Inflation is falling—but is a recession next, or will we get that vaunted “soft landing” Jay Powell keeps talking about? Wouldn’t it be great if there was a dividend-payer built for either outcome?

Just such an income play exists—it’s called a covered-call closed-end fund (CEF). They’re smart buys now because they pay big dividends: the CEF we’ll break down today—the Nuveen Dow 30 Dynamic Overwrite Fund (DIAX)—yields a healthy 7.8%.

That not only gives us a high income stream, but it also increases our safety, as we’re getting the vast majority of our return in safe dividend cash.

That’s one part of DIAX’s appeal—especially if a recession is headed our way (more on that shortly).

The second benefit with a CEF like DIAX is that it sells covered-call options. This means DIAX sells the right to buy stocks from its portfolio for a fixed price at a fixed time in the future. If the stock hits that price, it gets sold, or “called away” in option-speak.

But no matter how these trades play out, the fund keeps the “premium”—or the sum it charges for the option. It’s a smart way to subsidize an income stream, and it works best in a volatile market.

Finally, DIAX, as you can probably tell from the name, holds the large caps of the Dow Jones Industrial Average—firms with strong cash flows that can weather a recession, such as Apple (AAPL), Caterpillar (CAT) and American Express (AXP).

But what about that recession? Can we expect it anytime soon? Let’s look at that now, starting with the state of play with inflation.

Price Gains Keep Slowing

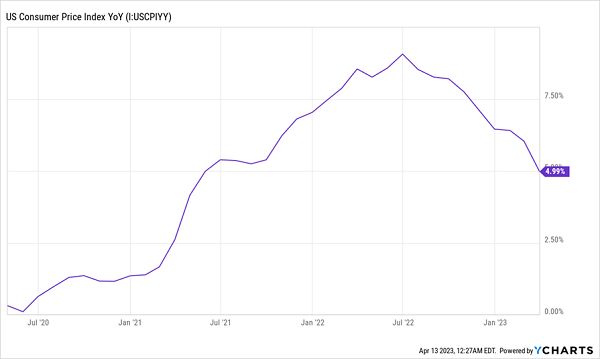

As we saw in last week’s inflation report for March, the consumer price index has fallen to mid-2021 levels, and 2020 levels are probably going to come in the next few months.

As we saw in last week’s inflation report for March, the consumer price index has fallen to mid-2021 levels, and 2020 levels are probably going to come in the next few months.

Of course inflation hasn’t disappeared entirely—and that’s a good thing. No inflation means no consumer demand, which means a recession. And that remains a risk that’s not only on everyone’s mind, but a key consideration when mapping out what markets will do over the next few months.

Before we talk recession odds, let’s stop and rejoice at just how far inflation has fallen. Last month’s 5% growth in prices from a year ago was a great data point, but not the best. The 0.1% rise in prices from February to March 2023 was microscopic, and well under economists’ expectations.

This means the Federal Reserve can ease off its string of rate hikes, which have already caused cracks in the banking sector and markets more broadly.

Skyrocketing Rates Finally See Land

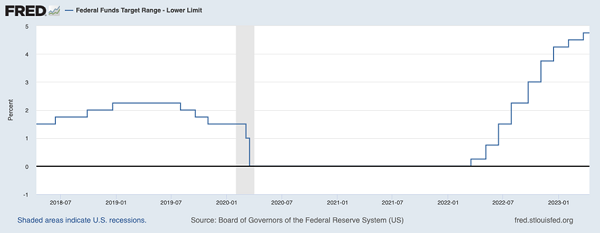

After hiking rates at the fastest rate in living memory, and to a level we haven’t seen in many years, the Fed has said they’re finally about done. The futures markets agree, predicting just one more hike, at the Fed meeting in early May.

After hiking rates at the fastest rate in living memory, and to a level we haven’t seen in many years, the Fed has said they’re finally about done. The futures markets agree, predicting just one more hike, at the Fed meeting in early May.

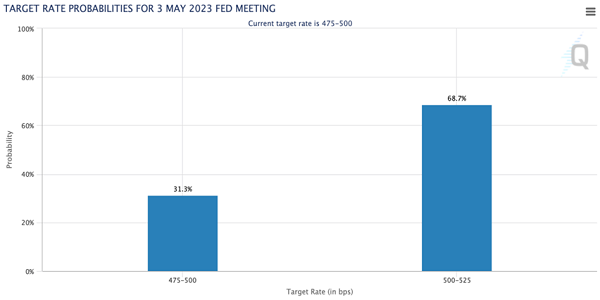

Source: CME Group

Source: CME Group

That increase is likely to be followed by a pause. More importantly, the Fed wants us to know this. The Federal Reserve recently released notes from its meeting of policymakers, several of whom “considered whether it would be appropriate to hold the target range steady at the meeting,” referring to the rate hike in March.

