saying we are overvalued for 20 years. People have been saying our products wouldn’t make us profitable. That we would not be able to become a juggernaut. That we would not become GAAP profitable. That we wouldn’t get on the S&P. Keep saying that about us. We love it. It discourages people from doing anything like what we’re doing. And we are winning.”

He’s right, Palantir is winning.

Palantir’s P/E Ratio is Not the Problem

It’s been the Palantir Bear’s argument for the last six months.

Palantir’s P/E ratio is “trading” at 186 and that’s a resounding sign that the stock is overvalued.

Enter the simple lesson on over- and under-valued stocks here.

A stock is only as valuable as the market sees, this is the reason that speculation is the most important driving factor in the market.

When investors see an opportunity for a stock to grow revenue and earnings they want to get into that stock as early as possible. They want to speculate that the results for the company will get better.

The earlier they are the higher the PE Ratio goes until the expected increase in earnings brings that “valuation” lower again.

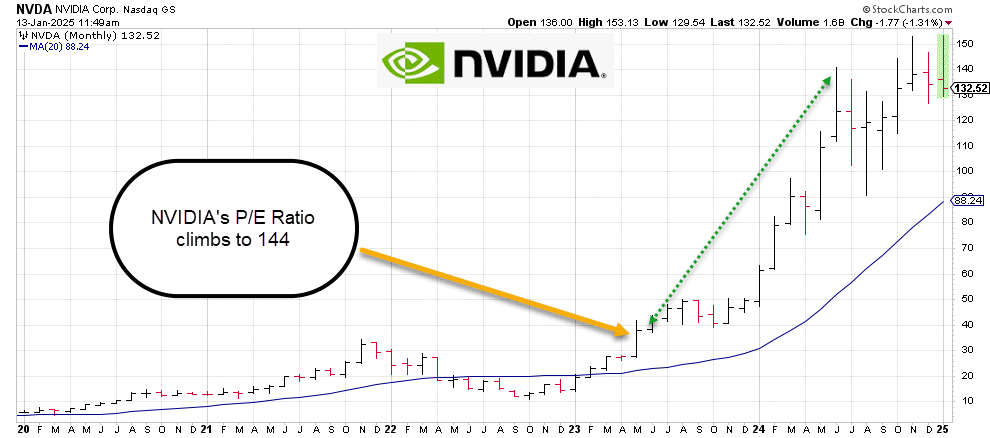

We’ve seen this before with NVIDIA.

In the second quarter of 2023 NVIDIA’s P/E Ratio shot from 60 to 145. The reason was that investors had seen some good news from the company’s earnings releases and sensed that the trend was going to continue.

Investors immediately bid the stock from $27 to $50 and then to $100. The reason that the P/E ratio came back down was that NVIDIA’s results started to meet the speculation reflected by higher prices.

A similar situation has been brewing with Palantir.

A similar situation has been brewing with Palantir.

As of today, the P/E ratio for Palantir is at 186.

Like NVIDIA in 2023, Palantir is seeing its pipeline of products begin to result in revenue increases on a quarterly basis. Simply put, the company is growing into its price valuation.

Last quarter, Palantir beat analyst expectations for revenue and earnings per share. The company also raised their guidance for the current quarter and 2025.

Investors once again drove the stock price higher – a natural reaction – pushing the stock’s P/E ratio higher again.

The point here is that investors used the P/E ratio to gauge whether they should buy a stock or not they would consistently miss opportunities with growth stocks.

Palantir’s Current Selloff Will Create an Opportunity

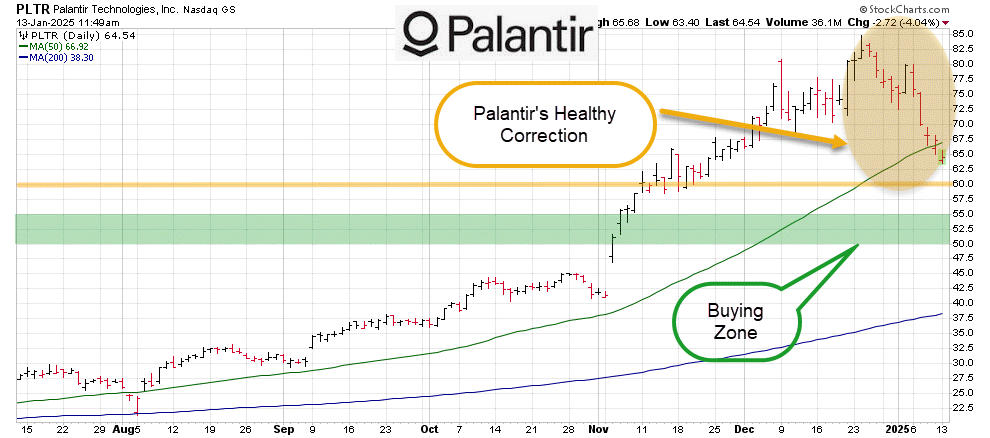

Palantir’s stock is now trading below its 50-day moving average for the first time since August.

In August, the stock dropped 10% ahead of the company’s earnings, breaking through its 50-day moving average.

The stock has been pressured lower by general market selling as interest rates move higher and investors cope with a sudden rise in uncertainty in the market.

For some investors, Palantir’s move below its 50-day should be seen as the preparation for a buying opportunity for the stock.

Already trading 25% lower than its December highs, Palantir has completed what we refer to as a “healthy correction”.

Healthy corrections are dips or corrections in a stock’s long-term bull market trend.

These corrections are necessary to “reset” the balance of buyers and sellers in a stock.

Here’s How Far Palantir Will Correct

Here’s How Far Palantir Will Correct

As mentioned, Palantir shares are below their 50-day moving average. Investors should expect to see some buyers come to test that support, but the overall market weakness suggests that Palantir will head lower.

From a chart perspective, any additional selling pressure should begin to mount on Palantir stock through the week, accelerating the decline towards the next support level of $55. This marks the price that Palantir started its bullish trend following last quarter’s earnings surprise.

Just $5 lower is the psychologically significant $50 which should act as a stronghold for Palantir shares.

Palantir is Still a Long-Term Buy

Wall Street may not agree, but Palantir is displaying all three components of a bullish stock.

Shares of Palantir remain in a long-term technical bull market and are currently in a short-term correction.

Palantir’s fundamental performance remains positive as the company is growing its revenue and earnings.

Sentiment remains pessimistic towards Palantir. This means that that stock still benefits from its Wall of Worry.

Long-term investors should expect to see Palantir bounce from this short-term correction and continue towards a long-term target of $100.

— Chris Johnson

$3 billion+ in operating income. Market cap under $8 billion. 15% revenue growth. 20% dividend growth. No other American stock but ONE can meet these criteria... here's why Donald Trump publicly backed it on Truth Social. See His Breakdown of the Seven Stocks You Should Own Here.

Source: Money Morning