While it’s debatable whether fintech stocks are truly cheap, the space has been suffering for months lately and many fintech companies still provide significant value to investors. After all, financial technology companies are trend setters: They are forming the next standards for global financial transactions, of which the world is finally ready to commit to.

As such, my goal here is to help investors identify the best fintech stocks to accumulate shares of during mid- to long-term swings while they remain “cheap.” The three fintech companies I’ll examine today are leaders among the group.

But before we dive into each analysis, let me set a few ground rules. When attempting to catch a “falling knife,” I need to see solid current fundamental metrics. While innovation is exciting, I avoid idea stage companies. When stocks are falling out of control investors need tangible numbers to lean on. Second, I also seek stocks that have fallen into potential support levels.

The following companies have excellent fundamentals and are free fall stocks. One more rule: Even though I am optimistic for the upside opportunity, I must advise caution in the short term. The situation in the Ukraine is getting worse and the players are not budging. Politicians like negotiate in the headlines, which creates fake rallies and unnecessary corrections. I am confident these stocks will make a comeback, but I also respect the macroeconomic and geopolitical risks at hand.

Without further ado, the three fintech stocks to buy are:

- Block (NYSE:SQ)

- PayPal (NASDAQ:PYPL)

- SoFi (NASDAQ:SOFI)

Fintech Stocks to Buy: Block (SQ)

Source: Charts by TradingView

Source: Charts by TradingView

Square recently rebranded as Block, which is testament to its boldness. Block has been a driving force in the space, pushing the limits for the sector. The old dogs are scrambling to keep up with it, so we are all better for it. Remember, these are companies that are healthy, and there is room for all of them to prosper.

SQ stock has the backing of excellent financial metrics. There is no way to negatively spin growth like that which it delivers. Last year’s revenues were seven times larger than just five years ago. And the company managed to do this while also delivering a positive net income since 2019. The critics will have to be creative to find fault with this report card.

Naysayers might harp on the high price-to-earnings ratio (P/E), and they’d be wrong. Delivering this aggressive growth is impossible if management focuses too much on profitability. This was the complaint with Amazon (NASDAQ:AMZN) for ten years before the haters figured it out. According to TradingView, SQ’s price-to-sales (P/S) ratio is under 3x, so investors have realistic expectations.

Lastly, Block has been on sale for months. Despite of its ever-improving profit and loss (P&L) statement, the sellers have not stopped pushing it down since last summer. From the highs, SQ stock lost as much as 70% of its value. Finally it bounced off the 2020 summer breakout neckline. Pivotal zones like this usually provide lasting support. There are willing buyers lurking and waiting for the opportunity they missed in 2020.