The Fed raised rates anyway, but only by 25 basis points, both the smallest hike this cycle and the smallest possible. After another small hike, we may be done with interest rate hikes for the foreseeable future.

But Is a Recession Coming?

Now that rates are no longer going to soar, markets will need to find something else to obsess over. And the most obvious contender is a recession.

Of course, that isn’t new. Worries about the Fed hiking us into an economic collapse have been in the news, and a topic at Wall Street business lunches, since early 2022.

Will it come or not? No one really knows. At least so far, retail sales and GDP data aren’t just good but improving—meaning the recession isn’t going to arrive tomorrow or even next month. In fact, it might mean that the recession we’re all waiting for doesn’t show up for a couple of years.

The Priced-In Collapse

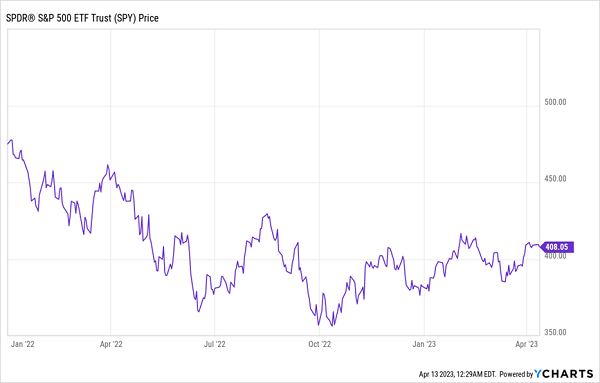

And since stocks tanked in 2022 waiting for the recession that didn’t happen—pictured above by the performance of the benchmark SPDR S&P 500 ETF Trust (SPY)—we can’t say the upcoming recession will tank stocks. It already has! For stocks to plunge even further, the recession will have to be quite severe indeed.

And since stocks tanked in 2022 waiting for the recession that didn’t happen—pictured above by the performance of the benchmark SPDR S&P 500 ETF Trust (SPY)—we can’t say the upcoming recession will tank stocks. It already has! For stocks to plunge even further, the recession will have to be quite severe indeed.

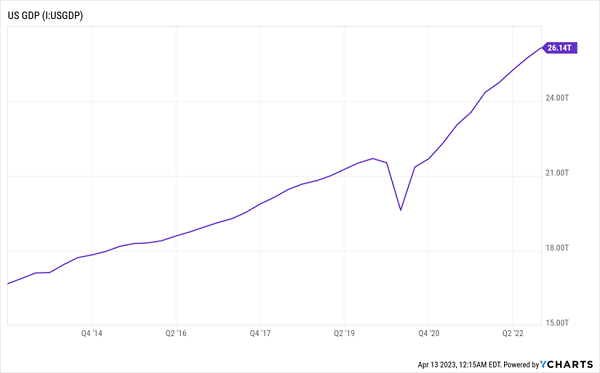

Growth, Not Recession

And with GDP actually rising faster than it was a few quarters ago, it looks like we have a long time before a deep recession pushes stocks down from their current level.

And with GDP actually rising faster than it was a few quarters ago, it looks like we have a long time before a deep recession pushes stocks down from their current level.

Markets realized this at the start of the year. Knowing that the mood changed sharply with the new year, stocks have continued to rise, despite the collapse of a handful of banks, which governments and central banks were quick to contain.

The bottom line is that now is a great time to buy. There are simply too many bargains out there after last year’s extreme overselling.

But if you aren’t fully convinced, I get it. This is why 7.8%-yielding DIAX is a solid conservative play, with a high dividend, strong portfolio and call-option strategy that holds up well when volatility strikes. And since DIAX holds all the firms in the index, you’re getting tremendous diversification, too.

One other thing: as a CEF, DIAX can, and often does, trade for less than the value of its portfolio—or its net asset value (NAV). Right now, DIAX’s discount stands at 6.9%, meaning you’re 93 cents on the dollar for that huge income stream, as well.

That sounds a lot better than keeping your money in cash, where inflation is chipping away at its value—especially if a recession still takes years to arrive.

— Michael Foster

These Incredible CEFs Make Money 90% of the Time (and Yield 10%+) [sponsor]

I checked the numbers on CEFs and found something astonishing: the most well-established of the bunch have an unparalleled safety record—they make money 90% of the time!

And their dividends? Incredible. The average CEF yields well north of 7% today. And the top five I’ve uncovered for maximum safety and maximum income yield way more—a blockbuster 10% average yield!

I’ve published my complete findings on CEFs’ astonishing safety ratings and why they’re the perfect investments for this uncertain market—with big dividends and bargain valuations that set us up for big capital gains, too!

Click here and I’ll tell you the full story on these CEFs’ sterling safety records and show you how to download a free Special Report naming my top 5 CEFs to buy now, hold for life—and collect huge 10.1% yearly dividends while you’re at it.

Source: Contrarian Outlook