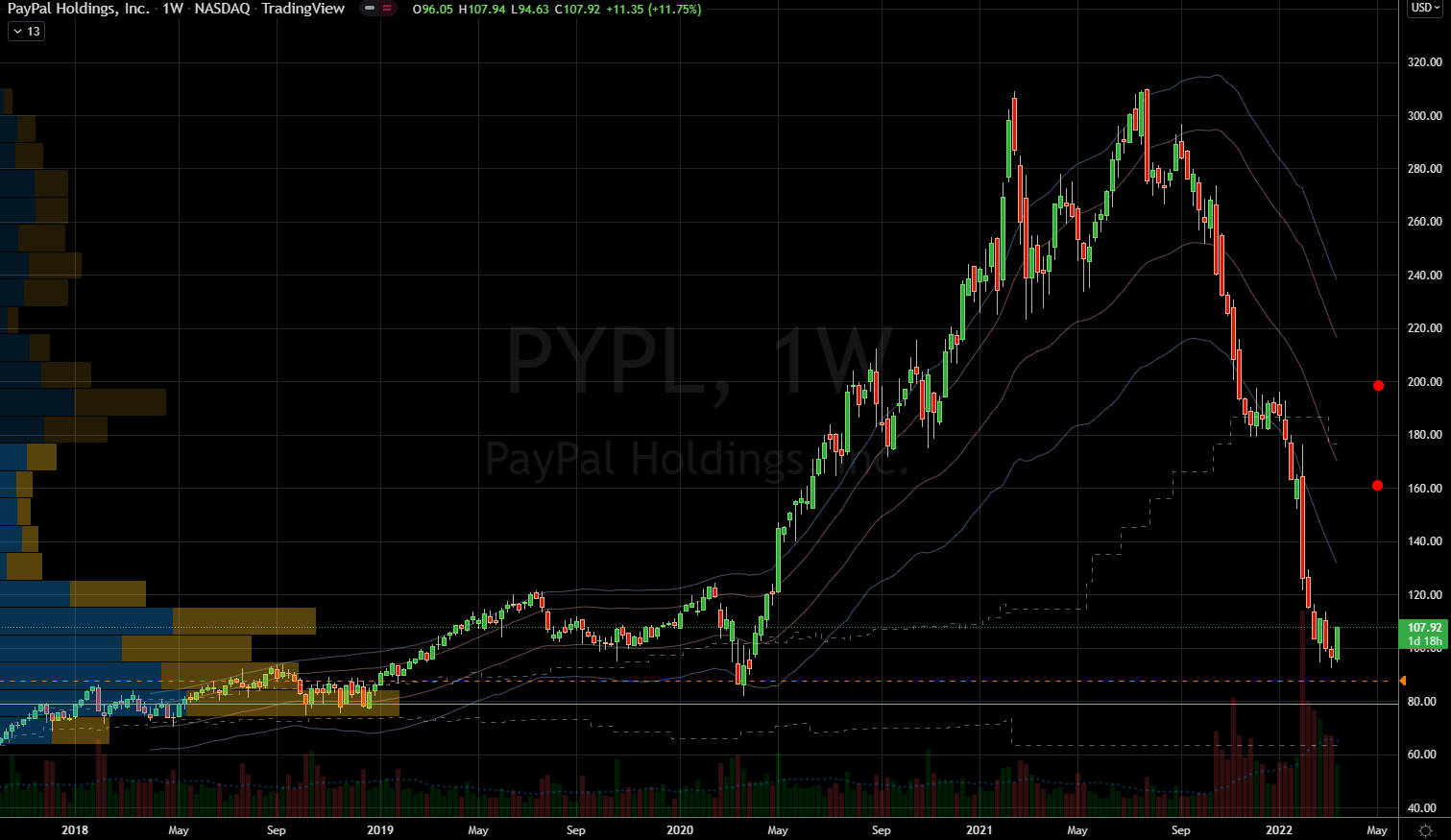

PayPal (PYPL)

Source: Charts by TradingView

Source: Charts by TradingView

Overall, the arguments I made for SQ still apply to PYPL stock. There are technical differences with the stock’s “speed” on the charts. For example, PYPL tried to find support late last year; whereas, SQ took a more terminal velocity approach. But, in the end, each stock hit rock bottom and is now trying to bounce.

PayPal investors rejoiced with a 7.5% climb on Tuesday, which was less than SQ, but still a great day. But before we sound the all-clear, we must first acknowledge that rallies have happened before. The problem has been with sustainability, like the stints in December and January. Each of these rallies showed promise but then failed miserably.

I would feel much more at ease when this rally exceeds $116 per share. While it won’t be an end zone, it would score one win for the bulls, beating the major fail of Feb. 28. Even then, this would be step one of many to come. The bulls could struggle with every level they tried to hold on the way down. But after a couple of weeks, they would develop a tailwind of an ascending trend.

This would change the logic to buy dips instead of selling spikes. When it comes to fundamentals, PYPL is no slouch either. The company has nearly doubled its revenues since 2017 and has enjoyed a whopping $4.2 billion in net income. The critics won’t have a bone to pick since it’s competitive with Apple (NASDAQ:AAPL) in absolute terms. PYPL sports a 28.6x P/E and 4.7x P/S, whereas Apple’s are 26x and 7x, respectively.

SoFi (SOFI)

Source: Charts by TradingView

Source: Charts by TradingView

If I had to designate a black sheep among this trio of fintech stock to buy, it would be SoFi. Unlike the previous two companies, SOFI has many disadvantages. First off, it is too new to have any benefit of doubt on Wall Street. More importantly, SOFI stock fell into new all-time lows because of its youth. This puts the bulls in a technical disadvantage to the sellers. The buyers no longer have reference points to try and catch it. Falling into a chasm weakens investors’ courage.

Second, SoFi is lacking in the financial metrics department. It needs more time to develop these metrics to make a strong judgement. Eventually it should earn the kudos it deserves, but for now investors are shying away. Nevertheless, according to Yahoo Finance SoFi has grown its revenues 2.3 times since 2018. That is impressive growth inside a growing sector.

The addressable market is growing as fast as the company, which creates a powerful tailwind. On the other hand, SOFI stock is crashing as if the business was shrinking. What is plaguing it are the lofty expectations of Wall Street that came to life in 2020. Moreover, SOFI stock will have strong resistance when it approaches $11 and $13 per share. SOFI investors need to have patience and to not be all-in at once.

— Nicolas Chahine

While Nvidia makes all the headlines, this little-known company is already beginning to surpass Nvidia's stock gains this year as data center growth surges. I believe this stock could soar in the next 12-24 months, potentially leaving Nvidia in the dust. I want to give you the name, ticker and my full analysis today – because I know you certainly won't hear about this stock in the mainstream financial media. Click here to get all the details...

Source: Investor Place